Utilities usually hold their ground well during uncertain times, and DTE Energy (NYSE: DTE) is no different. Over the past year, the S&P 500 (SPX) has declined by roughly 20%. In the meantime, shares of DTE Energy have only declined by about 6%. DTE Energy transformed into a pure-play regulated electric and natural gas utility following its spinoff of DT Midstream (NYSE: DTM) last year. As such, the company’s investment case comes with several attractive characteristics, including a reliable dividend. However, I wouldn’t expect much when it comes to DTE’s growth prospects, which appear limited despite the stock’s somewhat rich valuation.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Accordingly, I am neutral on the sock.

DTE’s Performance to Remain Robust Despite Ongoing Challenges

As a regulated utility, DTE’s performance is less affected by the ongoing macroeconomic and geopolitical challenges compared to the average stock out there. The company’s Electric segment keeps the lights on for 2.3 million residential, commercial, and industrial customers in Michigan, while its Gas segment distributes natural gas that powers the cooking and heating needs of 1.3 million households and businesses.

Electricity and natural gas consumption are, to a large extent, recession-proof and mostly not impacted by the underlying state of the economy. Sure, if electricity and gas rates are high, you may try to moderate consumption, but only by so much. Further, natural gas consumption could increase during inflationary environments such as the current one, as households are likely to favor cooking inside over ordering overpriced food.

Finally, regulators ensure that the company can increase its charging rates by reasonable hikes that make up for DTE’s growing operating costs and allow the company to make a fair return on its capital investments. Thus, the company is further protected from the current highly inflationary environment.

The qualities that come attached to regulated utilities are illustrated in DTE’s historical revenue generation, with the company featuring a five-year and a 10-year revenue compound annual growth rate (CAGR) of 7.1% and 5.4%, respectively. Its growth has been slow but gradual and consistent. The company’s performance so far this year has also demonstrated the resilience of DTE’s business model.

Year-to-date, the company has posted operating revenues and net income of $14.75 billion and $818 million, up from $10.32 billion and $598 million during the first nine months of 2021, respectively. That’s quite reassuring, considering that households have been impacted by a tough economic environment during this period.

Consequently, I am confident DTE’s performance will most likely remain resilient as we advance.

Trust the Dividend, but Expect Minor Hikes Ahead

With DTE’s revenues and net income steadily growing over the years, the company has been delivering on its strategy of providing an attractive and growing dividend. In fact, DTE has never cut its dividend as far as its public data goes – all the way back to 1962. Isn’t that impressive? Since 1962, multiple recessions and periods of highly challenging economic environments have occurred. Yet, DTE’s shareholders and the company’s commitment to the dividend were honored.

After paying a constant quarterly dividend per share of $0.438 from 1993 to 2006 and then a constant one of $0.451 from then until 2010, dividends have grown annually since. Could dividend growth be paused again at some point? Sure. However, I would definitely not expect a cut. Based on the company’s year-to-date earnings and ongoing developments, I expect DTE to post earnings per share close to $6.00 this year, which implies a comfortable payout ratio of around 60%. That should keep investors reassured regarding dividend coverage.

Simultaneously, though, I wouldn’t expect rapid dividend growth either, which is likely to remain in the low-single-digits in the coming years as DTE pursues its electric capital investments over the 2022-2026 period, which are estimated to amount close to $15 billion.

Note that it may seem like DTE cut its dividend last year. However, this is not true. The reduction only reflects the aforementioned spin-off. The combined dividend actually increased.

What is the Price Target for DTE Stock?

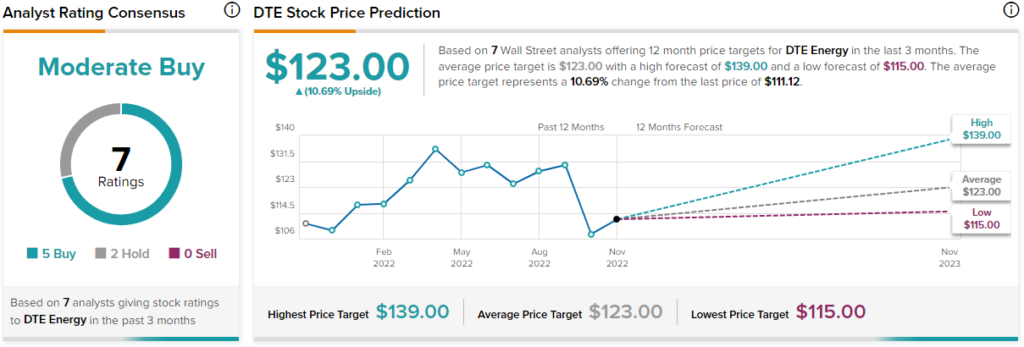

Turning to Wall Street, DTE Energy has a Moderate Buy consensus rating based on five Buys and two Holds assigned in the past three months. At $123.00, the average DTE Energy stock forecast implies 10.69% upside potential.

Takeaway: A Utility Stock for Conservative Dividend Investors

DTE is not going to make you rich overnight. However, it can most certainly provide you with reliable income that should continue growing slowly but gradually over the years. As proven through DTE’s decades-long track record of robust earnings generation and dividend payouts, the stock should keep performing well when most stocks won’t. That said, remember to keep your expectations low, as regulated utilities lack any extraordinary growth catalysts.

Additionally, note that investors are currently paying around 18.5x DTE’s expected net income for 2022. This is a steep multiple for a company with relatively uninspiring growth prospects.

It may be justified, as investors are willing to pay a premium for a company they can trust during the ongoing macroeconomic unrest, but it still means future returns could be limited for investors buying the stock at its current levels. Thus, the stock will likely be appreciated mostly by conservative, dividend-growth investors.