Last year, the world experienced a significant shock in grain prices following Russia’s invasion of Ukraine, as two of the world’s largest grain exporters became entangled in an intractable conflict. The conflict spilled over into the Black Sea and halted the flow of grain to world markets. A recent deal between Russia and Ukraine promised to resume the grain flow, but it broke down after a new round of fighting in and around Crimea.

Protect Your Portfolio Against Market Uncertainty

- Discover companies with rock-solid fundamentals in TipRanks' Smart Value Newsletter.

- Receive undervalued stocks, resilient to market uncertainty, delivered straight to your inbox.

The result was another price spike and a grain shortage. The vital grain and oilseed markets have been facing headwinds from the Russo-Ukraine war, and recent drought conditions in North America’s farming regions haven’t helped.

A recent note from Roth MKM’s Brian Wright puts things into perspective. Despite the impact of the war on the grain trade and the drought’s effect on North American production, agricultural businesses stand to gain in the current conditions. The analyst points out several reasons why this would be so, including agribusiness’s resilience in the face of a recession and the sector’s current attractive valuations.

“We believe the coming decades are likely to witness more complex supply chains, resulting in more value-added margin expansion potential. We see this environment evolving due to a combination of the invasion of Ukraine, the increased assertiveness of China on the global stage, and the United States’ structural lack of financial discipline, which invokes challenges to its global leadership position. The emphasis on food security and this industry’s integral role in feeding the planet, we believe, will take on added importance,” Wright opined.

In addition to taking a broad-based look, Wright also tapped two specific agriculture stocks that stand to benefit in a global wheat shortage. Let’s take a closer look.

Bunge Limited (BG)

We’ll start with Bunge Limited, a major player in the agribusiness supply network. Bunge bills itself as the world’s leader in oilseed processing, and it is also an important producer in several other areas of food production and distribution, including specialty plant-based oils, fats, and proteins. The company’s products find their way into numerous food service applications, from cooking oils and flours to animal feeds, and from plant-based meat substitutes to infant nutrition. Bunge is also involved in the development of crop infrastructure and bio-based renewable fuel solutions.

On the operational side, this Missouri-based company has a global network. Bunge is integrated into the worldwide system of purchasing, storing, transporting, processing, selling, and distributing agricultural products and commodities for domestic use and export. The company’s operations span six continents, with grain elevators, oilseed processing facilities, and port terminals all located at strategic points. The company has allocated 36% of its processing capacity in South America, 26% in North America, and 23% in Europe. The remaining 15% is in the Asia-Pacific region.

In other words, Bunge has one of the largest global footprints of any major agribusiness. Bunge’s scale can be seen in a few simple numbers: the company has more than 300 facilities in over 40 countries and employs some 23,000 people.

One more number will round out the picture: $15.33 billion, Bunge’s revenue from 1Q23. That was down 3.5% year-over-year, but came in $150 million ahead of expectations. The firm’s non-GAAP EPS figure was reported as $3.26, or 2 cents per share better than the forecast.

In June of this year, Bunge announced it had entered into a ‘definitive agreement’ to merge with the privately held agribusiness giant Viterra. The transaction will include a transfer to Viterra shareholders of 65.6 million shares of Bunge stock as well as $2 billion in cash; Bunge will assume $9.8 billion in Viterra debt. When the transaction closes, Viterra’s ownership will control approximately 30% of Bunge’s stock. The merger is expected to close in the middle of next year.

Analyst Brian Wright takes a holistic view of Bunge, and is impressed by the company’s prospects. He notes its large footprint, and the opportunities presented by the Viterra acquisition, writing, “Given asset portfolio optimization in recent years, we expect less relative financial performance volatility going forward. In addition, BG shares should benefit from a greater growth profile given its favorable geographic profile with more exposure to higher growth South America. More consistent margins going forward should improve the company’s relative valuation discount.”

“Viterra acquisition diversifies geography footprint and crop exposures while enhancing scale. The transaction catapults BG ahead of publicly-traded peer ADM to the second largest agribusiness solutions company globally and increases Bunge’s merchandising, grain handling and logistics assets while diversifying Bunge’s footprint with more assets in the United States, Canada, Australia, Europe, and Argentina,” the analyst added.

Looking ahead, Wright sees reason for a Buy rating on BG shares, and his $138 price target implies room for a 27% upside on the one-year horizon. (To watch Wright’s track record, click here)

Looking at the consensus breakdown, 5 Buys and 2 Holds have been published in the last three months. Therefore, BG gets a Moderate Buy consensus rating. The stock is trading for $108.75, and its $122.57 average price target suggests an upside of ~13% in the months ahead. (See BG stock forecast)

Archer-Daniels-Midland Company (ADM)

Next up is Archer-Daniels-Midland, or ADM, one of the world’s largest agricultural companies, with a market cap of $47.3 billion and more than $100 billion in annual revenues.

This powerhouse company controls a network of crop procurement facilities and production plants, where it is working to develop solutions for healthier living through better food. The firm is also working on new ways of replacing petroleum-based products with plant-based substitutes. ADM’s expertise extends worldwide, making significant contributions to food processing and efficient supply chain management on a global scale.

ADM’s business is focused on four main segments: human nutrition, animal nutrition, pet nutrition, and industrial biosolutions. These four fields cover most possible uses for the plants and crops cultivated in the world’s farms, while maximizing beneficial uses and minimizing waste. Understanding that agriculture is vital to human existence, ADM is working to make it both more productive and sustainable.

The company reported its 2Q23 financial results earlier this week, and showed a top line of $25.2 billion. This was down 7.7% year-over-year, and was $520 million below estimates. At the same time, earnings showed a solid beat; the non-GAAP EPS was reported at $1.89 per share, or 30 cents per share ahead of the forecast.

Investors should note that ADM has a strong commitment to returning capital to shareholders. In June, the company paid out a dividend of 45 cents per common share, or $1.80 annualized. This yielded 2%, about in-line with the market average, and together with the company’s $1 billion in share repurchases in 1H23, marked a hefty capital return.

Checking in against with Roth’s Brian Wright, we find him appreciating AMD’s ability to bring value for shareholders. Wright says of the stock, “We believe the largest publicly-traded agricultural supply chain manager and processor’s strong return profile will continue to accrue significant value to shareholders as the company benefits from three enduring trends: food security, sustainability, and health and well-being. Shareholders should also benefit from continued substantive share repurchase activity.”

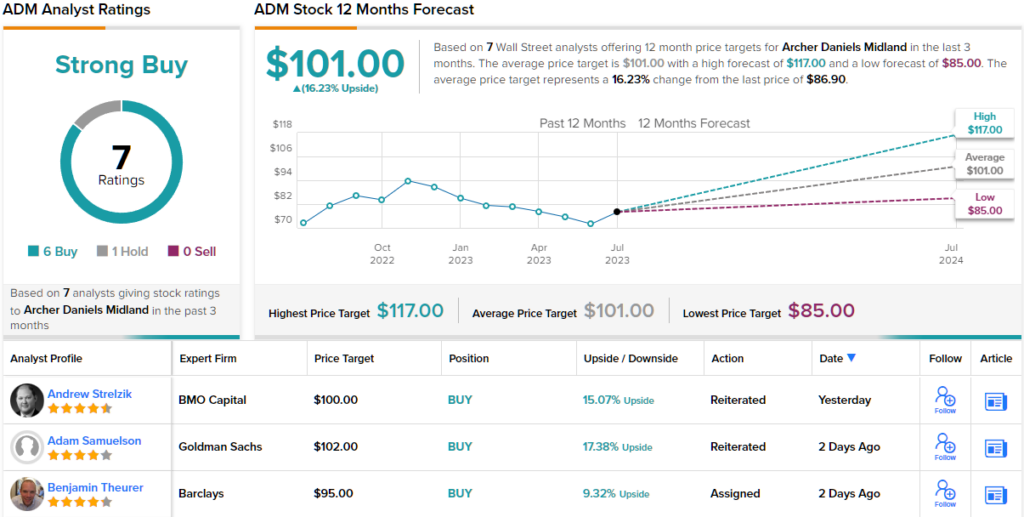

What does the rest of the Street have to say? 6 Buys and 1 Hold add up to a Strong Buy consensus rating. The average price target of $101 suggests a 16% upside potential over the one-year horizon. (See ADM stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.