What’s more critical for the stock market’s health than the outcome of the presidential election? A COVID-19 vaccine, so says Goldman Sachs.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

With Q3 earnings season kicking into gear this week, the firm believes the virus’ effect on fundamentals should be the focus, as opposed to the race to the White House. “The vaccine represents a more important factor than the election result for the path of equities… The consequences of the semi-frozen economy on an uneven road to recovery will be in Q3 results,” Goldman Sachs’ U.S. equity strategist David Kostin commented.

Even though elections are a source of uncertainty, research analysts from Goldman Sachs found just a 4% difference in EPS if President Trump is re-elected or the Democrats come out on top. Based on the firm’s analysis, an increase in fiscal spending that is partly funded by increased tax revenue would “boost economic growth, and help offset the earnings headwind from high tax rates.”

Taking this into consideration, our attention turned to two stocks that Goldman Sachs thinks have outsized growth prospects, with the firm’s analysts forecasting at least 90% upside potential for each. Using TipRanks’ database, we found out both tickers also sport a “Strong Buy” consensus rating from the rest of the Street.

Athira Pharma (ATHA)

Applying cutting-edge approaches to neurodegenerative diseases, Athira Pharma wants to improve the lives of patients from all over the world. Given the potential of its asset in Alzheimer’s disease (AD), Goldman Sachs is pounding the table.

ATHA made its public market debut on September 18, with the first trade coming in at 17.4% above the IPO price. Raising $204 million, the company sold 12 million shares instead of the 10 million that was originally expected.

Writing for Goldman Sachs, analyst Graig Suvannavejh points to its lead candidate, ATH-1017, which is a small molecule activator of HGF/MET currently being evaluated in a Phase 2/3 trial as a treatment for mild-to-moderate AD, as a key component of his bullish thesis.

The analyst doesn’t dispute that AD is a difficult indication to address, but tells clients he has high hopes for ATHA. “We’re fully cognizant of the history of AD drug development, and its well documented past of high failure rates. As such, AD-focused companies like ATHA should be considered as having high risk. However, as there still remains a significant lack of effective drugs for AD, we believe alternative approaches to treating AD have merit,” he explained.

In the past, the most common therapeutic approaches to AD have been those focused on the belief that the accumulation of disease-causing proteins in the brain leads to AD. However, AD therapeutics based on targeting amyloid have all failed in clinical trials to demonstrate efficacy, with monoclonal antibody (mAb) approaches that target tau, another protein that aggregates in the brains of AD patients, also failing.

So, ATHA’s differentiated approach makes it a stand-out, in Suvannavejh’s opinion. Looking at the therapy’s mechanism of action (MOA), it is based on HGF/MET agonism, a strategy that hasn’t been studied in AD before. Additionally, Suvannavejh argues the FDA’s recent decision to review Biogen’s aducanumab for approval even though it was prematurely discontinued in two large Phase 3 studies due to futility is a “sign of a positive regulatory backdrop.”

On top of this, the company is applying a new thinking to AD clinical trials. It will use a non-traditional technique (EEG) in order to measure improvements in the brains of AD subjects, and a novel clinical trial end point (Global Statistical Test/GST) that will evaluate the efficacy. It is based on both the ERP biomarker and more traditional efficacy measures (e.g., ADAS-Cog).

Weighing in on this, Suvannavejh stated, “With this entirely innovative way of thinking in mind, we think it’s critical to acknowledge that FDA has already provided its sign off to ATHA’s novel clinical trial plan — which importantly also reduces overall time and costs typically associated with AD drug development. Further, given our view that FDA may be experiencing a sense of urgency to get new AD therapeutics in the hands of patients, their caregivers and physicians, we believe the time is right for a candidate like ATH-1017.”

When it comes to the revenue potential for ATH-1017, according to Suvannavejh, neurodegenerative diseases represent one of the highest areas of unmet medical need, with it estimated that more than 5 million people over the age of 65 in the U.S. have AD. This number is expected to nearly triple by 2050, based on research from the Alzheimer’s Association. To this end, the analyst projects risk-unadjusted peak 2035 sales of $10.8 billion.

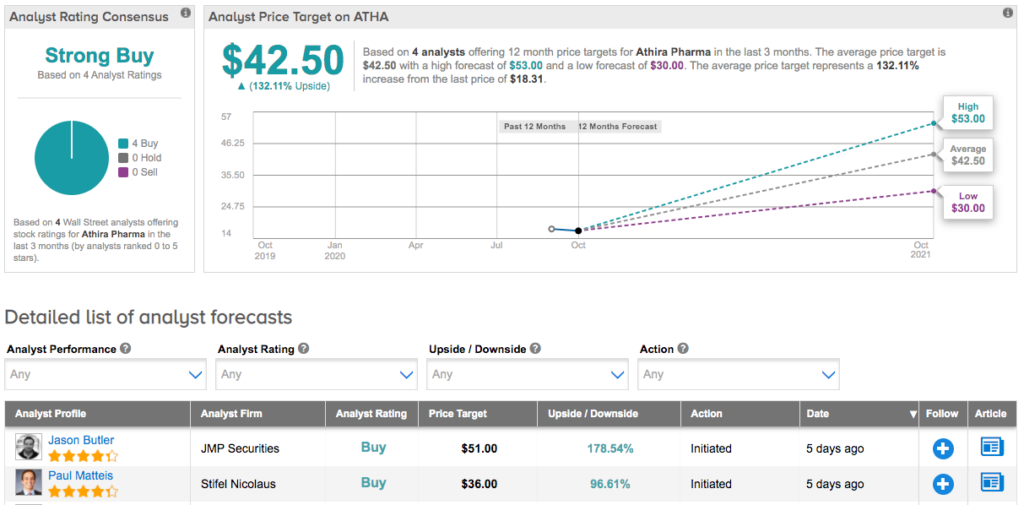

Everything that ATHA has going for it convinced Suvannavejh to initiate coverage with a Buy rating. In addition to the call, he set a $53 price target, suggesting 189% upside potential. (To watch Suvannavejh’s track record, click here)

Judging by the consensus breakdown, opinions are anything but mixed. With 4 Buys and no Holds or Sells assigned in the last three months, the word on the Street is that ATHA is a Strong Buy. At $42.50, the average price target implies 132% upside potential. (See Athira Pharma stock analysis on TipRanks)

Denali Therapeutics (DNLI)

Dedicated to defeating neurodegenerative diseases through rigorous therapeutic development, Denali Therapeutics is attracting significant attention from Wall Street. Ahead of a key data readout, Goldman Sachs has high hopes.

As the company gears up to report first proof-of-concept biomarker data for DNL310 in Hunter syndrome by YE20, the firm’s Salveen Richter likes what she’s seeing.

DNL310 is a recombinant form of the iduronate 2-sulfatase (IDS) enzyme engineered to cross the blood-brain barrier (BBB) using Denali’s enzyme transport vehicle (ETV) technology, which enables the trafficking of large molecules into the brain.

DNLI is set to publish initial data from Cohort A, and management expects the starting dose of 3mg/kg to reduce CSF GAGs by 50% at eight weeks. A second Cohort B will evaluate DNL310 in a broader range of patients, with dose escalation levels based on findings from Cohort A. Richter points out a 50% reduction in CSF GAGs was associated with a decrease in lipid lysosome and neurofilament light (NfL) chain accumulations that are associated with neuronal degeneration and injury.

“While this is the first in-human trial for DNL310, we see the pre-clinical data as strongly supportive of the anticipated therapeutic benefit and potential for GAG reduction in the CSF to drive downstream changes in lysosomal lipid and NfL accumulation (i.e. prevent neuronal dysfunction and injury) for improved cognition and function,” Richter commented.

It should be noted that the preclinical and early clinical data for JCR Pharmaceuticals’ JR-141, a BBB-penetrant fusion protein that also leverages receptor-mediated transcytosis to traffic iduronate-2-sulfatase (I2S) to the brain, de-risks the approach, in Richter’s opinion.

To this end, the five-star analyst believes positive DNL310 biomarker data could serve as proof-of-concept for DNLI’s transport vehicle (TV) technology. The platform’s modularity could allow for various large molecules to be transported across the BBB, for a range of other neurodegenerative indications like Parkinson’s disease (PD) and frontotemporal dementia (FTD).

On top of this, DNLI could leverage this delivery platform for antibodies, proteins or enzymes not currently in its own portfolio, with increasing interest on assets from Biogen, according to Richter.

In line with her optimistic approach, Richter stayed with the bulls, reiterating a Buy rating. She also bumped up the price target from $41 to $60. Investors could be pocketing a gain of 36%, should this target be met in the twelve months ahead. (To watch Richter’s track record, click here)

Looking at the consensus breakdown, 6 Buys and 2 Holds have been issued in the last three months. Therefore, DNLI gets a Strong Buy consensus rating. Based on the $51.17 average price target, shares could surge 16% in the next year. (See Denali Therapeutics stock analysis on TipRanks)

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.