Hark back to the start of the year and few saw the markets recovering to the extent they have, particularly after 2022’s overall performance was the worst seen since 2008.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

But here we are more than six months later and the S&P 500 and particularly the tech-loaded NASDAQ have completely exceeded expectations, with the surge built on investors’ appetite for everything AI.

But not all stocks have been riding the AI gravy train. Some have been excluded from the rally and have retreated during the year, although that doesn’t mean they are headed for the permanent bargain bin.

In fact, the analysts at banking giant Goldman Sachs have been performing one of their favorite pastimes – tagging the stocks that they see as primed for gains in the latter half of the year. Specifically, firm analyst Adam Samuelson has pinpointed an opportunity in two beaten-down names he sees pushing higher over the coming months – by the order of 40% or more.

We ran these tickers through the TipRanks database to see what other Street experts make of their chances. Here are the details.

The Mosaic Company (MOS)

Let’s begin in the agricultural sector and zoom in on The Mosaic Company. This heavyweight in the crop nutrient industry has earned its reputation as a leading global producer and marketer of concentrated phosphate and potash fertilizers. The Tampa, Florida-based firm focuses on mining and processing phosphate rock, which is then used to produce agricultural fertilizers, and potash, a vital nutrient for crops. The company’s products are essential in promoting crop productivity and improving soil fertility, thereby supporting the global agricultural industry.

Early last year, fertilizer prices increased dramatically in the wake of Russia’s invasion of Ukraine and subsequent Western sanctions on Russia and Belarus led to supply issues. However, as supply from Belarus started again – it is the third biggest exporter of potash – fertilizer prices also came down and that affected Mosaic’s latest quarterly results.

In Q1, adj. EPS fell from $2.41 in the same period a year ago to $1.14, while missing the Street’s call by $0.11. Revenue also dropped, by 8.2% year-over-year to $3.6 billion, although that figure actually beat Wall Street expectations, by $340 million. More recently, the company said it expects Q2 potash sales volumes will come in at the high end of the 2-2.2 million metric tons guide and phosphates at the low end of the 1.8-2 million tons guide.

Year-to-date, MOS shares peaked back in March but have since retreated by 36%. While Goldman analyst Adam Samuelson is cognizant of the present issues, he highlights Mosaic’s appeal for investors.

“While we recognize the current turbulent environment in the fertilizer market (and broader commodities) blurs the short-term outlook, management remains prudent on capital allocation and MOS’ portfolio of production assets appear sharply discounted relative to peers, let alone potential replacement cost,” the analyst noted.

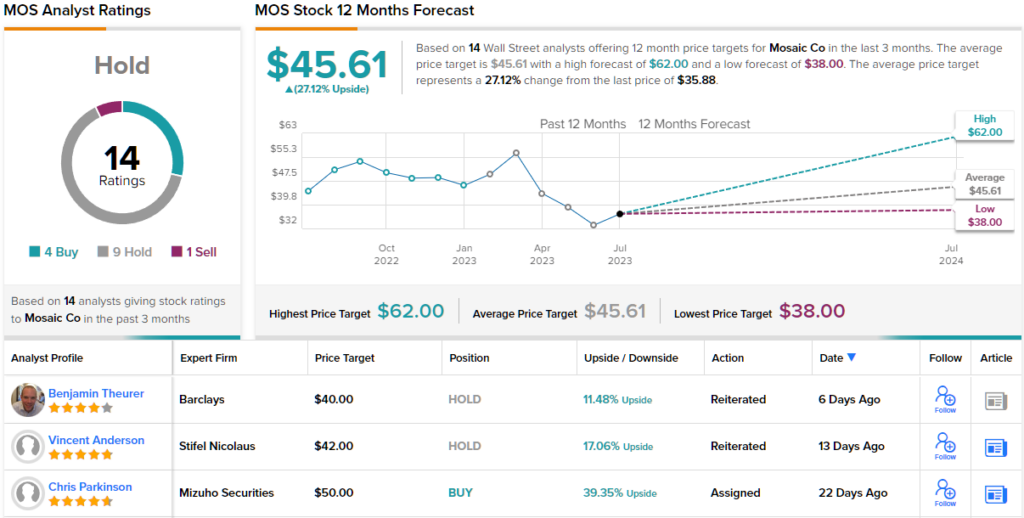

Accordingly, Samuelson rates MOS as a Buy along with a $62 price target, suggesting the stock will climb ~73% higher over the coming months. (To watch Samuelson’s track record, click here)

That said, Samuelson’s take is the Street’s most exuberant one. Elsewhere, the stock garners an additional 3 Buys, 9 Holds and 1 Sell, for a Hold consensus rating. Nevertheless, most feel the shares are undervalued; going by the $45.61 average target, a year from now, they will be changing hands for a 27% premium. (See MOS stock forecast)

Sealed Air Corporation (SEE)

Let’s take a turn now from the fertilizer industry to packaging and the aptly named Sealed Air. Fun fact, the company is responsible for the invention of the iconic Bubble Wrap, the cushioning material widely used for protecting fragile items during shipping, and Sealed Air was founded based on that invention.

Today, Sealed Air is a global packaging company that provides a range of innovative packaging solutions for various industries and is a leader in protective packaging and food safety solutions. Its offerings include protective packaging materials, such as foam and air cushions, as well as automated equipment and systems for packaging optimization.

The global economic woes have not spared the packaging industry. Companies using such products have been impacted by the recessionary environment and that in turn has affected SEE’s business.

In Q1, volumes dropped by 9.3% on the back of a 10.4% decline in Q4, both historically sharp drops not witnessed by the firm since 2008-09. As such, revenue came in at $1.3 billion, amounting to a 7.1% decline and falling short of the consensus estimate by $60 million. Adj. EPS of $0.74 also missed expectations, by $0.03. For the full year, SEE reiterated its outlook for adj. EPS in the range between $3.50 to $3.80, just shy of consensus at $3.66 at the mid-point.

This is the kind of stuff that does not help a stock’s performance, and indeed, the shares are down by 23% since this year’s February peak. However, according to Goldman’s Adam Samuelson, this could be an opportunity for investors.

“While we recognize near-term cyclical pressures and do see risk that the upper half of full-year guidance and implied Protective volume recovery appear ambitious, SEE’s underlying franchise strength and long-term growth from automation and digital solutions remain sharply discounted at 9.1x /8.3x 2023/24 EV/EBITDA. We see current weakness offering a compelling entry point for longer-term investors,” Samuelson opined.

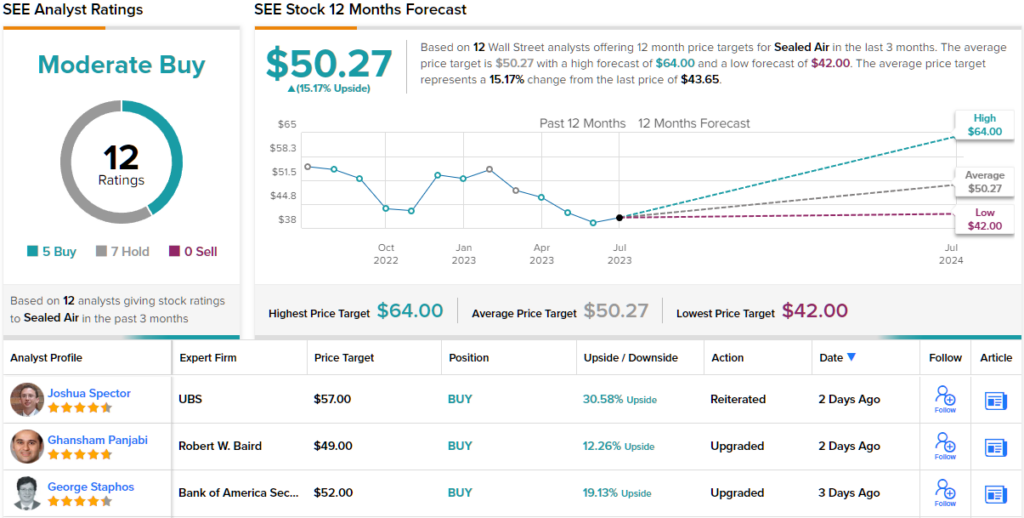

Samuelson, then, recommends that investors buy SEE shares, as his $64 price target indicates the potential for ~47% returns over the next 12 months.

Elsewhere on the Street, 4 other analysts join Samuelson in the bull-camp and with an additional 7 Holds, the analyst consensus views this stock a Moderate Buy. The average target currently stands at $50.27, implying shares will deliver 15% gains in the months ahead. (See SEE stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.