Online betting is increasingly being legalized in the United States after the U.S. Supreme Court struck down the Professional and Amateur Sports Protection Act 2 (PASPA) three years back. This year, according to a FinancialBuzz report, 19 U.S. states are expected to decide on the legalization of sports betting which could significantly benefit online sports betting companies.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

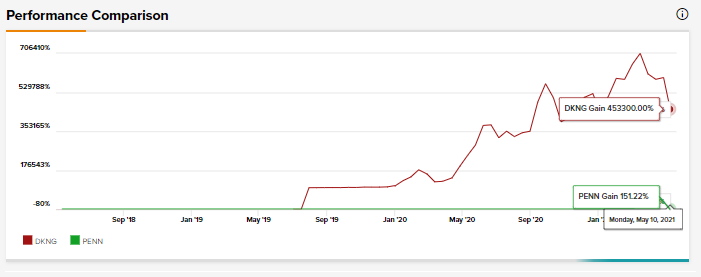

Using the TipRanks Stock Comparison tool, we will compare two online betting companies, DraftKings and Penn National Gaming, and see how Wall Street analysts feel about these stocks.

DraftKings (DKNG)

DraftKings is an online sports gaming and entertainment company that provides its users with a sports betting Sportsbook, daily fantasy sports, and online casino gaming opportunities.

Last week, DKNG reported first-quarter revenues of $312 million, a jump of 253% year-on-year. Revenue was up 175% year-on-year after giving pro-forma effect to the company’s acquisition of Diamond Eagle Acquisition Corp and SBTech Global Ltd that was completed on April 23 last year.

However, the company’s losses widened to $346.3 million in Q1 versus a loss of $68.7 million in the same quarter last year.

DraftKings’ Chief Financial Officer, Jason Park said, “Our $312 million in first quarter revenue, 114% increase in MUPs [monthly unique payers] and 48% growth in ARPMUP [Average Revenue per MUP] reflect solid customer acquisition and retention as well as successful launches of mobile sports betting and iGaming in new states. We are raising our revenue outlook for 2021 due to the outperformance of our core business in the first quarter and our expectation for continued healthy growth.”

The company has raised its financial outlook for FY21 and expects revenues to land between $1.05 billion and $1.15 billion versus earlier forecasts of between $900 million and $1 billion. This indicates year-on-year growth of between 63% and 79%.

The upgraded guidance is a result of DKNG’s strong activation of its user base due to effective marketing, the launch of mobile sports betting in Michigan and Virginia, and iGaming in Michigan. The fiscal outlook also assumes that all professional and college sports events take place as scheduled, and DKNG continues to operate in the U.S. states in which online sports betting is currently live.

DraftKings’ online sports betting is live in 12 U.S. states at present. That represent 25% of the U.S. population. The company’s Co-Founder, CEO, and Chairman, Jason Robins said on the earnings call, “We believe the outlook for further legalization is very promising. In 2021, more than 20 state legislatures have introduced legislation to legalize online sports betting.”

The company anticipates both its monthly unique payers (MUP) and average revenue per MUPs (ARPMUP) to increase in FY21 with MUPs growing at a higher rate than ARPMUP.

DKNG also gave a quarterly revenue breakup for FY21 and expects Q1 revenue to represent 28% of FY21 total revenue while second-quarter revenue is forecast to account for slightly higher than 20%. Q3 revenue is expected to represent slightly less than 20% of the full-year revenue, with fourth quarter revenue likely to account for 30%.

The company anticipates higher sales and marketing spend in FY21 than FY20 as it has become the official sports betting partner of the National Football League (NFL).

DraftKings also gave some color regarding its adjusted loss before interest, taxes, depreciation, and amortization for FY21 and expects it to be the deepest in Q3 due to higher sales and marketing spend as the NFL season kicks-off with “three states in their first full NFL season”. (See DraftKings stock analysis on TipRanks)

Yesterday, Northland Securities analyst Greg Gibas reiterated a Buy and a price target of $70 on the stock. Gibas commented on DKNG’s Q1 results, “DKNG reported strong Q1 results featuring revenue growth that was well ahead of consensus, accompanied by solid 2021 guidance upside. Top-line growth was driven by better than expected user activation (MUPs) following the well-executed launches in Michigan and Virginia, as well as overall strong unique payer retention and acquisition across DFS [daily fantasy sports platform], SB [sportsbook], & iG [iGaming] offerings.”

Shares of DKNG have plunged 23.5% in the past month.

Overall, consensus among analysts is a Moderate Buy based on 17 Buys and 6 Holds. The average analyst price target of $70.86 indicates upside potential of around 59.2% from current levels.

Penn National Gaming (PENN)

Penn National Gaming has ownership interests in or owns and operates 41 racing and gaming properties across 19 states in the United States. The company offers online sports betting in Mississippi, Pennsylvania, Colorado, Illinois, Indiana, Iowa, Michigan, and West Virginia.

Last year, PENN acquired a 36% stake in Barstool Sports, a digital media company for $163 million. Since then, the company has launched its Barstool Sportsbook app and products in the states of Illinois, Michigan, and Pennsylvania.

PENN also operates online sports betting in the states of West Virginia, Iowa, Indiana, and Pennsylvania through strategic partnerships and has an interactive gaming division through its subsidiary, Penn Interactive Ventures, that has launched iCasino in Pennsylvania and Michigan.

Last week, the company reported its first-quarter results with revenues of $1,274.9 million, down 6% compared to pro-forma results from the first quarter of 2019, while adjusted EBITDAR was up 7% to $447 million.

Jay Snowden, President, and Chief Executive Officer stated, “We remain focused on garnering top-three gaming revenue market share for the Barstool Sportsbook and driving best in class profitability. Since launching our product just over seven months ago, we have registered more than 400,000 customers and generated over $660 million and $61 million in handle and gaming revenue, respectively. We plan for the online Barstool Sportsbook to be live in eight states by football season and in at least 10 states before the end of the year.”

PENN intends to open or rebrand six more retail sportsbooks by the end of this year. The company is also looking at increasing cross-selling opportunities through its mychoice mobile app that was launched last quarter.

According to the company, the app has been downloaded 333,000 times with monthly active users of approximately 115,000. The company stated that the app allows for more meaningful user engagement, provides for targeted marketing, and is a key driver of growth in revenues. (See Penn National Gaming stock analysis on TipRanks)

Following the Q1 earnings on May 6, Deutsche Bank analyst Carlo Santarelli reiterated a Sell with a price target of $31 on the stock. Santarelli said in a research note to investors, “PENN’s 1Q21 net revenue was $55 mm ahead of our forecast, though adjusted EBITDAR was relatively in line, coming in 1% ahead of our estimate ($447 mm versus our $442 mm estimate), as margins fell 120 bps shy of our forecast. The South and Midwest regions drove upside to our estimate, though this was largely offset by higher other segment (corporate/interactive/OSB) losses.”

“Given peer reports, we don’t find the upside to Consensus to be overly surprising to many, and as such, we think the stock reaction will likely be more tied to the equity market direction…Management noted that spend per visit remains considerably higher than preCOVID levels, while visitation has returned to near pre-COVID levels as the 55+ customer has been returning,” Santarelli added.

Shares of PENN have plunged by almost 21% in the past month.

Overall, consensus among analysts is a Moderate Buy based on 6 Buys, 1 Hold, and 1 Sell. The average analyst price target of $116.57 indicates upside potential of around 45.4% from current levels.

Bottom Line

The rising legalization of online sports betting in the United States could benefit both DKNG and PENN as it could offer significant revenue-generating opportunities for the companies. While currently, both stocks appear to indicate significant upside potential over the next 12 months, analysts seem to be more bullish on DKNG’s long-term growth prospects.