Adam Smith demonstrated the division of labor with the humble example of pin-making, but the idea was a big one, and today it permeates our economy at every level. It forms the basis of the modern assembly line – and of the contract services in the Engineering & Construction sector.

Contract services are a vital niche, covering the inevitable gaps between companies’ work roles and the expertise and capabilities of their work forces. E&C companies typically hold expertise in a narrow area, construction or telecom, for example, but need competent execution in related fields like energy build-outs or telecom human resources. Farming out those services allows for greater efficiency of action.

Looking at the sector, Sangita Jain, a senior equity analyst at KeyBanc, tells investors of the attributes she is looking for when considering investments in the segment. “We focus our investment recommendations on stocks that… are exposed to the energy transition theme and offer valuation upside, or have not yet benefited from the unlocking of federal spending dollars. We are not counting on any additional federal support, and to that end, our top picks do not rely on upcoming catalysts but rather on execution and valuation,” Jain explained.

Specifically, Jain is pointing out two contract service providers in the E&C segment. Using the TipRanks database, we’ve found that each of Jain’s ‘specialty contractor’ E&C picks gets a ‘Strong Buy’ rating from the Street. Here’s a closer look at them, to find out just why KeyBanc and the rest of the Street is bullish.

MasTec, Inc. (MTZ)

The first stock on our list is MasTec, a construction and engineering company that provides contract services in energy and infrastructure build-outs. MasTec, with its $5.67 billion market cap and 22,000 employees, has positioned itself as an indispensable provider of building, engineering, installation, and maintenance services for a client base that leans heavily toward the communications, energy, government, and utility sectors.

MasTec bills itself as an expert in a number of important specialized fields, including communications, power generation and delivery, heavy civil and industrial construction, turnkey solutions for water and sewer distribution and transmission systems, energy transition solutions, and oil and gas transmission pipelines. While this may sound like an eclectic combination, the items have several common factors: they are niche fields in construction, and many of them revolve around pipeline and pumping technologies.

For MasTec, these fields of niche expertise bring in big business. In 2022, the company handled over $6.5 billion in energy-related projects, including projects in the transition from fossil fuel to ‘green’ energy sources such as hydrogen hubs, carbon capture, and wind and solar power.

While the company is profitable, its revenues and earnings are frequently volatile – and the last reported quarter, 3Q23, was considered somewhat disappointing. Revenue came in at $3.26 billion, a company record, but also $532 million less than had been expected. MasTec’s Q3 earnings were 95 cents per diluted share; this missed the forecast by 89 cents per share. The company’s overall strength, however, could be seen on the balance sheet. While the company was carrying more than $3 billion in long-term debt at the end of the quarter, it had also managed a $213 million debt reduction and finished the quarter with liquid assets on hand of $1.16 billion.

For KeyBanc’s Sangita Jain, the earnings and revenue misses were disheartening, but not disqualifying. In her view, the stock still presents plenty of attractions for investors. As she puts it, “MTZ has become a show-me stock after the recent disappointing results, but at this juncture, we believe that expectations have been reset to achievable levels and the valuation is attractive. We may be somewhat early in our recommendation, and for the stock to ‘work,’ we need strong execution, and for management to provide consistently achievable guidance. That said, we are attracted by MTZ’s favorable positioning in growing end markets, which are looking at extended periods of investment through federal stimulus and expect the shares to regain some luster in 2024, forming the basis for our Overweight rating…”

That Overweight (Buy) rating comes along with a $92 price target that points toward a 28% increase in share price on the one-year time horizon. (To watch Jain’s track record, click here)

There are 10 recent analyst reviews on file for MasTec stock, and they break down 8 to 2 in favor of Buy over Hold to give these shares a Strong Buy consensus rating. That said, the average price target, at $70.11, implies the shares will stay rangebound for the time being. (See MasTec stock forecast)

Dycom Industries (DY)

The second KeyBanc pick we’ll look at now is an important player in the human resources field, providing the essential resource that every company needs: quality people. Dycom works as a contract workforce provider in the telecom industry. The company has more than 15,000 workers on its payrolls, available for jobs in everything from wireless construction to planning to maintenance to engineering – a series of specialized services to meet the essential needs of its telecom client companies.

Dycom was first incorporated in Florida, and today operates through a chain of several dozen subsidiaries, with over 600 locations across 49 states. Dycom has achieved this – a contract network capable of meeting client needs on any scale, nationwide – by building relationships. The company doesn’t see itself as merely a contractor for its clients, but as a partner, building relationships with the firms it serves, to mutual advantage.

The telecom sector is a particularly rich field for personnel contracting. With technology changing, visible in everything from new 5G networks to AI-powered tech, telecom firms don’t always have the immediate expertise needed for current conditions; Dycom, with its large workforce, available on demand to provide flexibility, can provide the right workers at the right time in the right place – an advantage that its enterprise clients are willing to pay for.

Dycom’s quarterly revenues and earnings show a clear seasonal pattern, rising from Q4 through Q3; In the company’s latest financial release, for fiscal 3Q24, which ended this past October, Dycom reported a top line of $1.136 billion. This figure was up 8.9% y/y, and came in $70 million better than had been expected. Dycom’s bottom line, the EPS of $2.82, was $1.06 per share over the forecast.

In her coverage for KeyBanc, analyst Jain sees an idiosyncratic opportunity taking shape for Dycom. As the Federal Government continues to appropriate and allocate funds for telecom purposes, the flood of money into the industry will create new work and new opportunities for firms like Dycom. She writes, “We believe that DY is in the early innings of benefiting from the record federal funding (>$100B) committed to building out broadband access across the U.S., especially in rural areas where DY has demonstrated capabilities. Telecom capex trends and data points can be uneven, yet DY’s deep large-telco customer relationships and the impending wireline spending cycle, combined with its discount valuation, make for an attractive entry point, in our view. This forms the basis for our Overweight rating…”

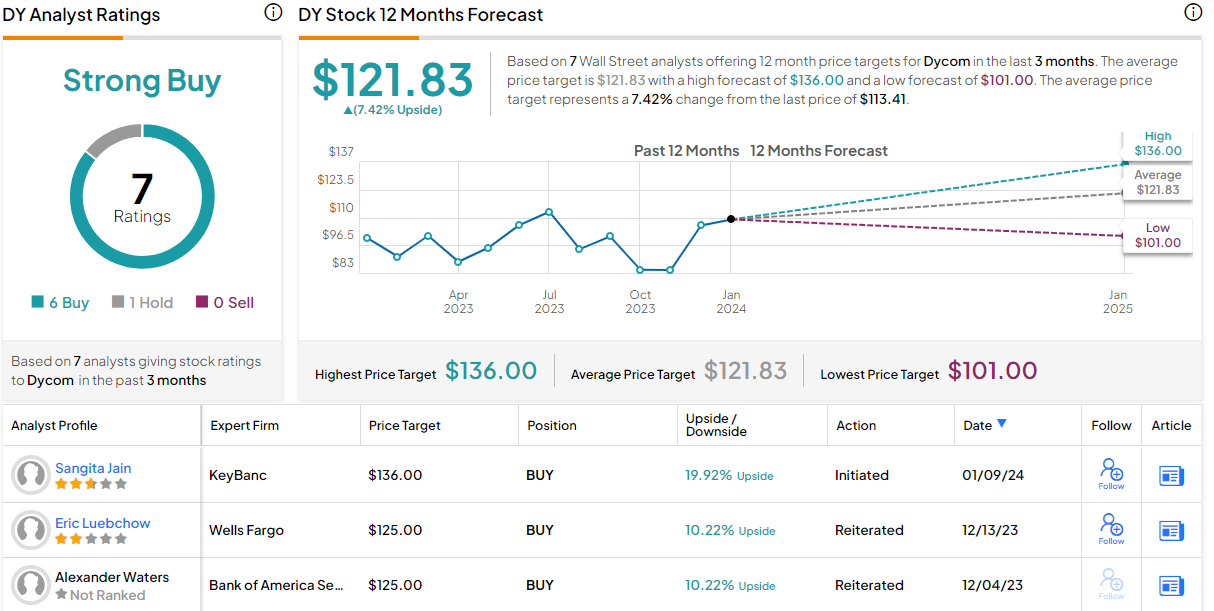

The Overweight (Buy) rating that Jain gives this stock is complemented by her $136 price target, implying a 20% upside for the next 12 months.

Dycom has picked up 7 recent analyst reviews, and they break down 6 to 1 in favor of Buying over Holding, for a Strong Buy consensus rating. The shares are trading now for $113.41 and have an average price target of $121.83; together, these numbers suggest a one-year potential upside of 7.5% for DY stock. (See Dycom stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.