Estée Lauder (NYSE:EL) is an established giant in the beauty industry that comes with multiple attractive characteristics. While these characteristics have made investors fall in love with the stock, Estée Lauder seems to be wildly overpriced, even if the company performs better than investors currently anticipate it to. Therefore, don’t let the company’s beauty fool you into buying its overpriced stock. I am neutral on Estée Lauder.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

4 Reasons Why Investors Love Overpriced Estée Lauder Stock

Before assessing the stock’s valuation, it’s crucial to understand why investors have a certain type of love of Estée Lauder stock and are willing to pay a massive premium for it. It’s not a single reason but a powerful bundle of multiple attributes.

1. A Large and Growing Market

For starters, despite the beauty industry already being quite large and mature, it continues to grow steadily. For context, in 2015, the global beauty industry (including cosmetics, fragrances, personal care, and skin care) generated revenues of $458 billion. In 2021, it produced revenues of about $529 billion, and it’s expected to grow at a 3.8% CAGR from 2023 to 2027. This growth is predominantly being powered by a growing awareness of personal grooming and self-care, and one to certainly benefit from this trend is Estée Lauder, which is the second-largest company in the industry, only behind L’Oreal (OTC: LRLCY).

2. Strong Brand Recognition and Customer Loyalty

Another driving force that explains why investors are eager to be a part of Estée Lauder’s success story is its outstanding brand reputation and steadfast customer base. The company’s portfolio of brands includes major names such as M·A·C, Bobbi Brown, Jo Malone London, Darphin, and Editions de Parfums Frédéric Malle, among others, which are adored by millions of consumers around the world.

Strong brand recognition and customer loyalty can result in consistent cash flows for the company, as beauty products generate repeat sales. Consumers are also willing to pay a premium for renowned brands, which also allows the company to charge above-average prices and achieve superior margins compared to its competitors.

3. Recession-Proof Cash Flows

Additionally, investors have felt comfortable with paying a premium valuation for the stock due to the beauty industry being relatively recession-proof. People keep spending money on personal grooming and self-care even during economic downturns, as personal grooming and self-care are considered somewhat essential nowadays.

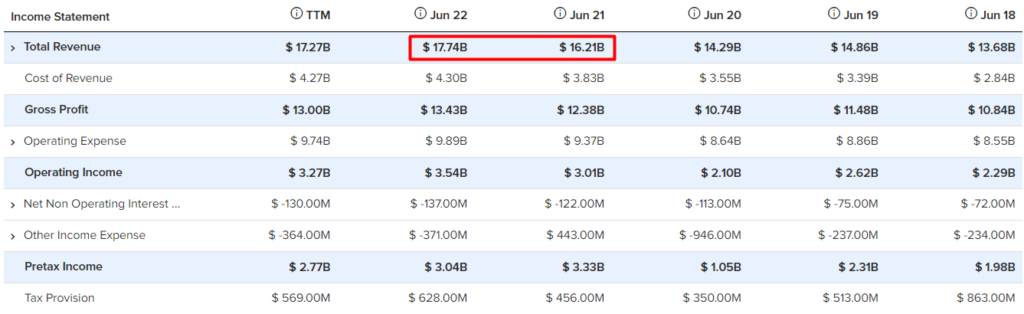

As a result, Estée Lauder’s revenues are likely not going to be impacted as much during such a scenario. This was demonstrated both during the Great Financial Crisis and the COVID-19 pandemic. In 2009, Estée Lauder’s revenues fell by just 7.6% from $7.9 billion in 2008 to $7.3 billion. By 2011, revenues had already shot past $8.8 billion. Further, in 2020, revenues declined by just 3.8% year-over-year to $14.3 billion due to the pandemic. Then in 2021 and 2022, the company continued to hit sustained top-line records, generating sales of $16.2 billion and $17.7 billion, respectively.

4. Proven Revenue and Earnings Growth Track Record

Finally, Estée Lauder has established a proven growth track record over the years, as illustrated by the quick comebacks and continued sales records in the above example. The company has increased its revenues by a compound annual growth rate (CAGR) of 6.2% over the past decade. Impressively enough, revenue growth has even accelerated lately, with its five-year revenues CAGR standing at 8.5%.

Besides its organic growth, Estée Lauder has grown through acquisitions as well. This past November, for instance, the company announced the acquisition of the luxury brand Tom Ford in a deal worth $2.8 billion.

Further, as I mentioned, the beauty industry enjoys high margins, especially Estée Lauder, due to its premium pricing capabilities. With its brands achieving economies of scale over time, net income growth has significantly outpaced revenue growth. To compare it with the above metrics, net income has grown at a CAGR of 10.8% over the past decade, while with stock buybacks reducing the share count during this period, earnings per share grew at a CAGR of 11.7% between Fiscal 2012 and Fiscal 2022.

Is EL Stock a Buy, According to Analysts?

Turning to Wall Street, Estée Lauder has a Moderate Buy consensus rating based on 16 Buys, five Holds, and one Sell assigned in the past three months. Despite analysts’ favorable ratings, the stock has likely run ahead of itself. At $257.94, the average Estée Lauder stock price prediction implies 0.6% downside potential.

Takeaway – The Problem is the Valuation

There is no doubt that investors’ love for Estée Lauder is well-justified, with the company featuring multiple monumental attractive characteristics. This fondness for the stock is reflected in the fact that shares have increased by more than 300% over the past decade and by 104% in the past five years.

Nevertheless, share price gains have outpaced the growth in Estée Lauder’s financials. Despite the company’s rapid revenue and earnings growth, as mentioned earlier, its revenues and net income have “only” grown by 63.8% and 134%, respectively, over the past decade. Accordingly, the stock has undergone massive valuation expansion. In fact, shares are currently trading at a forward P/E ratio of 46.7x, nowhere near the “normal” forward P/E ratio of around 20x to 25x that it historically carried.

Thus, even if the company massively outperforms the current consensus growth estimates, which forecast earnings-per-share growth of about 7% per annum over the next five years, the stock could face violent valuation headwinds. Does the stock deserve a premium? Yes, but nowhere near this absurd magnitude. Therefore, be wary of holding shares of Estée Lauder near its current levels.

Join our Webinar to learn how TipRanks promotes Wall Street transparency