Chewy stock (NYSE:CHWY) has experienced an endless plunge over the past two years, which may make the stock a prime M&A target. Although the online shop for pet supplies has not created much value for shareholders, it has made exceptional progress in expanding its subscriber base and revenues. This positions Chewy as an enticing acquisition target for a retail giant that could leverage Chewy’s progress in the pet industry to unlock efficiencies and turn it profitable. Thus, I’m bullish on the stock.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Who Could Be a Potential Chewy Acquirer, and Why?

Chewy emerges as an exciting acquisition target, especially for key players in the retail or e-commerce realm, like Amazon (NASDAQ:AMZN) or Walmart (NYSE:WMT). The appeal lies in Chewy’s ability to breed (pun intended) one of the most expansive and passionate customer bases within the pet industry. A big retailer would likely find this customer base highly valuable.

Why, you may ask? Well, in an arena as competitive as the pet industry, effectively managing customer acquisition costs is paramount, and Chewy has proven its prowess in this aspect. Consequently, companies that want to acquire customers in this space are willing to pay a hefty price (i.e., high customer acquisition costs).

Chewy has successfully navigated this challenge, having already set a robust foundation with 20.3 million active monthly customers. These customers, on average, contribute $543 per quarter to the company’s e-store. Clearly, pet owners happily open their wallets for their cherished companions. Pet supplies are also a recurring need, meaning that Chewy’s business model is quite predictable while enjoying high lifetime customer value.

Remarkably, Chewy’s revenues have consistently grown. In fact, they have grown over any 12-month period following the company’s initial public offering. This underscores the recurring revenues, long customer lifetime value, and the recession-resistant nature inherent in the pet industry.

In its most recent quarterly report, the company achieved a noteworthy 8.2% increase in revenue, reaching a substantial $2.74 billion. Notably, an impressive $2.09 billion, equivalent to 76.4% of the total revenue, was attributed to Autoship Customer Sales—an increase from the previous year’s 73.3%. Autoship sales specifically pertain to the revenue generated through Chewy’s subscription service, offering pet owners the convenience of customizable auto-reordering and deliveries.

This expanding subscription model not only ensures consistent and robust cash flows for Chewy but also contributes to an elevated customer lifetime value. The trust cultivated by Chewy through this platform emerges as an invaluable asset, especially in a fiercely competitive industry, fortifying its prowess in retaining customers.

Overall, it’s quite evident that Chewy’s compelling attributes, including its substantial share of recurring sales, extensive data on each pet owner, and dominant position in the pet industry, make it a highly appealing prospect for integration with the pet division of a retail giant.

A Potential Acquirer Could Solve Chewy’s Profitability Issues

In addition to the compelling advantage of enhancing a retailer’s customer acquisition efforts, the acquisition of Chewy holds the promise of resolving the company’s profitability challenges. The issue at hand is that Chewy’s margins are very thin due to the ultra-high competitive nature of the pet industry.

Demonstrating this point, the company has maintained an average gross margin of 28.3% and a net income margin of 0.1% over the last four quarters. Although the company is experiencing growth, its earnings are essentially at a breakeven point. By strategically addressing Chewy’s marketing costs, optimizing its distribution network for synergies, and bolstering pricing power, a retail giant has the potential to transform the company into a profitable entity.

Should the prospective acquirer successfully secure a 10% profit margin for Chewy, buying out the company at its current forward P/S ratio of a mere 0.8x has the potential to yield a highly favorable investment outcome. This underscores my conviction that the acquisition of Chewy would prove advantageous for both the acquiring entity and Chewy’s existing shareholders (as it will enable them to realize a premium in the process).

Is CHWY Stock a Buy, According to Analysts?

Regarding Wall Street’s view on the stock, Chewy has a Moderate Buy consensus rating based on 10 Buys, eight Holds, and one Sell assigned in the past three months. At $24.17, the average Chewy stock forecast implies 3.5% upside potential.

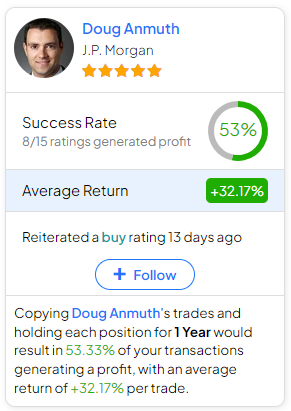

If you’re wondering which analyst you should follow if you want to buy and sell CHWY stock, the most accurate analyst covering the stock (on a one-year timeframe) is Doug Anmuth from JPMorgan (NYSE:JPM), with an average return of 32.17% per rating and a 53% success rate.

The Takeaway

In conclusion, Chewy’s stock performance in recent years, characterized by a prolonged decline, has paradoxically positioned it as an attractive M&A target. Despite its struggle to create shareholder value, Chewy has excelled in expanding its subscriber base and revenues, making it a compelling prospect for retail giants like Amazon or Walmart.

With a robust foundation, recurring revenues, and a subscription model fostering customer loyalty, Chewy’s integration with a retail giant could address profitability issues and unlock substantial value for both the acquiring entity and existing shareholders.