While electric vehicles (EVs) are getting the headlines in the automotive industry, there are two other trends that will reward closer investor attention. These are driver assistance and autonomous vehicles. These are based on similar technologies – advanced sensor systems, machine learning and AI, and interactive interfaces for the human operator – but they fill different roles. For investors, however, these technologies will offer a realm of opportunities where the rubber meets the road.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

The auto industry experts from investment firm Goldman Sachs have been right on top of these new developments in the automotive world, and have been particularly enthusiastic about LiDAR systems. These are high-tech sensor systems (the term is derived from ‘light detection and ranging’) using lasers to provide the highest possible precision in range and velocity information about surrounding objects. LiDAR represents the latest in sensing tech, and Goldman analyst Allen Chang writes of it, “We believe we are in the early stages of LiDAR mass adoption and model global assisted driving penetration to rise 3-fold over the next 10 years. This represents among the fastest growth profiles in the EV supply chain over the next decade.”

We can follow the Goldman Sachs lead and use the TipRanks platform to pull up the details on two of the firm’s LiDAR picks, companies that the G-S analysts see at the forefront of the LiDAR revolution. Each of these target companies has a Strong Buy aggregate rating from the Wall Street analysts, and Goldman sees them with at least 80% upside for the coming year. Let’s take a look at their details, as wells as the Goldman commentaries.

Hesai Group (HSAI)

We’ll start with Shanghai-based Hesai Group, a global leader in the development and application of LiDAR systems. The company’s sensor tech has found uses in autonomous mobility, of course, but also in the trucking industry, robotics, and even factory production. As of December 31, 2022, Hesai Group had shipped out over 100,000 LiDAR units, and the company has also built up strong connections with leading OEMs in the car industry, and has a 60% market share in the autonomous mobility – self-driving car – niche.

Hesai Group only recently joined the U.S. public markets, having carried out an initial public offering of American Depositary Shares (ADS). The IPO, which closed on February 13, saw the company put 10 million ADSs on the market at an opening price of $19 each and raise $190 million in gross proceeds. The IPO was the largest initial offering of a Chinese stock on the US markets since 2021.

Last week, just over a month from the IPO, Hesai released its first quarterly financial results as a publicly traded entity on the US NASDAQ exchange. The report, for 4Q22, showed a quarterly top line of $59.3 million, for a 56% year-over-year increase. This was supported by a massive 739% y/y increase in quarterly LiDAR deliveries which hit 47,515. Of that total, 43,351 were ADAS (advanced driver assistance systems) and 4,164 were autonomous mobility. Despite these successes, Hesai’s stock has suffered in the market downturn and is down 42% since trading began.

Goldman’s Allen Chang, however, sees enough reason to back Hesai. Explaining his bullish stance, he writes, “We highlight Hesai’s three key competitive advantages: (1) Technology – Hesai pursues a unique “ASIC” technology that integrates key components to reduce power consumption, simplify manufacturing and lower unit cost; (2) Manufacturing – Hesai owns a world-class LiDAR manufacturing facility in Shanghai. Their manufacturing and product design reinforce each other, allowing faster product iteration. (3) Large domestic market – China leads ADAS and autonomous adoption, with penetration in new car sales to grow 10X from 8% to 84% (2021-30E). This expansion provides the opportunity for Hesai to scale up its technology.”

Taking this forward, Chang sees fit to rate the shares as a Buy, with a $29 price target that implies a robust 123% upside potential for the coming year. (To watch Chang’s track record, click here.)

In its short time on the US public markets, Hesai has picked up 3 analyst recommendations – and they are all positive, for a unanimous Strong Buy consensus rating. The stock has a current trading price of $13.00, and its $28.50 average price target suggests a 12-month gain of 119%. (See Hesai’s stock forecast at TipRanks.)

Innoviz Technologies (INVZ)

Next on our list is Innoviz Technologies, another leader in the world-wide LiDAR market. Innoviz both designs and manufactures high-end solid-state LiDAR sensors, along with the software required to connect the sensor hardware with the controlling computer systems. Innoviz has been working with several big-name automotive companies, including BMW and Volkswagen.

Innoviz shares showed a peak in February of this year, and are down 33% from that level; over the past two years, the stock has fallen 65%. During this time, the company has been running net losses, and revenues have failed to take off. A look at the company’s last financial report shows that the full year 2022 numbers are modestly higher year-over-year, that the 4Q22 missed expectations, and the forward guidance disappointed.

At the quarterly level, the company showed revenues of $1.58 million, missing the estimates and down almost 5% year-over-year. The company’s Q4 EPS, a 25-cent loss, came in below the 24-cent loss forecast. In the full year numbers, the top line did grow 10% to 6 million, and the company sold a record number of LiDAR units.

Further souring sentiment, Innoviz missed on the forward revenue guidance. The company projected total 2023 revenues in a range between $12 million and $15 million; while this would represent a doubling – or more – of the top line y/y, the analyst consensus had expected guidance of ~$30 million.

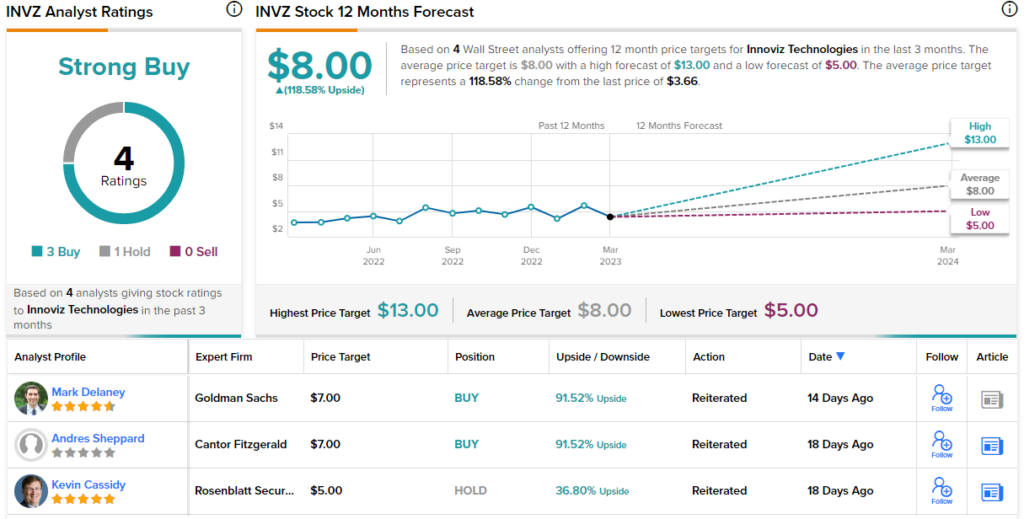

This stock is covered for Goldman by 5-star analyst Mark Delaney, who acknowledges the headwinds that the company is facing but goes on to outline an upbeat prospect: “We believe the 4Q report was an incremental negative, although we maintain our Buy rating on the stock reflecting our positive view of the company’s long-term opportunity. Specifically, we believe that the company’s order book remains strong including design wins at 3 auto OEMs (i.e. BMW, VW, and an Asian based OEM). While the production ramp up is occurring more slowly than we’d expected with 2023 revenue guidance below the Street, we believe that as OEM ADAS programs ramp in the coming years that the company will see improved results.”

Quantifying his stance, Delaney rates INVZ shares as a Buy, and his price target, set at $7, indicates his confidence in an upside of 91% for 2023. (To watch Delaney’s track record, click here.)

Overall, Innoviz has a Strong Buy consensus rating from the Street, based on 4 analyst reviews with a 3 to 1 breakdown favoring Buy over Hold. The stock has an $8 average price target, higher than the Goldman outlook and suggesting a 118% upside from the trading price of $3.66. (See Innoviz’s stock forecast at TipRanks.)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.