FuboTV stock (NYSE:FUBO) is steadily advancing toward profitability, igniting optimism among investors about its investment potential. Despite consistently posting robust revenue growth, the sports streaming service’s shares have faced challenges recently due to a lack of profitability. This has left investors rather disheartened. However, with the prospect of achieving a positive bottom line drawing near, FUBO’s investment outlook appears more promising than ever. Consequently, I am bullish on the stock.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Industry-Leading Growth Metrics Despite Challenges

FUBO’s Q3 results not only demonstrated remarkable growth metrics but also underscored its resilience in a challenging and saturated streaming landscape. It’s a market where the main players like Netflix (NASDAQ:NFLX), Disney (NYSE:DIS), Amazon (NASDAQ:AMZN), and AT&T (NYSE:T) and their streaming divisions have struggled to impress lately. Even Netflix’s Q3 results, which highlighted a resurgence in growth, still fell short of the outstanding figures the company once routinely achieved a few years ago.

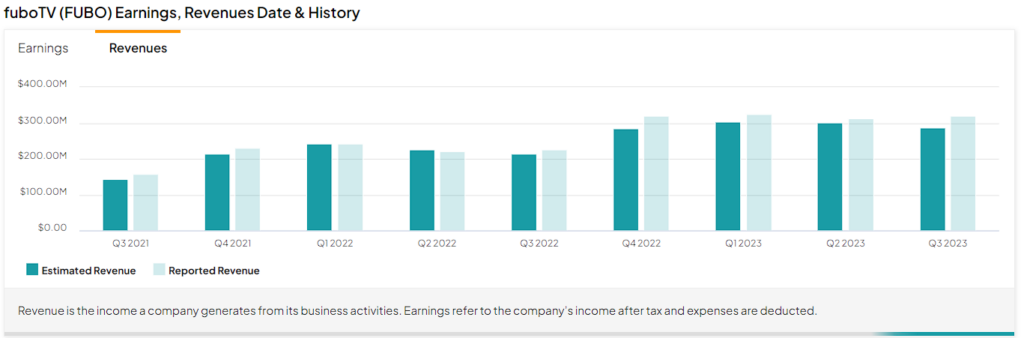

The intense competition and the battle for consumers’ attention have led to higher churn rates and a general lack of pricing power across the board. In contrast, FUBO, with its distinctive sports-oriented live SVOD model, has managed to transcend these challenges. The company posted revenue growth of 43% in Q3, reaching $320.9 million. This rate mirrored the strong momentum observed in the previous quarter.

FUBO’s strategic emphasis on live sports has allowed it to carve out a niche in the market, even amid challenging conditions. Driving revenue growth was the 20% increase in subscribers, totaling 1.477 million. Revenue growth was further fueled by a substantial 17% rise in average revenue per user (ARPU) to $83.51, setting a new record for the company. In my view, these metrics unmistakably signify robust consumer demand for FUBO’s services.

Additionally, a noteworthy highlight from Q3 was the North American segment generating $313 million in revenues, surpassing management’s earlier guidance of $275 million. Consequently, management revised its full-year estimates upwards, now anticipating revenues in the range of $1.319 billion to $1.324 billion for FY2023. This represents a 34% increase at the midpoint, up from the previous range of $1.26 billion to $1.28 billion.

Robust Top-Line Performance Propels FUBO Toward Profitability

FUBO’s robust top-line performance has propelled the company toward the eagerly anticipated realm of profitability, marking a pivotal stride for investors. The persistent challenge of attaining profitability had been a key factor in the stock’s post-pandemic downturn. However, with management expressing confidence in an imminent end to losses and the company’s latest results showcasing enhanced margins, investor faith in the stock has notably solidified.

FUBO’s strategic implementation of stringent cost controls, coupled with top-line expansion, has resulted in a praiseworthy uptick in margins—a direct alignment with management’s objectives. Notably, in Q3, the company’s adjusted EBITDA margin underwent a substantial improvement, narrowing from -36.9% to -19.2%. This positive shift was driven by a remarkable 884 basis points expansion in gross margins to 6%.

Overall, I believe that this substantial improvement serves as compelling evidence that FUBO’s business model is indeed scalable, dispelling past doubts on this front. While skeptics may raise concerns about the company’s persistent losses, it is crucial to highlight the substantial progress made. Operating losses for the quarter amounted to $83.3 million, a noteworthy improvement compared to the previous year’s figure of $103.6 million.

The pivotal question, however, revolves around the sustainability of these losses. Thankfully, fuboTV’s management, in a statement during the Q3 earnings call, reassured investors by stating, “We closed the year with $266 million in cash…and we believe [we] have sufficient liquidity to fund our current operating plan as we progress towards our 2025 goal.” This assertion strongly suggests that the need for additional capital is unlikely, mitigating the prospect of further dilution or damage to the balance sheet.

Is FUBO Stock a Buy, According to Analysts?

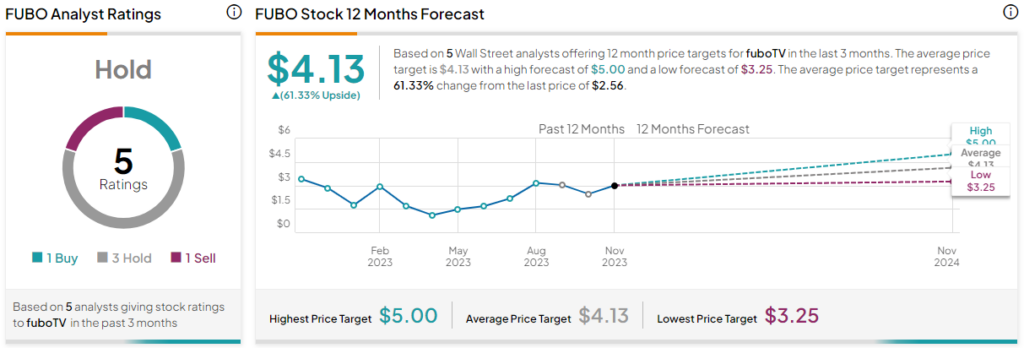

Regarding Wall Street’s view on the stock, FUBO features a Hold consensus rating based on one Buy, three Holds, and one Sell assigned in the past three months. At $4.13, the average FUBO stock price target implies 61.3% upside potential.

The Takeaway

In conclusion, FuboTV’s steadfast journey toward profitability signals a promising outlook for investors. Despite challenges in a competitive streaming landscape, FuboTV’s Q3 results showcased impressive growth metrics, highlighting its resilience and strategic positioning in the market.

The company’s focus on live sports and robust top-line performance, coupled with improving margins, instills confidence in its 2025 cash-flow-positive plan. Along with management’s reassuring comments, I can see FuboTV emerging as a bullish investment, shedding away earlier doubts and positioning itself for a promising future.