On the surface, gold royalties and streaming specialist Franco-Nevada (NYSE:FNV) appears to be an incredibly risky idea. Due to a critical issue at one of its key mines, FNV has heavily underperformed its rivals in the broader precious metals industry. Nevertheless, an unexpected reversal of fortune could create a positive feedback loop from gamma squeeze conditions. It’s an extremely speculative idea. Nevertheless, I’m bullish on FNV stock because the backdrop seems favorable for a recovery.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

FNV Stock May be Signaling a Reversal of Fortune

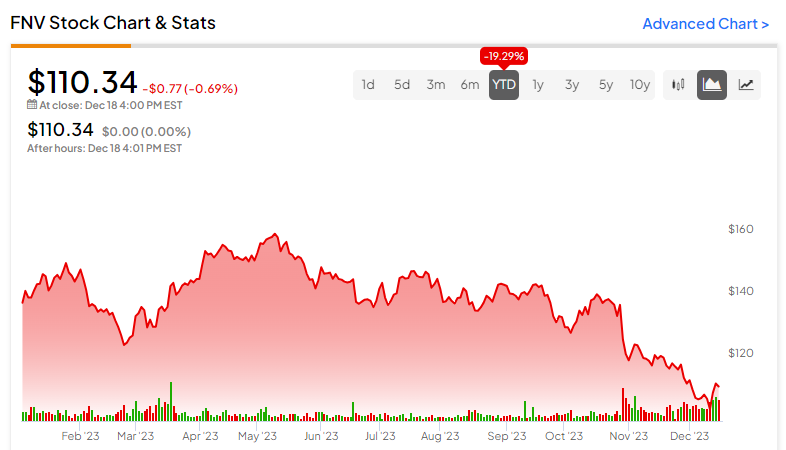

At first glance, FNV stock would not normally inspire confidence. Since the start of the year, it has given up almost 20% of its value. In contrast, gold and silver streaming giant Wheaton Precious Metals (NYSE:WPM) practically prints almost the opposite performance: up 22% on a year-to-date basis. Still, contrarian speculators could help contribute to Franco-Nevada’s reversal of fortune.

Primarily, that’s because Franco-Nevada is not an inherently flawed enterprise. One of the key mines with which the company partners – called Cobre Panama – incurred significant issues. Recently, the Panamanian government announced that it would shut down the mine after several weeks of public protests calling for its closure, according to a Bloomberg report. Understandably, the matter dogged FNV stock, leading to its value erosion.

Still, the Cobre Panama controversy is an unexpected headwind that’s not of Franco-Nevada’s doing. So, forward-looking investors may end up taking a shot on FNV stock, thanks to its perceived de-risked profile. Even better, options flow data shows that on December 14, the only big block transaction that materialized for the month so far was for a bought call option, specifically, 573 contracts of the Jan 19 ’24 120.00 call.

Now, when large purchases of call options materialize, someone – usually a market maker – must take the opposite side of the wager. In this case, the counterparty is short FNV stock because it sold the aforementioned calls.

Here’s where the speculation part comes in. Should more traders buy call options, the market maker’s negative delta exposure expands. In simple terms, negative delta represents the measure of a call seller’s losses should the underlying stock’s price rise.

Essentially, increased bullish speculation could force the market maker to buy the underlying security to hedge the negative delta, creating a positive feedback loop (a gamma squeeze) among optimistic gamblers.

Franco-Nevada Offers Compelling Fundamentals

To reiterate, the notion of a surge in FNV stock is speculative. It’s also possible that investors could prefer other precious metal investments, leaving Franco-Nevada in the cold. Nevertheless, the fundamentals undergirding the company suggest that it’s worthwhile to keep it on the radar.

First, BMO Capital analyst Jackie Przybylowski continues to maintain a Buy rating on FNV stock. While she acknowledges the impact that the Cobre Panama closure will have on Franco-Nevada’s production and stream volumes, she believes that the company’s diverse and cost-effective exposure to precious metals will help it remain a compelling investment.

Specifically, Przybylowski anticipates rising gold and copper prices along with increased demand for growth-oriented enterprises. Also, the BMO analyst isn’t alone in maintaining an optimistic framework for FNV stock.

Second, it’s not at all unreasonable for investors to believe that the underlying commodities could shoot higher in 2024. With the Federal Reserve signaling an open-minded approach regarding interest rate cuts next year, reduced borrowing costs could help boost the commodities sector. If so, the narrative may lift all boats in the precious metals space.

However, with FNV stock lagging behind its peers, it would simply look more attractive to bargain hunters. Therefore, the prospect of FNV reversing its bearish print offers some measure of credibility.

Greater Financial Predictability Offers Another Nod

For those sitting on the fence with Franco-Nevada, the predictability inherent in its royalties and streaming business model could help move the needle favorably. Unlike pure-play mining enterprises, Franco-Nevada offers financial consistency, which may carry a premium during these uncertain times.

For example, in the company’s third-quarter earnings report, it posted a gross margin of 62.2%. Admittedly, this figure slipped a bit against a year-over-year comparison. However, it’s right in line with the gross margin seen during the past several quarters. In Q4 2020, its gross margin came in at 62.5%. This consistency stems from pre-arranged deals in the royalties and streaming contracts.

In contrast, profit margins can be all over the map for direct mining enterprises due to dynamic factors such as volatile gold prices. With many investors worried about lingering uncertainties, FNV stock offers a more palatable exposure to the gold market.

Is FNV Stock a Buy, According to Analysts?

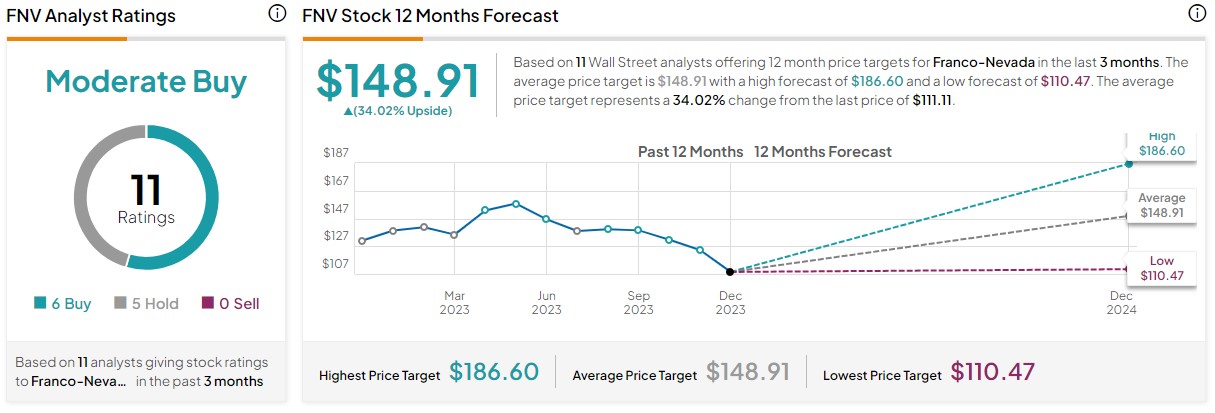

Turning to Wall Street, FNV stock has a Moderate Buy consensus rating based on six Buys, five Holds, and zero Sell ratings. The average FNV stock price target is $148.91, implying 34% upside potential.

The Takeaway: A Reversal for FNV Stock Is Not an Unrealistic Proposition

Franco-Nevada, hit hard by a mine closure, lags behind its precious metal peers. However, gold price increases and FNV’s strong fundamentals could trigger a gamma squeeze fueled by bullish options buying, attracting contrarian investors. While speculative, FNV’s diversified portfolio, analysts’ Buy ratings, and predictable revenue from royalties offer compelling reasons to keep it on the radar, especially if commodities boom on potential Fed rate cuts.