We are now past the mid-point of the current earnings season. So far, the reports at the S&P 500 (SPX) have been much better than expected, with roughly 80% of the companies beating EPS estimates. Although the companies in the index are reporting a year-over-year decline in earnings, that decline is way smaller than what the analysts were talking about just a month ago. According to Factset, the blended Q1 earnings decline estimate, which combines the actual reported results with estimates for firms that are yet to report, stands at -3.7% in end-April, versus the expectations of a -6.7% crash in end-March.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

Amazon Dominates the Quarterly Results

In total, 55% of companies that have already reported show that the S&P 500 is in an earnings recession (defined as two consecutive quarters of year-on-year earnings declines). However, out of the eleven S&P 500 sectors, five are reporting earnings growth: Consumer Discretionary (leading by a wide margin), Industrials, Energy, Financials, and Real Estate. Earnings in other sectors have declined from the same quarter of 2022, with the biggest drag being the Materials sector’s financial results. But let’s leave the losers for a minute and have a closer look at the winners.

The Consumer Discretionary sector is celebrating an almost 50% increase in earnings year-on-year; an eye-popping growth even for the most buoyant economic and monetary environment. But anyone looking a bit deeper into the numbers can notice that they are immensely skewed by just one company: Amazon (AMZN).

The e-commerce and cloud-computing giant with a market cap of over $1 trillion is responsible for more than 70% of the sector’s earnings increase in Q1 2023. Moreover, Amazon has become so fundamental to the S&P 500, that it is also the largest contributor to earnings growth for the entire index; its results have taken off almost 30% of the index’s earnings decline in the quarter. The sector’s and the index’s calendar year 2023 are expected to also be influenced heavily by the behemoth’s results.

Amazon Is a League of Its Own (in its Sector)

Do these results justify a TTM P/E ratio of 146 and a Forward P/E of 62, versus the Consumer Discretionary sector’s 31 and 26, accordingly? It’s hard to say, especially since the company’s business is so versatile it could be included in at least three sectors (besides on- and off-line retail, it engages in cloud services, advertising, and subscription services; it is also entering other industries such as healthcare).

Amazon began operating as an online retailer; as the world’s largest e-commerce operator, its place on top of the Consumer Discretionary sector is secure. But although retail remains the company’s primary source of revenue, its Amazon Web Services (AWS) cloud-service business is growing at a fast pace and is currently responsible for all of its operating income. In short, Amazon’s retail business is still losing money, even after decades in business, while the cloud is the earnings driver.

The Cloud Crowd

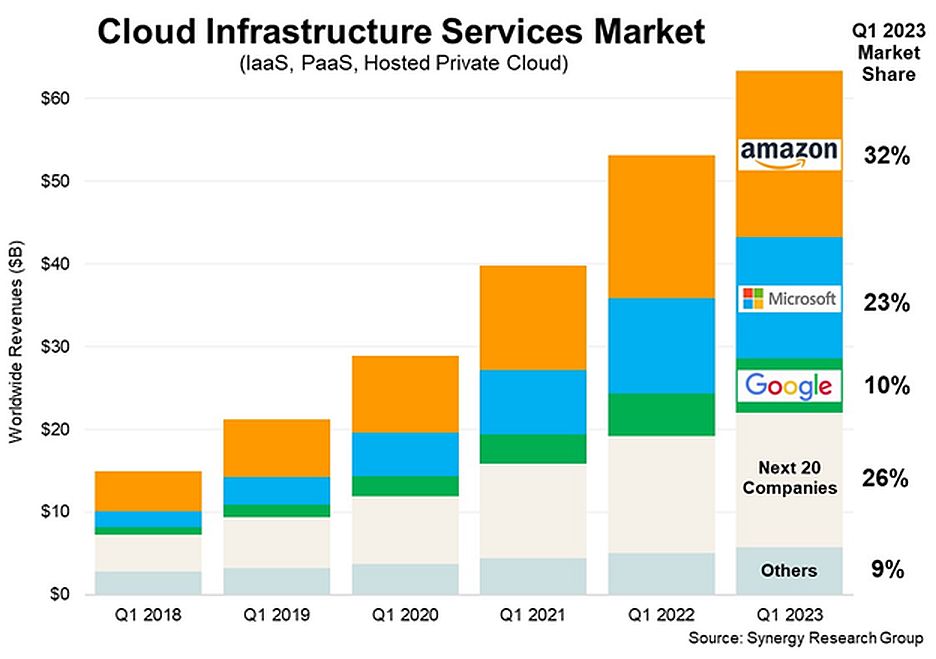

Amazon controls above a third of the global cloud market, substantially more than its next closest competitors, Microsoft (MSFT) and Alphabet (GOOGL). The two cloud leadership contenders are much larger in total market cap than Amazon; they are also much cheaper, although not cheap. MSFT now sells at a Forward P/E of 32 (vs. the IT sector’s 24), while GOOGL looks to be a bargain at a Forward P/E of just 22 (vs. the Communication Services’ 18).

It may be that Amazon should be in the IT sector, like Microsoft, or in the Communication Services, like the Google parent. In any case, judging by net income sources, Amazon is not a retail stock, but a cloud play – so it shouldn’t be compared to the likes of eBay (EBAY) or Walmart (WMT).

AI Will Boost the Cloud

In its Q1 2023 report, Amazon showed solid results, outperforming analyst expectations with regards to both topline and earnings. However, the multitasking giant revealed a slowdown in AWS segment growth and warned that growth is expected to drop further in the current quarter. Microsoft and Alphabet both saw decelerating cloud performance in the March quarter; customers are looking to decrease spending as economic uncertainty reigns.

However, looking further than the next one or two quarters, the global cloud computing market is expected to reach $1.5 to $2 trillion by 2030, versus its size of $484 billion at the end of last year. The continued strong growth is led by the functional ability of cloud computing to improve business performance, as well as by the rising need for hybrid models, omni-cloud systems, and pay-as-you-go models. Government initiatives to safeguard data security and integrity are also helping the sector to expand. Additionally, the COVID-19 pandemic has increased the use of cloud computing and hybrid work models.

The market’s growth may increase even further thanks to the Artificial Intelligence applications and uses that have swept into our lives in recent years. All the Big Three cloud providers agree that the future growth of the cloud service business will come from the growing demand for AI-based services that each of the vendors offers on their cloud platforms. This is a great opportunity and, at the same time, a huge challenge for Amazon. For now, Microsoft is far ahead in the AI race, thanks to its special position as a primary partner for OpenAI with its ChatGPT and GPT-4 technology. Alphabet has recently made a considerable advance into the AI battlefield with its various investments in the AI technology and the incorporation of the generative AI service “Bard” into its applications.

Conclusion: Is Amazon a BUY?

One conclusion that can be drawn from the results is that Amazon is valued as a high-growth company, while in fact, it is an established slow-growth, market-commanding conglomerate, whose leadership in its most profitable segment may be soon challenged by rivals. The cloud business is a gold mine, that’s for sure; but one that is mined by many players, some of which may take over the helm. When looking for a long-term cloud computing play, Microsoft’s and Alphabet’s stocks may have more room for upside than Amazon’s.

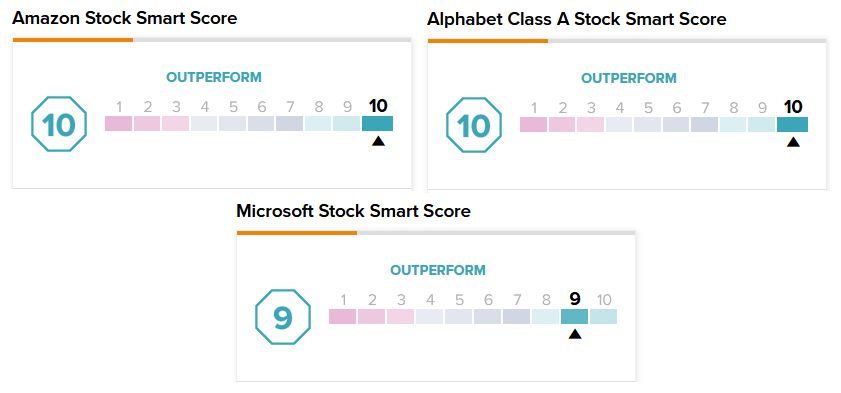

Significantly, all three companies have “Outperform” Smart Score ratings on TipRanks, with the analysts attaching “Strong Buy” recommendations to their stocks.