This year started with a red-hot stock market, there is no question of that. Since the start of 2023, even accounting for losses last week, the S&P 500 shows a year-to-date gain of 17%, and the NASDAQ is up 33%.

Currently, the gains are narrow, mainly relying on a handful of deep-pocketed, big-name tech firms, but there’s a likelihood that investor money will start spreading more widely. If the bull market does widen out, it will raise the question of which stocks to buy.

This is where Goldman Sachs comes in. The banking giant has a special rating for stocks which it holds in particularly high regard. This is called a ‘Conviction Buy’ rating. The firm’s prized list of Conviction Buy stocks reveals the stock picks that the firm’s analysts expect to beat the market.

Now, let’s zoom in on two such names that have earned a spot on Goldman Sachs’ list of top stock ideas.

Chevron Corporation (CVX)

The first Goldman pick we’ll look at is Chevron, one of the world’s largest oil companies, with a market cap of $298 billion and annual revenues in the neighborhood of $240 billion. The company’s operations are varied and include hydrocarbon exploration and production, a transportation division that includes a maritime shipping company, an active refining segment producing fuels, lubricants, petrochemicals, and additives, a retail division to market the refined products (including a chain of gasoline filling stations), and a 50/50 joint venture with Phillips 66 in the industrial fuel and chemical sector.

Post-COVID, the price of oil peaked in May of last year, and the price since then has been downward. Chevron’s financials have tracked with the price of oil, declining from a 2Q22 peak – but the company remains profitable, benefiting from continued high demand for oil and fuels. Consumer demand for oil has been rising this year and is expected to increase by 2.2 million barrels per day to reach a year-end average of 102.1 million barrels per day.

On the financial side, Chevron reported its 2Q23 results last month, and despite the continuing fall-off from peak values it beat the expectations on both revenues and earnings. The top line, a revenue total of $48.9 billion, was down 29% year-over-year, but was over $900 million better than the forecast. At the bottom line, the company’s EPS of $3.20 beat the estimates by 22 cents per share. In addition to beating the earnings forecasts, Chevron also generated $6.3 billion in cash flow from operations, and $2.5 billion in free cash flow. The company returned a record amount of capital to shareholders, a total of $7.2 billion.

That return to shareholders included the regular share dividend. Chevron last declared its dividend on July 28, for $1.51 per share. This annualizes to $6.04 per common share, and yields 3.8%. Chevron has a dividend history going back to 1990, and has been gradually raising the payment since 2005.

Goldman’s 5-star analyst Neil Mehta is impressed by Chevron’s cash and capital returns, and writes of the stock: “Look for an inflection in the US oil major’s shares as (a) key upstream projects come online and other execution risks abate, driving robust cash generation, (b) shares are supported by a leading capital returns profile among large cap Energy and the S&P100, and (c) relatively attractive valuation.”

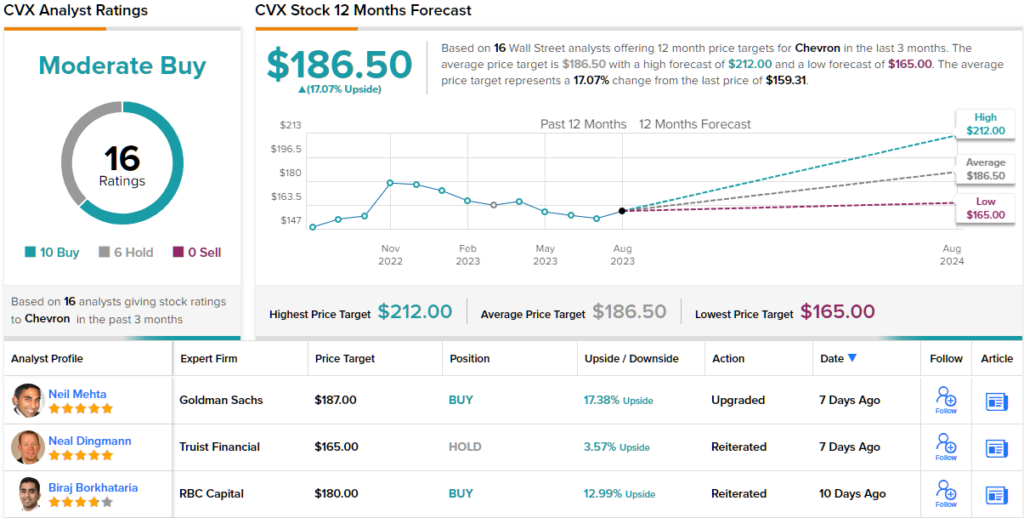

Looking forward, Mehta rates Chevron as a Conviction Buy, and his price target of $187 indicates room for a 17% upside potential in the year ahead. (To watch Mehta’s track record, click here)

Overall, Chevron gets a Moderate Buy rating from the Wall Street consensus, based on 16 recent analyst reviews that break down 10 to 6 favoring Buys over Holds. The shares are priced at $159.31, and the average price target of $186.50 is practically the same as Mehta’s. (See Chevron stock forecast)

Macy’s, Inc. (M)

Next up is Macy’s, a well-known name in American retail. Tracing its origins back to 1858, this department store has evolved into an omni-channel retailer, boasting a significant e-commerce footprint and a network of brick-and-mortar stores. Macy’s offers quality brands across all price ranges, from upscale luxury to off-price discount, providing customers with a seamless and convenient shopping experience.

The company owns several brands, including its eponymous department stores, as well as Bloomingdale’s and Bluemercury. As of the end of the calendar year 2022, Macy’s operated 783 stores across all of its brands, with 566 Macy’s locations and 160 Bluemercury stores.

In an interesting move, Macy’s announced in March plans to conduct a transition in its corporate leadership. The current CEO, Jeff Gennette, will be retiring in February of next year after 40 years with the company. His position will be taken over by Tony Spring, who is currently an executive VP with Macy’s and the CEO of the Bloomingdale’s brand.

The company will release its 2Q23 financial results on August 22, but we can look back at Q1 to see where Macy’s stands now. The top line, of $5 billion, was slightly down from $5.3 billion in the prior-year quarter and $84 million below analyst expectations. However, Macy’s demonstrated stronger bottom-line results, with a 56-cent GAAP EPS, which was 10 cents better than the forecast. Looking ahead, Macy’s has revised its expectations for FY2023 sales, now projecting a range of $22.8B to $23.2B. This adjustment comes in contrast to the previous projection of $23.7B to $24.2B and falls below the consensus estimate of $24.01B.

Macy’s has a history of paying out cash dividends since 2003, with a brief interruption from early 2020 to the summer of 2021 due to the pandemic. Dividend payments resumed in August 2021 and have been gradually rising since then. The latest declaration on May 31 was for a 16.54 cent payment, distributed on June 15. The common share dividend currently annualizes to just over 66 cents, offering a yield of 4.06%.

This stock is covered for Goldman Sachs by analyst Brooke Roach, who sees the company poised for success on the back of a new growth strategy. She is also impressed by strength of the company’s brand and cash positions, and writes: “Look for the US department store to execute on its five pillar growth strategy after successfully completing ‘trial and learn phases’ this year. Focus on M’s new idiosyncratic initiatives, and look for strengthening execution and improving inventory management to drive market share capture, growth, and profitability, supported by Macy’s strong brand positioning and FCF generation.”

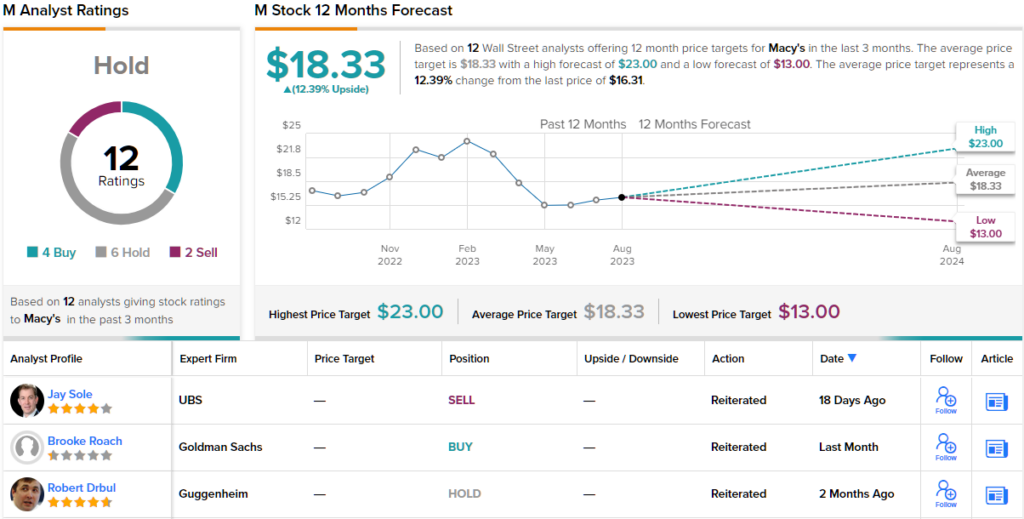

Roach goes on to give Macy’s a Conviction Buy rating, with a $23 price target implying a 41% one-year upside potential. (To watch Roach’s track record, click here)

The rest of the Street is less confident, however; based on 4 Buys, 6 Holds, plus 2 additional Sells, the stock has a Hold consensus rating. Meanwhile, the stock’s average price target of $18.33 suggests an upside of ~12% from the current selling price of $16.31. (See Macy’s stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.