The crystal balls are cloudy, and the energy sector is difficult to predict for 2024. Conventional wisdom says, ‘Oil is going higher;’ after all, there is a war in the Middle East. But neither Israel nor Hamas exports oil, and prices are down from a mid-October spike.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

The conflicted headwinds of the energy sector, and the oil industry especially, have put heavy pressure on energy stocks in recent months. Even the current war in the Middle East only caused a brief spike in prices, and the OPEC+ group’s efforts to pare back production have simply provided a floor in the current environment – they have not pushed prices back toward recent high levels.

The wild card here is a possible US recession. If one hits in 2024, that could crimp oil demand – but we may also see a Fed rate cut, which could in turn goose a call for more oil.

For Goldman analyst Neil Mehta, however, this confused environment equals opportunity. He sees a strong chance for several energy stocks to make a 2024 turnaround. “As we make the turn into 2024, we continue to screen for companies with turnaround and mean reversion potential in a mid-cycle $80/b Brent and $3.50/MMBtu Henry Hub environment,” the 5-star analyst recently wrote. “Amid a tougher year for Energy equities, there has been significant differentiation in stock performance across sub-sectors.”

Moving forward, Mehta sees opportunity in specific names and is bullish on the prospects of two major energy stocks that have underperformed over the past year. We ran them through the TipRanks database to see what makes them stand out. Here’s the lowdown.

Schlumberger Limited (SLB)

For the first, we’ll look at a leader in the oilfield services sector. The exploration and production companies put their money down finding the oil, siting the wells, and bringing the product to the surface. But, they lack the specific expertise to complete those wells; companies like Schlumberger provide all the particular engineering and technical know-how needed to complete wells and put them into operation. These skills include, among others, drilling, hydraulic engineering, and pollutant control. In 2022, Schlumberger was the world’s largest offshore drilling company, measured by revenue.

Drilling and well completion, however, are only part of Schlumberger’s operations. The company sees the writing on the wall, and understands that today’s fossil fuel energy regime will not last forever, and it is diversifying its operations now, both to expand its revenue base and to prepare the next generation of energy technology. These forays into alternate business models include Schlumberger’s business in digital technology, scaled to fit customer needs at any size and capable of tracking and accessing data, developing insights from it, and using that data to elevate performance. The company is also moving into AI technology, to enable autonomous operations on the oil patch.

Schlumberger’s operations brought the company solid year-over-year increases in its headline financial results in the third quarter of 2023, the latest reported. The company had a bottom line of 78 cents per share, in non-GAAP measures; this was a full 15 cents per share better than the prior-year result, and came in 1 cent above the forecast. The earnings were based on $8.31 billion in total revenue, a figure that was up 3% from the previous quarter and 11% year-over-year. The company’s revenue, however, came up short of the forecasts, missing by $10 million.

Free cash flow in the third quarter was strong, listed as $1.04 billion. This made up the larger part of the company’s $1.76 billion FCF for the first nine months of 2023. Schlumberger generated far stronger cash flows in Q1,2, and 3 of 2023 than in the prior year, when the nine-month total came to just $563 million.

While Schlumberger saw sound financial performance, we should note here that the stock price has simply been treading water in 2023. Shares were barely breaking even at the end of trading on December 29, the year’s last trading day, and the stock was down approximately 16% from the peak it hit in September 2023.

Turning to the Goldman view, we find that analyst Neil Mehta is bullish here, basing his view at least in part on the company’s solid performance as an offshore driller and its moves into digital tech. Moreover, the stock’s underperformance represents an opportunity. Mehta writes, “We believe that at the current price the stock is fundamentally undervalued as international rig count still remains below pre-COVID levels, offshore activity outlook has remained resilient and SLB continues to expand its digital business. We believe that the stock should be positioned to outperform as macro activity indicators continue to grind higher, margin expansion from repricing contract portfolios continue to improve and over time as the company begins to commercialize its newer businesses in new energy.”

For Mehta, this provides support for a Buy rating, and his price target, set at $65, suggests a one-year upside potential of 25%. (To watch Mehta’s track record, click here)

This stock has a Strong Buy rating from the Street, based on a lopsided split among the 13 recent analyst reviews – 12 to Buy and 1 to Hold. The shares are trading for $52.04 and their $70.58 average target price points toward a one-year gain of 36%. (See Schlumberger stock forecast)

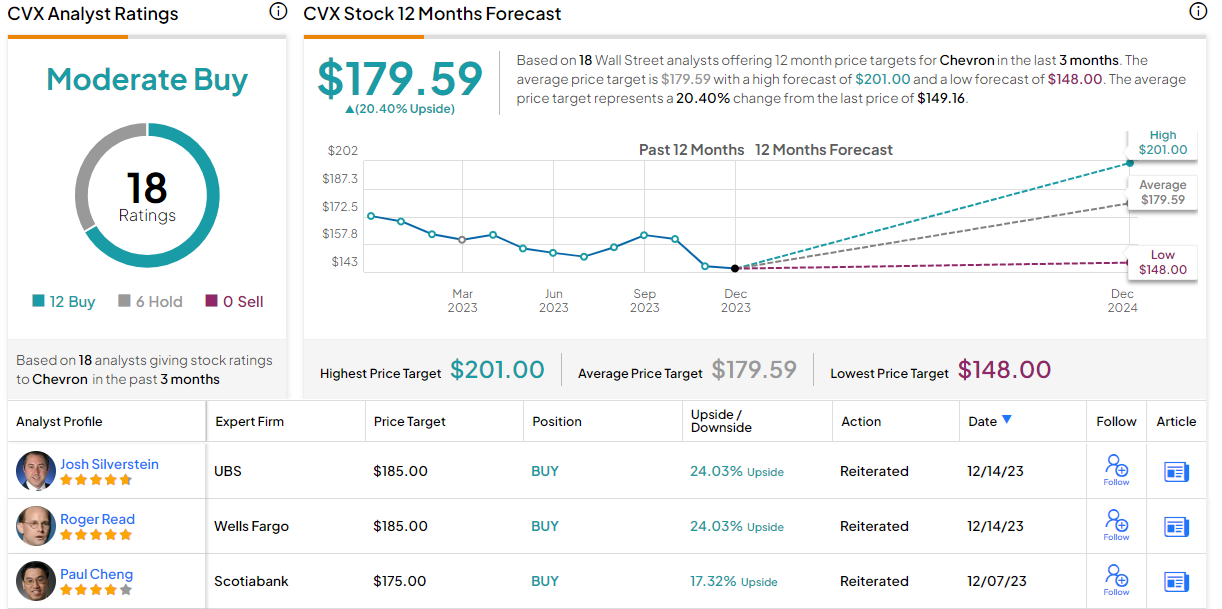

Chevron Corporation (CVX)

From oilfield services we can move over now and take a look at a major-name exploration and production company. Chevron is ranked, by market cap, as the world’s third-largest oil company, valued at ~$281 billion by that measure.

The company’s business and activities revolve around oil and natural gas exploitation, transport of hydrocarbon products, operation of a maritime shipping line for both crude oil and natural gas products, and a large-scale petroleum refining segment.

Chevron is a major producer and supplier of a wide range of petrochemicals, including fuels, lubricants, and various additives. While not the main thrust of Chevron’s business, it’s probably the most visible in our everyday life – Chevron markets many of these products, including gasoline and diesel fuel, through its nation-wide chain of branded gas stations.

The biggest recent news for Chevron, however, has come from two updates in its oil business. In 2023, in October, the company entered a definitive agreement with Hess Corporation, an independent E&P firm specializing in offshore hydrocarbon extraction. The agreement’s total value comes to $60 billion, including the $53 billion all-stock acquisition transaction and approximately $7 billion in debt assumption by Chevron. The merger is expected to be completed in 1H24.

The second large piece of news for Chevron comes from Kazakhstan, near the northeastern shores of the Caspian Sea. Chevron is expanding an already significant operation in this area, where it has a 50% interest in Tengizchevroil, or TCO. TCO is the operating firm exploiting the Tengiz oil field, a ‘supergiant’ field known to be one of the world’s largest single-trap producing reservoirs. The Tengiz has a massive proven reserve, estimated at 25.5 billion barrels of recoverable oil. Daily production in the field is already averaging 600,000 barrels of crude oil every day, along with 22 million cubic meters of natural gas.

Chevron’s last reported financial results on record are from 3Q23, when the company had $54.08 billion at the top line. While this total was more than 18% below the prior-year revenue, it did beat the forecast, by $1.08 billion. The oil giant’s earnings, the non-GAAP EPS, came to $3.05 per diluted share – and missed the forecast by 64 cents per share. Investors were not too keen on the results, sending shares down in the aftermath. Overall, the stock trended lower in 2023, falling some 17% from the peak seen in January last year.

Laying out the Goldman Sachs view of Chevron, analyst Mehta lists several factors to support optimism, including strong prospects for gains in the HES acquisition and the Tengiz oilfield expansion operations. He writes of CVX, “Heading into 2024, we believe (a) improving earnings execution, (b) regular updates on TCO, (c) continued commitment to return of capital through-the-cycle, and (d) attractive balance sheet should drive 2024 outperformance. On capital returns we expect the company to be competitive in return of capital, with GS estimates of ~$29 bn in 2024 (buybacks + dividends), representing ~10% yield, with room for upside on potential HES transaction close, based on company commentary. On Tengiz, we continue to look for updated management commentary surrounding the WPMP and FGP start-ups in 2024 and 2025, where we see the project driving a clear Upstream volume ramp and cash flow inflection in 2025.”

Putting this into quantifiable form, Mehta rates CVX as a Buy, and his $180 price target implies the shares will appreciate by 21% through 2024.

For the Street generally, this stock remains a Buy, albeit a Moderate Buy. This consensus rating comes from 18 analyst reviews, breaking down 12 to 6 in favor of Buys over Holds. Chevron’s shares have a current average target price of $179.59, suggesting a 20% one-year increase from the last trading price of $149.16. (See Chevron stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.