It’s no secret that the big gains in the stock market this year have been on account of only a select number of equities surging ahead – namely, the Mega Caps, and mostly ones with AI exposure.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

While that has raised concerns among market watchers that the rally is not really as strong as it appears and masks a more fragile market, Sharmin Mossavar-Rahmani, head of the investment strategy group at Goldman Sachs, disagrees with such a prognosis. In fact, Mossavar-Rahmani thinks that if history is anything to go by, it is indicative of further gains to come.

“What is really fascinating when you’ve had this kind of narrow breadth, the market actually continues to rally,” she recently said. “So in the three instances of market narrow breadth we can look at in the last 20, 30 years, the market actually continued to have double-digit returns after that.”

Moreover, while many financial prognosticators are expecting a recession to materialize at some point over the coming months, the strategists at Goldman Sachs also think that is less likely than before, with the bank having recently lowered the probability of a recession from 25% to 20%.

So, with this positive outlook in tow, it’s only natural to look for the prospective winners in such an environment, and here the analysts at Goldman can point investors in the right direction too. They have earmarked two stocks as ready to push ahead from here, and they even see one surging by 120% over the following months.

Are other Wall Street analysts on the same page? Looks like it. According to the TipRanks database, both are rated as Strong Buys by the analyst consensus. Let’s see why these equities have solid upside in them.

Amylyx Pharmaceuticals (AMLX)

The first Goldman-backed name we’ll look at resides in the biotech space. Amylyx is a biopharma that seeks to address the significant unmet medical needs in the field of neurodegenerative disorders. As such, the company is focused on developing innovative therapies for neurodegenerative diseases. Amylyx is dedicated to advancing its research and translating it into potential treatments for conditions like amyotrophic lateral sclerosis (ALS), Alzheimer’s disease, and other related neurological disorders.

A biotech’s holy grail is to get a drug approved and Amylyx has achieved that milestone. AMX0035, given the commercial name Relyvrio in the US, gained FDA approval last September to halt the progress of amyotrophic lateral sclerosis (ALS). The drug is also approved in Canada, and the launch appears to be going well; in Q1, Relyvrio generated revenue of $71.4 million, significantly improving on the $21.9 million recorded in 4Q22.

AMX0035 is also being assessed as a therapy for Alzheimer’s disease and Wolfram syndrome while the company also intends to kick off a Phase 3 trial of AMX0035 in progressive supranuclear palsy later this year.

There’s also an ongoing Phase 3 clinical trial of AMX0035 in people living with ALS that will have implications about the continued use of the drug. Goldman Sachs’ Corinne Jenkins thinks a downbeat view regarding the study’s success has been responsible for the stock’s lackluster performance this year (down by 40%).

However, the analyst has a more upbeat take and writes, “AMLX shares have significantly underperformed year-to-date, despite a better-than-expected US commercial launch of Relyvrio in amyotrophic lateral sclerosis (ALS), primarily due to investor concerns related to the likelihood of success in the ongoing Ph3 PHOENIX study (data expected in 2024). With this context in mind, we evaluated the probability of PHOENIX success using a proprietary statistical analysis that suggests a >60% chance that PHOENIX demonstrates statistical significance. Further, our model indicates a >70% probability that PHOENIX achieves p<0.1, which we believe is sufficient for the drug to remain on market, with a modest impact on the peak sales opportunity in the US.”

“On balance,” Jenkins summed up, “we see this as an attractive entry point for the stock in the context of a strong US launch and better-than-feared outlook into PHOENIX results next year.”

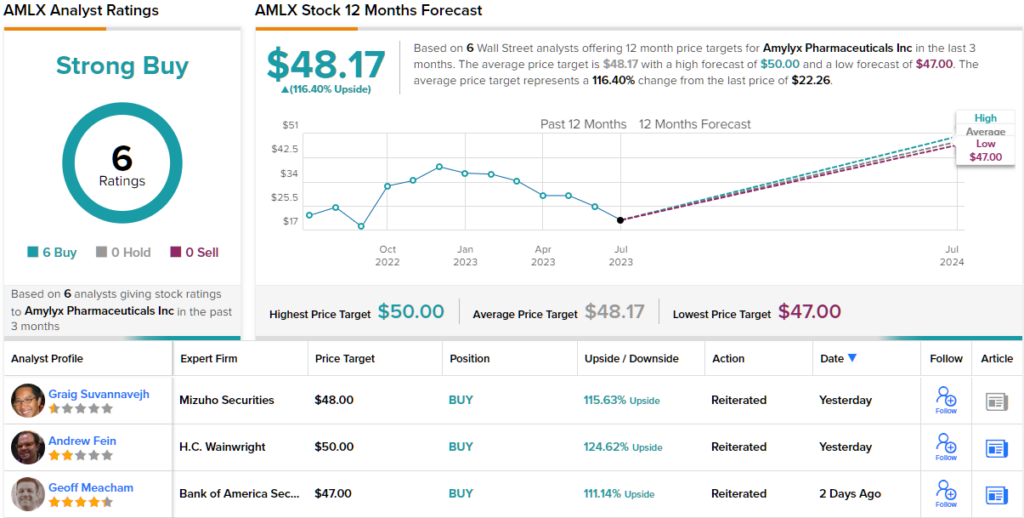

An attractive entry point, indeed. Along with a Buy rating, Jenkins gives AMLX a $49 price target, which makes room for share gains of 120% in the year ahead. (To watch Jenkins’ track record, click here)

Other analysts are no less upbeat. All current ratings are to Buy – 6, in total – naturally making the consensus view here a Strong Buy. The average target stands at $49, the same as Jenkins’ objective. (See AMLX stock forecast)

Kodiak Gas Services (KGS)

For our next Goldman-endorsed name we’ll shift our focus to an entirely different sector – the natural gas compression market. Natural gas compression plays a crucial role in the production process. It involves raising the pressure of natural gas to facilitate its efficient transportation through pipelines and other transportation networks for eventual consumption by end-users.

This is the value proposition of Kodiak Gas Services, a top-tier supplier of natural gas contract compression services in the US. The company touts its pioneering gas compression technology, and it provides a broad range of turnkey and operational services to the upstream and midstream sectors of the oil and gas industry, all specifically tailored to its clients’ needs.

The Montgomery, Texas-based firm is a newbie in the markets, having held its IPO last month. The company sold 16 million shares in the IPO, priced at $16 apiece and raised $256 million. The shares began trading on the New York Stock Exchange on June 29, and since the close of the debut session, the stock is up by 16%.

That is not much of a surprise to Goldman analyst John Mackay, who points out several reasons why investors should take note of this new energy player.

“Kodiak is a leading company in the natural gas compression market and is well positioned to benefit from strong growth in both US gas supply (most immediately in the Permian) and upcoming demand inflections (notably from LNG capacity additions in 2025+),” Mackay said. “We see solid upside for the stock from here given: 1) favorable fundamentals for the overall compression market that should support EBITDA growth with low relative capital intensity; 2) its high quality asset base relative to peers that should support a better relative multiple; and 3) a clear capital allocation strategy – all with an unchallenging valuation.”

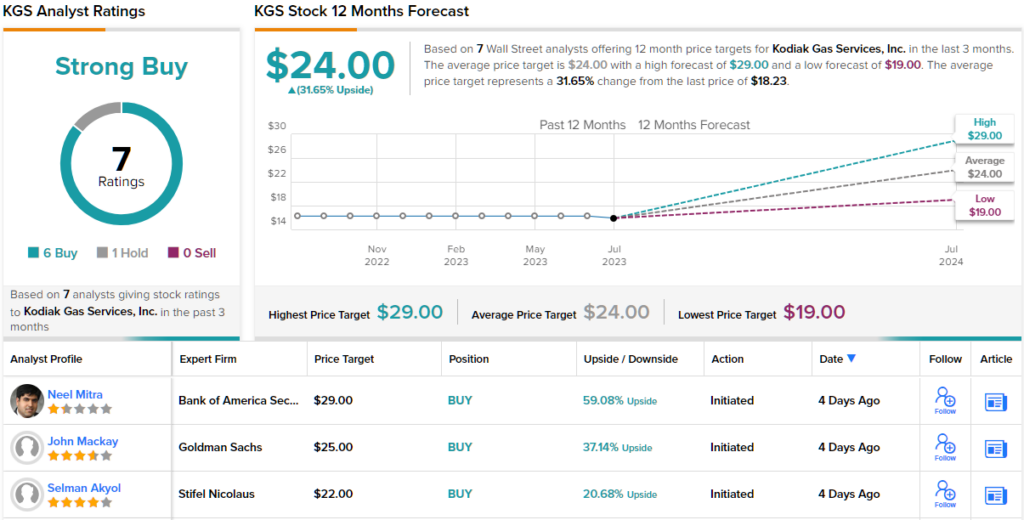

To this end, Mackay rates KGS a Buy rating, along with a $25 price target. The implication for investors? Upside of 37% from current levels. (To watch Mackay’s track record, click here)

Wall Street has taken to this name pretty quickly. The stock boasts a Strong Buy consensus rating, based on 6 Buys vs. 1 Hold. At $24, the average target suggests shares will post growth of ~32% over the coming year. (See KGS stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.