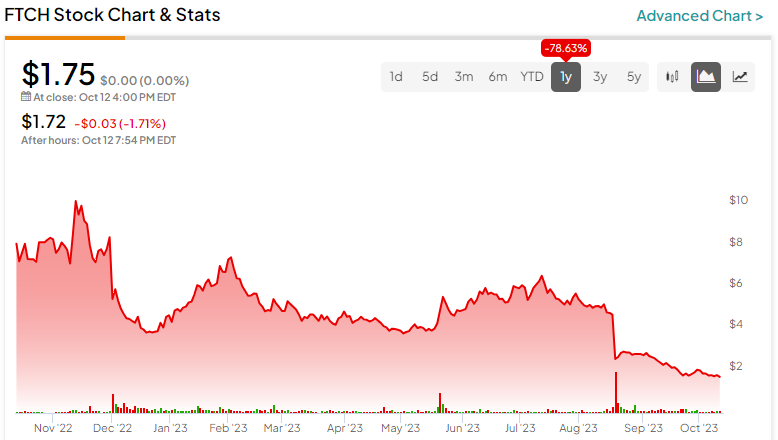

Farfetch stock (NYSE:FTCH) has collapsed in recent months. The online luxury fashion marketplace has seen its shares decline more than 78.6% over the past year. This disaster can be attributed to the company’s failure to scale its operations profitably despite the luxury industry’s resilience in a challenging macroeconomic environment. With steep losses continuously eroding its cash position and destroying shareholder value, this trend is likely to persist. Thus, I am bearish on the stock.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Strong Demand for Luxury Goods Sustains Solid Revenues

Before delving into Farfetch’s financial challenges, it’s crucial to underscore the company’s commendable revenue performance. Despite grappling with financial setbacks, Farfetch has consistently navigated turbulent economic waters powered by the unwavering demand for luxury goods. The resilience of the luxury industry has proven instrumental, ensuring a robust influx of traffic into Farfetch’s marketplace and a sustained appetite for its premium brands.

Contrary to common assumptions, the luxury industry exhibits remarkable resilience, sustaining elevated interest in Farfetch’s offerings among affluent consumers. While a challenging macroeconomic landscape typically dampens consumer purchasing power, the dynamics shift when dealing with high-end products and wealthy clientele.

The conventional economic norms seem not to apply in the realm of luxury, as wealthy consumers remain relatively unaffected by economic downturns. In fact, challenging times often become fertile ground for the wealthy to amass even greater fortunes. Therefore, their spending habits remain largely unchanged, defying the patterns observed in the broader market during periods of economic uncertainty.

This narrative finds empirical support in Farfetch’s recent Q2 results, wherein the company reported gross merchandise value (GMV) of $1.03 billion. This implies year-over-year growth of 1.2%. In constant currency, GMV registered a modest 0.8% year-over-year growth, propelled by increased Marketplace orders and the commendable GMV expansion of Farfetch Platform Solutions (FPS).

Moreover, the company proudly announced a record-breaking active consumer count, reaching 4.1 million—a 7% increase year-over-year. Notably, the quarter witnessed an influx of over 550,000 new consumers, with a modest uptick in orders per customer contributing to a noteworthy 9% increase in overall orders.

This was partially offset by a 6% decline in average order value to $562. However, the company’s marketplace demonstrated its ability to attract substantial “foot traffic” even amid a challenging economic landscape. It proved its resilience even when customers had to adjust their spending habits.

Uncontrollable Spending Sends Cash Down the Drain

Despite Farfetch’s apparent resilience, the company’s unrestrained spending spree has led to a significant depletion of its cash reserves. This extravagant expenditure not only precludes the possibility of reporting substantial profits but has also resulted in considerable dilution, steadily eroding shareholder value.

To illustrate, the company posted a 4.9% increase in selling, general & administrative expenses (SG&A), totaling $456.4 million. This substantial amount, accounting for approximately 80% of its $572.1 million in revenues, raises questions about Farfetch’s prioritization of serving management over creating value for shareholders.

This concern deepens when considering the surge in Farfetch’s stock-based compensation (SBC), which soared from $58.1 million in Q2 2022 to $71.1 million in Q2 2023. It appears perplexing that management is boosting compensation while the company struggles for survival.

The cumulative impact of these expenditures manifests in Farfetch’s quarterly loss of $228.3 million, with cash and equivalents declining to $453.8 million by the end of June. This marks a significant decline from the $734.2 million at the close of Fiscal 2022, vividly highlighting Farfetch’s cash-bleeding predicament. Continuous cash bleeding means further dilution, as Farfetch will have to raise cash again sooner rather than later. Its excessive SBC also contributes to diluting shareholders over time, accelerating this issue.

Is FTCH Stock a Buy, According to Analysts?

Turning to Wall Street, Farfetch has a Hold consensus rating based on four Buys, eight Holds, and one Sell assigned in the past three months. At $5.78, the average FTCH stock forecast implies 230.3% upside potential.

Please be mindful that FTCH’s price targets have consistently seemed elevated when compared to both the current stock price and the fundamental financial position of the company. As a result, it is prudent to approach this forecast with a degree of skepticism and to consider it within the broader context.

Conclusion

In conclusion, Farfetch has navigated the luxury market’s challenging waters with commendable revenue performance. However, its failure to scale profitably and its unchecked spending have resulted in the decay of its balance sheet, the continuous dilution of shareholders, and, thus, steep share price losses. Despite the resilience of the luxury industry and positive metrics like increased consumer counts, the company’s prioritization of spending over shareholder value creation is evident.

Unfortunately, the escalating SG&A expenses and growing stock-based compensation raise concerns about management’s fiscal responsibility. In the meantime, Farfetch’s dwindling cash reserves underscore a perilous trend. As the company grapples with losses and cash depletion, I hold a bearish outlook on the stock.