Etsy (NASDAQ:ETSY) continues to benefit from strong consumer spending, which keeps driving lasting growth post-pandemic. The stock is still down about 66% from its all-time-high levels from November 2021, a time when most e-commerce stocks were trading at absurd valuations that were powered by their pandemic-driven growth.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

However, Etsy has managed to grow past its pandemic-induced numbers. Despite recent concerns of a slowdown in economic growth, consumers’ purchasing power remains very strong, resulting in the company achieving record revenues in its most recent quarterly results. Combined with shares still trading at attractive levels relative to the company’s future earnings projections, I am bullish on the stock.

Strong Consumer Spending is Driving Record Revenues

The success of Etsy can be heavily influenced by consumer spending and the level of disposable income that buyers have available. The distinctive handmade items and vintage gems showcased on Etsy’s marketplace are not exactly necessities. Their sales are mostly related to discretionary spending. This was greatly illustrated amid the pandemic when government checks and excess liquidity allowed consumers to overspend on such goods. Specifically, in Fiscal 2020 and Fiscal 2021, Etsy’s revenues grew by 110.9% and 35.0%, respectively.

With fears of a looming recession dominating the market last year, most investors expected a reasonable correction in Etsy’s revenues that would normalize the prior years’ trend. Yet, Etsy managed to grow past its already inflated numbers. Not only did the company post 10.2% growth in revenues in Fiscal 2022, but its Q4 results, in particular, were impressive as they implied an acceleration in its overall performance.

Specifically, in Q4, revenues came in at a record $807.2 million, up 12.6% year-over-year, including Etsy’s take rate (i.e., revenues divided by consolidated Gross Merchandise Sales) rising to 20%.

In the meantime, management’s guidance points toward another exciting year ahead. The company sees record Q1 revenues, which are expected to land between $600 million and $640 million, implying a year-over-year increase of about 7%.

To me, it’s impressive that Etsy continues to grow despite some of its biggest peers struggling. Let’s take Amazon (NASDAQ:AMZN), for instance, which acts as a bellwether for e-commerce sales. In Q4, Amazon’s product sales (total revenues minus AWS revenues) actually fell by 1.3%. Further, Amazon’s Q1 guidance, projecting year-over-year net sales growth of between 4% and 8%, suggests another quarter of declining product sales, given that most of the company’s growth is being carried by its Amazon Web Services (AWS) division, which saw 20% growth in Q4.

A Couple of Interesting Points Regarding Etsy’s Future Growth

There are also a couple of interesting points to make regarding Etsy’s future revenues. Firstly, the FED’s decision to hike rates by 25 basis points (bps) suggests that it believes the economy is strong enough to sustain the hike. In other words, the FED likely believes the economy should be able to sustain strong spending moving forward, which is good news for Etsy. If this wasn’t the case, we could have seen a pause in rate hikes (this is a more complicated matter, but this basic element holds true) in an attempt to fuel the economy.

Secondly, even if we were to see a decline in consumers’ purchasing power, Etsy’s sales could still be sustained at lofty levels or even grow further. This is because, apart from its core Etsy platform, the company also owns and operates a few more businesses, like Depop and Elo7. With these two platforms focusing on second-hand clothes and musical instruments, respectively, Etsy could benefit if consumers opt for used goods following lower disposable income.

Strong Profitability & Growing Buybacks: A Positive Catalyst

Etsy’s most vibrant catalyst for driving its stock higher in the near term is the company’s strong profitability and growing buybacks. At first glance, Etsy posted a net loss of $694.3 million in Fiscal 2022. However, this was only due to a $1.0 billion impairment charge in Q3.

On an adjusted basis, which excludes such non-cash items, the company’s adjusted EBITDA margin stood at a satisfactory 28% for the year. Management’s Q1 guidance targets a lower adjusted EBITDA margin of about 26% to 27%, likely due to higher marketing expenses, but again, margins remain at quite sufficient levels. In the meantime, analysts expect the company’s earnings per share to hit a new record of $4.69 by Fiscal 2024.

Etsy also appears to expect substantially improving earnings by then, as signaled by its rapidly growing share repurchases. In 2022, the company repurchased $425.8 million worth of stock, around 41% more than it did in 2021.

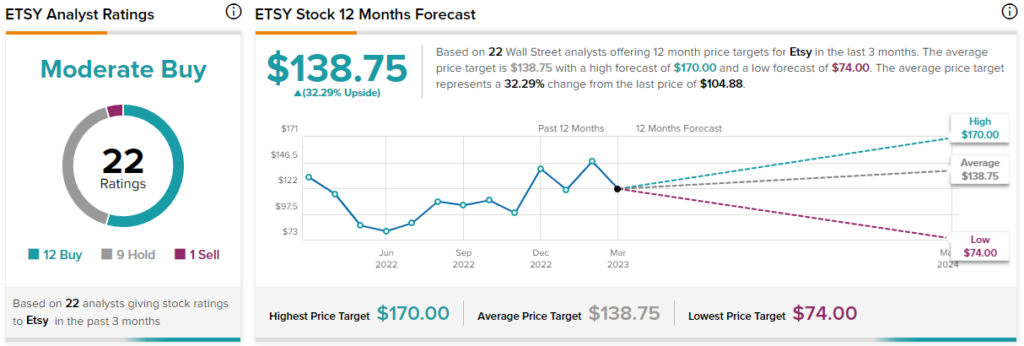

Is ETSY Stock a Buy, According to Analysts?

Turning to Wall Street, Etsy has a Moderate Buy consensus rating based on 12 Buys, nine Holds, and one Sell assigned in the past three months. At $138.75, the average ETSY stock forecast implies 32.3% upside potential.

The Takeaway

Overall, Etsy’s ability to sustain growing revenues on top of its pandemic-induced results is quite remarkable. This success can be attributed not only to strong consumer spending but also to the preference of consumers for its platforms.

In the short term, Etsy’s profitability is expected to take a hit. However, in line with Wall Street’s estimates for earnings per share of about $4.69 by 2024, Etsy’s profitability has lots of room for improvement. In fact, this particular estimate suggests a forward P/E of about 22.8 at the stock’s current price, which makes for a rather attractive multiple, in my view, despite this projection being two years ahead.