Foot Locker (FL) is an athletic footwear and apparel retailer. We are bullish on the stock as its valuation seems too cheap to ignore.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Measuring Efficiency

Foot Locker needs to hold onto a lot of inventory in order to keep the business running. Therefore, the speed at which a company can move inventory and convert it into cash is very important in predicting its success.

To measure its efficiency, we will use the cash conversion cycle, which shows how many days it takes to convert inventory into cash. It is calculated as follows:

CCC = Days Inventory Outstanding + Days Sales Outstanding – Days Payables Outstanding

Foot Locker’s cash conversion cycle is 40 days, meaning it takes the company 40 days for it to convert its inventory into cash. In the past several years, this number has declined, meaning that the company has become more efficient.

In addition to the cash conversion cycle, let’s also take a look at Foot Locker’s gross margin trends. Ideally, we would like to see a company’s margins expand each year. This is, of course, unless gross margins are already very high, in which case it is acceptable for them to remain flat.

In Foot Locker’s case, gross margins have declined in the past several years from the low 40s to 34.4%. This is not ideal because it means that competitors are chipping away at its competitive advantage.

Respectable Returns on Capital

Often times when looking at a “deep value” stock, the stock may have fallen into deep value territory because the underlying business isn’t all that great. However, this isn’t the case for Foot Locker.

Although we prefer companies with very high returns on capital, Foot Locker’s numbers are still respectable. This is especially true when considering its low valuation, which we will talk about later.

When looking at its cash return on invested capital (measured as free cash flow divided by average invested capital), this number came in at 11.2% for the past 12 months. Foot Locker’s CROIC has always been over 10% in the past 10 years.

Considering its weighted average cost of capital (WACC) is 9%, this classifies FL as a value creator. If its returns were under 9%, it would be considered a value destroyer.

Risks

Recent developments may negatively impact the cash conversion cycle going forward. A material risk that the market is currently concerned about is Nike’s (NKE) decision to reduce the number of products it will supply to Foot Locker. This is part of Nike’s move to shift more of its sales direct-to-consumer.

Investors and some analysts believe that this development will translate into long-term headwinds for the company. In its most recent quarter, Nike products made up 65% of sales, and the company now expects this number to fall to 55% by the end of 2022.

However, the recent sell-off and analyst sentiment may be overblown. Yes, Nike products are popular, but they aren’t the only brand that’s growing. Other brands like Adidas and Puma also performed well in 2021 for Foot Locker.

Therefore, it might not be such a bad thing if the company further diversifies its product mix going forward. This would allow it to reduce the impact of similar events if another brand were to attempt the same thing.

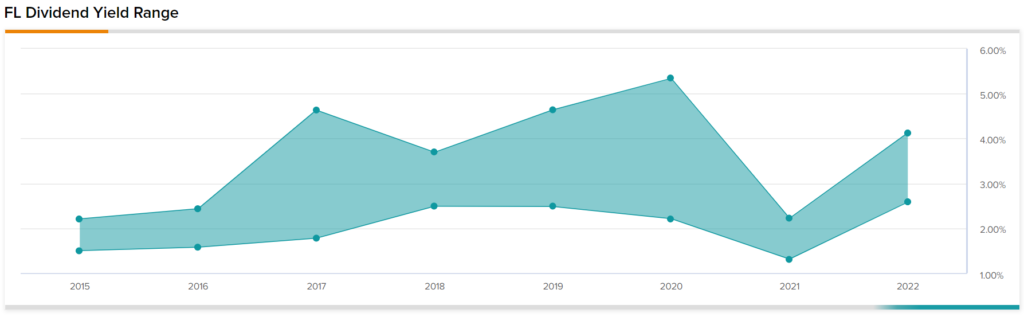

Dividends, Buybacks

Foot Locker’s current dividend yield is 3.8%, with a forward yield of approximately 5.5%.

Taking a look at its historical dividend payments, we can see that its yield range has been choppy in the past several years.

In addition, the company approved a $1.2-billion share repurchase plan, which is huge considering that its market cap is $3 billion.

This means that if earnings stay the same, the earnings per share figure could increase by 42% (assuming the share price stayed the same). Earnings are expected to drop substantially in the next year, but the buybacks should offset some of this drop.

Regardless, based on forward EPS estimates of $4.88 (which could end up coming in higher if buybacks are strong), the stock is trading at a forward P/E ratio of just under 6.4x. This multiple seems very cheap to us.

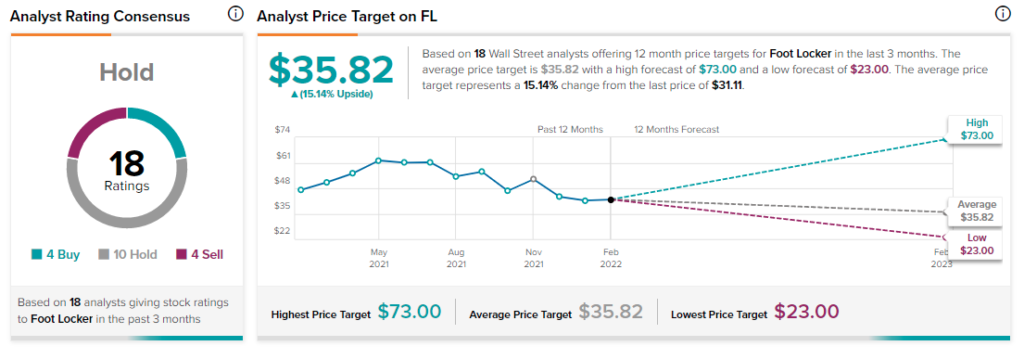

Wall Street’s Take

Turning to Wall Street, Foot Locker has a Moderate Buy consensus rating, based on four Buys, 10 Holds, and four Sells assigned in the past three months.

The average Foot Locker price target of $35.82 implies 15.1% upside potential.

Final Thoughts

Foot Locker has seen a huge sell-off recently, which may have been an overreaction by the market. Despite the headwinds it is facing, its juicy forward yield and huge buyback authorization can be a potential catalyst for share price appreciation. It is also a value creator when looking at its returns on invested capital.

We are bullish on the stock at current prices in the long term, although the short-term stock price may still see some pressure.

Download the TipRanks mobile app now

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Read full Disclaimer & Disclosure