After 2022’s inflation-driven market meltdown, 2023’s bogey number 1 appears to be the fear of a global recession. However, Sharmin Mossavar-Rahmani, CIO of Goldman Sachs’ wealth-management segment, does not necessarily think this is a particularly bad omen for the stock market.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

“We’re not arguing that today’s valuations fully discount a recession, but considering last year’s equity drawdown, we do think a significant part of any valuation reset has already occurred,” Mossavar-Rahmani opined.

In fact, Mossavar-Rahmani thinks the S&P 500 has room to move 12% higher this year, even if a mild recession does materialize. “Put simply,” she added, “markets bottom when the news is still bad.”

Against this backdrop, Mossavar-Rahmani’s analyst colleagues at the banking giant have pinpointed three names that they think will benefit from such a rally. We ran the tickers through TipRanks database to see what other Wall Street’s analysts have to say about them.

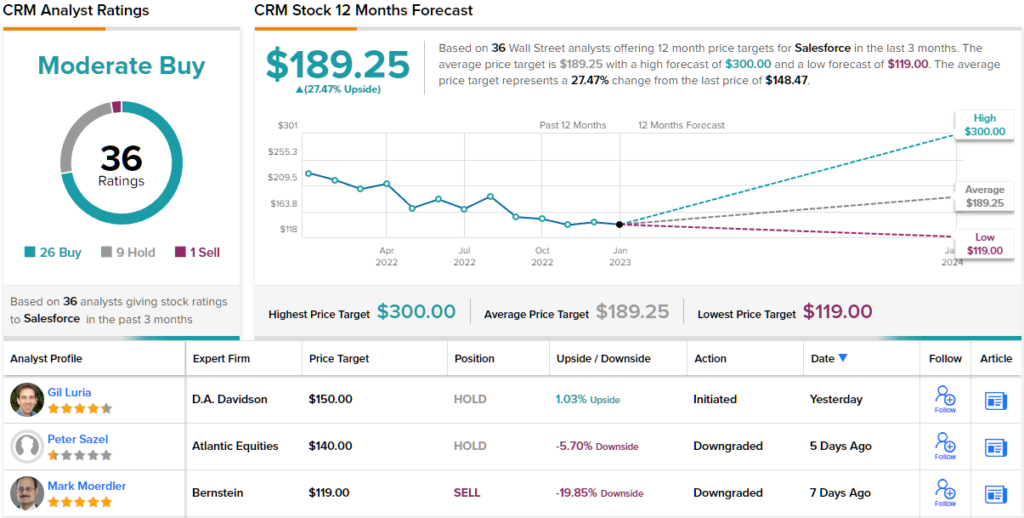

Salesforce, Inc. (CRM)

The first Goldman pick we’re looking at is software giant Salesforce. The company is a customer relationship management (CRM) specialist, providing software and applications that help its clients offer a better level of service to their own customers. Services run the gamut from support to analytics and relationship intelligence to personalized customer service, sales, and everything in between. Salesforce is one of the biggest software providers in the world, boasting a market cap north of $148 billion.

That said, like many other tech companies, recent times have been no easy ride, and the company only recently announced a 10% reduction to its workforce. Additionally, several execs have been handing their notice in over the past few months, amongst them co-Chief Executive Bret Taylor, who said he will leave his post at the end of January.

That announcement was made in tandem with the release of the company’s FQ3 results (October results). Salesforce delivered revenue of $7.84 billion, amounting to a 14.3% year-over-year uptick. Adj. EPS reached $1.40, easily trumping the Street’s $1.22 forecast. For the outlook, the company called for revenue for the fiscal fourth quarter to be in the range between $7.9 billion and $8.03 billion, just missing Wall Street’s call for $8.02 billion at the midpoint.

Despite the challenging environment, Goldman Sachs analyst Kash Rangan sees plenty of potential for investors to grab onto.

“We see a constructive set up for Salesforce when macro hurdles unwind and the company comes off a challenging period that includes management departures, new shareholder involvement and execution missteps within Mulesoft and Tableau… We think revenues and margins have the potential to double in the next 5-6 years, potentially quadrupling earnings in steady state. To that end, making inroads towards its operating margin expectations of 25% by CY25 can drive a higher re-rating of the stock, as seen with companies such as Microsoft, Adobe, Intuit and Autodesk, who’s valuations re-rated higher from significant step-ups in profitability,” Rangan opined.

Accordingly, Rangan rates CRM shares a Buy while his $300 price target suggests they will double in value over the coming year. (To watch Rangan’s track record, click here)

Rangan is the Street’s biggest CRM bull but plenty of other analysts are backing his case; based on 26 Buys vs. 9 Holds and 1 Sell, the stock receives a Moderate Buy consensus rating. At $189.25, the average target makes room for 12-month gains of ~27%. (See CRM stock forecast)

T-Mobile US, Inc. (TMUS)

From one giant to another. American wireless network operator T-Mobile US is the country’s second-largest wireless carrier and anticipated to see out 2022 with the customer count reaching 113.6 million. The company also prides itself with having America’s sole nationwide stand-alone 5G network, positioning it to be the 5G leader. T-Mobile’s market cap exceeds $186 billion and in sharp contrast to many other mega caps, that only grew in 2022’s bear.

The shares posted gains of 21% over the course of the year, boosted by strong earnings. In the last reported quarter, Q3, the company posted EPS of $0.40, which handily beat the $0.26 consensus estimate. The company also delivered its highest ever net additions for postpaid accounts (394,000).

The outlook was pleasing too, with postpaid net customer additions for the year anticipated to be in the range between 6.2 million and 6.4 million, above the previous guidance for 6.0 million to 6.3 million. In fact, at the start of the month, the company released preliminary results for 2022, which showed that it will attain 6.4 million total postpaid customers, exceeding the high end of that guide. For Q4, the company delivered postpaid net customer additions of 1.8 million, a feat that when combined, rivals AT&T and Verizon did not even manage.

That’s the sort of stuff Goldman’s Brett Feldman thinks makes TMUS a ‘Top Pick’ in 2023 even when taking into consideration last year’s gains.

“Despite material outperformance in 2022, we continue to see TMUS as the most attractive large cap growth stock in telecom and cable,” the analyst said. “Key catalysts that we see in 2023 include durable postpaid phone net adds (3mn vs. 3.1mn in 2022), even if sector growth slows, owing to ongoing churn improvement; sustained growth in core adjusted EBITDA (10% vs. 12% in 2022E) as merger (2020’s merger with Sprint) with synergies approach run-rate; and a near doubling in FCF/share as capex falls and buybacks ramp.”

To this end, Feldman rates TMUS shares a Buy, along with a $180 price target. The implication for investors? Upside of 22% from current levels. (To watch Feldman’s track record, click here)

Where do other analysts stand on TMUS? 14 Buys and 1 Hold have been issued in the last three months. Therefore, TMUS gets a Strong Buy consensus rating. Given the $182.62 average price target, shares could surge ~24% in the next year. (See TMUS stock forecast)

Warner Bros. Discovery (WBD)

Onto our third Goldman recommendation, Warner Bros. Discovery, a company that was formed as a merger of Discovery and WarnerMedia, after the latter was spun off by AT&T in April last year. The media and entertainment giant has an enviable portfolio spanning across film and TV; Warner Bros. film and television studios, DC Comics, HBO, CNN, Discovery Channel, the Cartoon Network, Eurosport, and plenty of other offerings all fall under the WBD moniker with some of the world’s most successful franchises such as Harry Potter, Lord of the Rings and Friends amongst its offerings.

The new entity is also combining its streaming services HBO Max and Discovery+, which together cater to almost 100 million paid subscribers. This launch is expected to take place in the spring.

The initial period following the merger was difficult and reflected in the company’s most recent earnings, for 3Q22. Revenue fell by 10.6% from the same period a year ago to $9.82 billion, while missing the Street’s call by $520 million. EPS of -$0.95 fell some way short of the -$0.45 anticipated by the analysts.

Following the readout, the shares took a beating, and overall they shed 61% in 2022. However, the stock is off to a flying start in 2023, having already delivered returns of ~39%.

There’s more to come, according to Goldman Sachs analyst Brett Feldman, who lays out the bullish case.

“We estimate that WBD is best positioned to drive EBITDA growth, ramp FCF and delever its balance sheet in 2023 as it pursues $3.5bn of merger synergies and relaunches its flagship streaming service,” Feldman said. “As such, while we expect investors to continue to debate the long-term outlook for traditional media companies, we see the risk/reward skew for WBD as most attractive vs. its peer group with key execution catalysts (merger milestones, streaming relaunch) largely within management’s control.”

These comments form the basis of Feldman’s Buy rating while his $19 price target implies 12-month share appreciation of ~44%.

And what about the rest of the Street? Based on 5 Buys and Holds, each, plus 1 Sell, the stock claims a Moderate Buy consensus rating. Going by the $16.28 average target, investors will be sitting on returns of 23% a year from now. (See WBD stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.