General Mills (NYSE:GIS) is in the doghouse on Wall Street today, but don’t let the company’s dour (in other words, grim) financial outlook shake you out of a perfectly good trade. I am bullish on GIS stock because General Mills’ results were fairly good, and the company’s value-and-dividends profile is hard to resist.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

General Mills is a giant in the U.S. consumer packaged foods industry. Some of the company’s famous food brands include Cheerios, Häagen-Dazs, Green Giant, Wheaties, and Nature Valley.

GIS stock is usually considered a safe stock, but it hasn’t been very safe to invest in General Mills in 2023. This could change in the coming year, though, as the market should rotate back into consumer-defensive names eventually. Besides, the market’s dislike of General Mills today could turn on a dime, as the company actually posted Street-beating earnings recently.

General Mills Warns of “Value-Seeking Behaviors”

All in all, General Mills’ results for the second quarter of Fiscal Year 2024 weren’t bad. Yet, investors undoubtedly found it off-putting when General Mills CEO Jeff Harmening warned that he’s “seeing consumers continue to display stronger-than-anticipated value-seeking behaviors” throughout the firm’s key markets.

In other words, due to high inflation this year, the American consumer isn’t as resilient as some optimists might have assumed. Possibly, food shoppers are finally starting to push back against manufacturers’ price increases.

General Mills’ management may have had this in mind, along with expectations of a “slower volume recovery,” when it lowered its full Fiscal Year 2024 organic net sales growth outlook. Management’s prior guidance was for revenue growth between 3% to 4%, but now it’s calling for revenue growth between -1% and flat for the year.

In a time when the market has been spoiled by hyper-growth technology mega-caps, investors didn’t appreciate General Mills’ honest assessment of the full year’s sales outlook. Consequently, GIS stock fell by 3.6% today.

Furthermore, General Mills’ previous product price hikes may have had a negative impact on the company’s revenue. In Q2 FY2024, its revenue declined by 2% year-over-year to $5.1 billion and missed the consensus estimate by $250 million. It’s not a huge miss, but again, the market is spoiled in 2023.

On the other hand, General Mills reported quarterly earnings of $1.25 per share, up 14% year-over-year in constant currency. This bottom-line result actually beat the Street’s estimate by $0.09 per share, so General Mills seems to have had a decent quarter despite the consumers’ “value-seeking behaviors.”

Finally, it’s worth noting that, on a year-over-year basis, General Mills’ Q2-FY2024 gross margin increased by 170 basis points, and the company’s operating profit margin grew by 50 basis points. So, while General Mills’ product price hikes certainly didn’t make the shoppers happy, they may have contributed to General Mills’ margin improvement.

General Mills Stock: Low Beta, High Yield, Good Value

While General Mills’ results paint a mixed picture and the company’s sales outlook isn’t very positive, GIS should still appeal to passive-income investors and value seekers. Plus, if you’d like to diversify your high-flying tech-sector holdings with a slow mover, adding a few General Mills shares isn’t the worst thing you could do.

First of all, General Mills stock has a five-year monthly beta of just 0.23. This suggests that the stock has historically tended to move slower than the overall stock market.

Second, assuming that General Mills doesn’t alter its quarterly dividend payments of $0.59 per share, the company should provide a forward annual dividend yield of 3.6%. In comparison, the average dividend yield for the consumer defensive sector is 2.13%.

Finally, General Mills stock seems to offer decent value during a time when good value is hard to find. The company’s GAAP P/E ratio is under 16x. Meanwhile, the sector median P/E ratio is 20.7x.

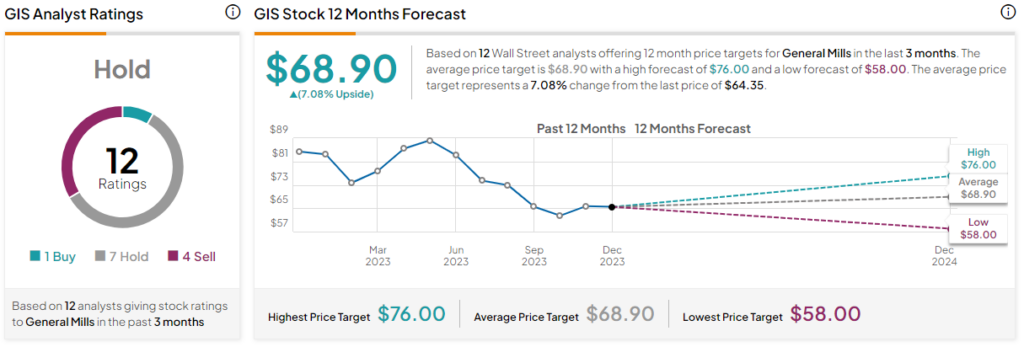

Is GIS Stock a Buy, According to Analysts?

On TipRanks, GIS comes in as a Hold based on one Buy, seven Holds, and four Sell ratings assigned by analysts in the past three months. The average General Mills stock price target is $68.90, implying 7.1% upside potential.

Conclusion: Should You Consider GIS Stock?

General Mills stock hasn’t been a good performer in 2023. However, it feels like the market has already priced in its disappointment with the emergence of consumers’ “value-seeking behaviors.” Besides, General Mills shares can help investors diversify their holdings and collect some decent dividends in 2024.

Is it possible that a tech-stock-obsessed market will come to appreciate General Mills’ value-and-yield proposition next year? Maybe there will be a “great rotation” into consumer-defensive names and especially GIS stock — no guarantees, but it’s a possibility. Therefore, I feel it’s a good time to consider a moderately-sized share position in General Mills.