What to make of the markets this year? 2022 started with a sharp drop, and we’re still seeing increased volatility, with large intraday swings in the main indexes. But where January was noted for showing four weeks in a row of net losses, February hasn’t been so hard on investors.

Looking at the situation from Goldman Sachs, global chief equity strategist Peter Oppenheimer notes several points. First, that January’s jobs report was far better than expected, indicating economic strength, and second, that the markets have priced in the Fed’s change of policy. The second point may be key, in his view.

“Overall, the economy remains pretty robust. And as long as the economy is still growing, then profits will grow. And although we’ve seen a D rating in the equity market as interest rates have increased, we’ll still get a gradual trend in equity markets higher,” Oppenheimer opined.

The stock analysts at Goldman Sachs have been following Oppenheimer’s lead, and pointing out the stocks they see primed for gains. And those gains may be substantial; in the Goldman view, perhaps as much as 70% or more this year. We used the TipRanks platform to look up the details on two of these stocks; here is what we found.

Cytokinetics (CYTK)

The first stock on Goldman Sachs’ radar is Cytokinetics, a clinical-stage biopharmaceutical company with a pipeline showing plenty of ‘shots on goal.’ The company is working on new drugs for musculoskeletal disorders, and its research tracks feature a series of first-in-class and next-in-class drug candidates for several diseases that cause severe loss of muscle function.

The company’s leading drug candidate, on its cardiac muscle research track, is omecamtiv mecarbil, a prospective treatment for heart failure. This investigational drug candidate is a novel cardiac muscle activator, and has recently completed the GALACTIC-HF Phase 3 clinical trial. While the trial did not show a benefit in regard to cardiovascular death, it did show a statistically significant benefit for patients in regard to hospitalizations. These results built on previous studies that showed a favorable tolerability profile. Based on the trial, Cytokinetics made a New Drug Application to the FDA, which the agency has accepted. The PDUFA target date is November 30 of this year.

In addition to the regulatory progress on omecamtiv mecarbil, Cytokinetics has reported clinical progress on another late-stage drug candidate. The company released topline data from Cohort 3 of the REDWOOD-HCM study, a clinical trial of aficamten. This Phase 2 trial is evaluating the drug in the treatment of hypertrophic cardiomyopathy, or HCM. The newly released results showed a clinically significant positive response in patients. Aficamten is currently undergoing the SEQUOIA Phase 3 trial, a 24-week randomized double-blind placebo-controlled study, enrolling up to 270 patients, that started last month.

Goldman Sachs 5-star analyst Madhu Kumar is bullish on Cytokinetics, citing both of the above drugs. He sees aficamten as the main driver, as it is more likely to show a strong patient response and has a Phase 3 study in the offing.

“This announcement [the NDA acceptance] is consistent with the path to approval for OM following Phase 3 GALACTIC-HF showing significant clinical benefit for the composite of first HF event or CV death vs placebo. Given this, the key consideration for OM is the commercial launch given the lack of evidence demonstration clinical benefit from the drug on CV death. That said, we reiterate that the launch of OM could create salesforce synergies for the potential approval and launch of aficamten in obstructive hypertrophic cardiomyopathy (oHCM). Overall, our primary focus continues to be on aficamten in oHCM, with the Phase 3 SEQUOIA-HCM [trial],” Kumar wrote.

To this end, Kumar gives CYTK a Buy rating to go along with this bullish outlook, and quantifies it with a $74 price target to indicate potential for 84% upside in the year head. (To watch Kumar’s track record, click here)

It’s not often that the analysts all agree on a stock, so when it does happen, take note. CYTK’s Strong Buy consensus rating is based on a unanimous 11 Buys. This stock’s $58.27 average price target implies ~45% upside from the current trading price of $40.24. (See CYTK stock forecast on TipRanks)

Amylyx Pharmaceuticals (AMLX)

The next stock on our list of Goldman picks is Amylyx, a biopharma company focused on neurodegenerative diseases. Based in Cambridge, Massachusetts, the company’s research focuses on drug candidate AMX0035, a product with a wide range of uses currently under investigation as a treatment for three indications: amyotrophic lateral sclerosis (ALS), Alzheimer’s disease, and Wolfram syndrome. The ALS track is farthest along the research and regulatory process.

In December of last year, Amylyx announced that the FDA had accepted the NDA on AMX0035 as a treatment for ALS – and had granted a Priority Review status. The PDUFA date is set for June 29, 2022. The company is currently evaluating AMX0035 in the globally-based PHOENIX, a test of the drug against ALS. The study is enrolling 600 patients, all within 24 months of the onset symptoms.

In addition to the FDA regulatory update, Amylyx has had AMX0035 accepted for review by regulatory authorities in Canada, and the EU MAA submission was submitted in January of this year.

Global clinical trials and multiple regulatory submissions don’t come cheap. To raise capital, Amylyx went public just this past January. The company put 10 million shares on the market, at $19 each, in an offering that was upsized from the initial filing. Overall, the company raised $190 million in the offering.

Goldman analyst Chris Shibutani, one of the firm’s 5-star analysts, notes the advantages of AMX0035, with its successful clinical trial history and its potential for label expansion. At the bottom line, he sees it as a major asset for Amylyx just in the ALS field, which he estimates to have a $1.4 billion global sales peak.

“We believe that Amylyx Pharmaceuticals is positioned for a successful commercial launch in ALS as the company’s lead drug candidate, AMX0035, is the first agent to have demonstrated a benefit on both function and survival in patients with ALS… Based on the data observed to-date, including the drug’s strong safety profile, and given the significant unmet medical need in ALS, we see a high likelihood of approval… Further, we expect that AMX0035 will quickly capture significant market share as currently available therapies provide limited efficacy benefit in ALS,” Shibutani explained.

In light of this bullish stance, Shibutani gives the stock a Buy rating along with a $36 price target that implies a one-year upside of 75%. (To watch Shibutani’s track record, click here)

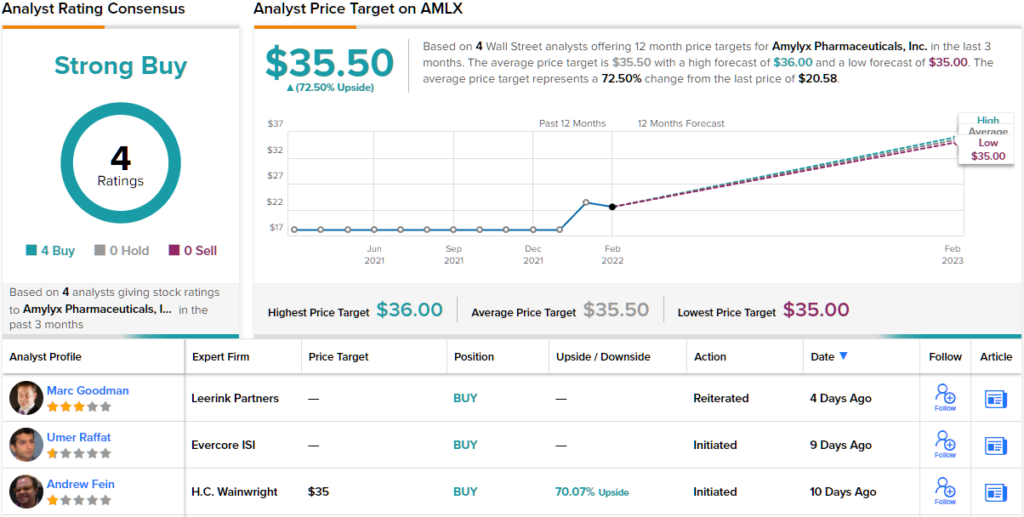

Amylyx has only been a public stock for a short time, but in that time it has picked up 4 positive analyst reviews for a unanimous Strong Buy consensus rating. The shares are selling for $20.58 and the $35.50 indicates room for 72.5% growth from that level. (See AMLX stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.