After the annus horribilis of 2022, with the final quarter now in play, investors will be hoping a late-year rally will materialize. According to Carson Group’s chief market strategist Ryan Detrick, that’s not such a far-fetched idea.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

“While October has a reputation for crashes, it is really a bear market killer,” Detrick recently wrote. “Of the past 17 bear (or near bear markets), stocks bottomed in October six times. Could it happen again? With sentiment this pessimistic and extremely positive seasonals right around the corner, we’d be open to it.”

Sentiment is indeed low. Bearish sentiment – according to the end of September’s American Association of Individual Investors Sentiment Survey – is at 60.8%, near record high levels. This is a bit of a contrarian indicator; historically, when sentiment has been at its lowest, it often suggests the bottom is in sight.

So, with a rebound potentially in the cards, let’s take a look at three names which could be in line for a well-deserved bounce, at least according to some Street analysts. These are stocks which have retreated significantly this year, with all down by 60% or more. Yet, according to TipRanks’ database, each also features a Strong Buy analyst consensus rating and a powerful upside potential.

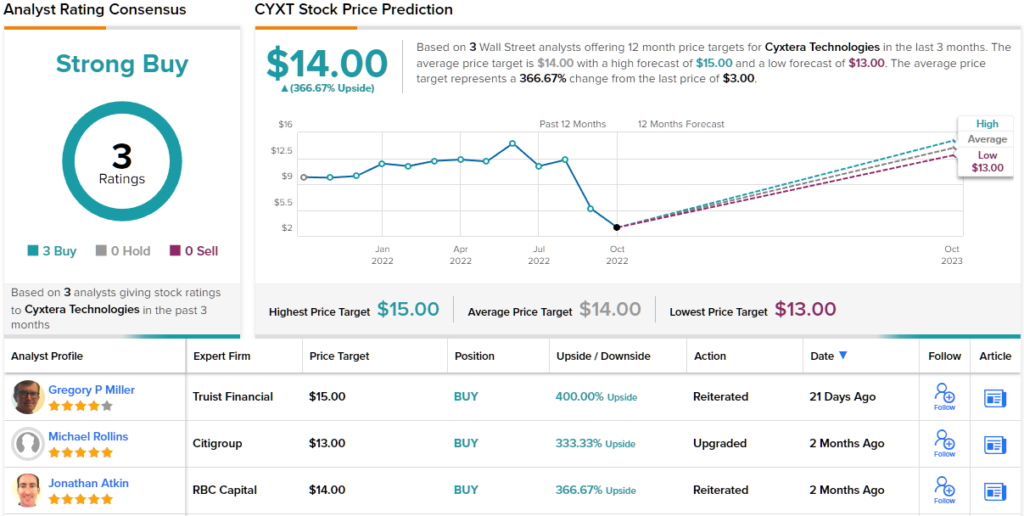

Cyxtera Technologies (CYXT)

The digital era has brought with it huge amounts of data which must be stored somewhere, and this in turn has led to a surge in global demand for data centers. This is where Cyxtera Technologies enters the frame. The company is a big player in data center colocation and interconnection services; Cyxtera boasts 60 data centers which are spread across 30 markets, with over 2,300 private enterprise and public sector customers making use of its services.

Cyxtera is relatively new to the stock market, having gone public via the SPAC route in July 2021. That’s an unfortunate bit of timing as anyone who has been following the fate of SPACs over the last year and a half or so will know. SPACs have had a miserable time and so have CYXT shares; they are down 76% on a year-to-date basis, a performance not helped by several factors.

In the latest set of quarterly results – for 2Q22 – revenue increased by 5.3% year-over-year to $184.7 million, just missing Street expectations by $0.3 million. There was a more conclusive miss on the bottom-line, with EPS of -$0.27 falling 6 cents short of the -$0.21 consensus estimate.

However, assessing the company’s prospects, Truist analyst Gregory P. Miller thinks it is a good time to be loading up.

“Despite current macroeconomic headwinds and the stock’s underperformance YTD, we believe fundamentals largely remain the same and increasingly believe in the Cyxtera management team’s ability to take advantage of industry tailwinds (i.e., expanding data usage, the digitalization of the economy). We continue to believe Cyxtera is well-positioned over the long-term with increasing utilization in key markets and expansion in resource-constrained regions as well as improving MRR/c pricing,” Miller opined.

Miller is certainly bullish; along with a Buy rating, the analyst’s $15 price target makes room for 12-month returns of a huge 400%. (To watch Miller’s track record, click here)

Other analysts’ expectations are hardly less upbeat; both other recent reviews are positive, making the consensus view here a Strong Buy. Moreover, the $14 average target suggests shares will be changing hands for a 367% premium a year from now. (See Cyxtera stock forecast on TipRanks)

Whole Earth Brands (FREE)

Let’s now pivot to a company also dealing with modern concerns but ones of an entirely different hue – that of the earthy kind. As its name suggests, Whole Earth Brands is focused on wellness, a lifestyle choice increasingly important to large parts of the population. Many consumers are now on the lookout for natural, plant-based, healthy products, and Whole Earth Brands caters to this consumer base with a selection of brands. On the CPG side, these include Whole Earth, Pure Via, Wholesome, Swerve, Canderel, and Equal, while its Flavors & Ingredients segment boasts Mafco, a leading manufacturer of natural plant-based licorice products.

In its most recent quarterly statement, for 2Q22, revenue reached $133.5 million, representing a 5.5% year-over-year growth, while beating the Street’s call by $2.85 million. However, the company missed expectations on the bottom-line, with EPS of $0.03 falling short of the analysts’ prediction for $0.10. Management reaffirmed its full-year guidance, however, with revenues expected in the $530 million to $545 million range – at the mid-point above consensus at $535.24 million.

The stock, like so many others, has taken a sound beating this year, and shares now trade at a 68% discount to the price at the beginning of 2022.

That could be an opportunity, according to the thesis laid out by 5-star analyst Mark Smith of Lake Street.

“We think the company continues to execute and run the business successfully despite a tough operating environment. We think current headwinds are temporary and the share gains and operational improvements being made will set it up to be a stronger company once the market improves. We believe the company is on the right track to becoming a +$1B revenue Branded CPG business,” Smith opined.

“We think the current valuation is attractive and that Whole Earth provides investors with an opportunity to buy a branded CPG company with a long runway of growth that is supported by secular tailwinds,” the analyst summed up.

Smith thinks the stock has some way to go, and by some way, we mean 303% of upside. Those are the returns investors are looking at, should the stock make it all the way to Smith’s $14 price target. No need to add, the analyst’s rating is a Buy. (To watch Smith’s track record, click here)

Turning now to the rest of the Street, other analysts also like what they’re seeing. 4 Buys and no Holds or Sells add up to a Strong Buy consensus rating. Not to mention the $12 average price target implies ~246% upside potential. (See FREE stock forecast on TipRanks)

KalVista Pharmaceuticals (KALV)

And now let’s switch gears once more and take a look at a biotech. KalVista Pharmaceuticals focused on discovering, developing and bringing to market small molecule protease inhibitors which are indicated to treat diseases with significant unmet needs. More specifically, the drug candidates are intended as best-in-class treatments for hereditary angioedema (HAE) and diabetic macular edema (DME).

A biotech stock’s fortunes are very dependent on the success or failure of its pipeline, and here KalVista recently announced a negative development which sent shares into meltdown mode; last week, the company said it is terminating its KVD824 program for the treatment for hereditary angioedema after numerous patients displayed liver enzyme elevations in a mid-stage trial.

While that is unfortunate, the lack of success does not necessarily extend to other programs. Of note here is KVD900 (sebetralstat) which is a different compound indicated to treat hereditary angioedema. The drug has successfully completed a phase 2 study and the company will now focus on the completion of the ongoing phase 3 KONFIDENT trial; results are expected to be announced in 2H23 and should support an NDA filing the following year.

To this end, Needham analyst Serge Belanger remains in the bull-camp and sees no reason to change tack.

“The decision to terminate KVD824 is not expected to have any read-thrus to the KVD900 program given that they are different compounds,” the analyst explained. “We note that KVD900 previously completed a PoC phase 2 trial as an acute HAE treatment in 68 patients without observations of liver enzyme elevations.”

“KALV remains well-funded with cash of ~$142MM (as of 7/31/22) that provides runway well into 2024,” Belanger went on to add, before concluding, “We view any downside move in KALV shares beyond 30-35% as an over-correction given that the main value-driving asset KVD900 is unaffected.”

That scenario has played out and some. Over the past week, the shares have waved goodbye to 67% of the previous valuation. And while Belanger’s price target is lowered from $38 to $24 to “reflect termination” of the KVD824 program, investors should not get too despondent; the new figure still makes room for ~412% gains over the one-year timeframe. Belanger’s rating stays a Buy. (To watch Belanger’s track record, click here)

Judging by the consensus breakdown, opinions are anything but mixed. With 5 Buys and no Holds or Sells assigned in the last three months, the word on the Street is that KALV is a Strong Buy. At $26.80, the average price target implies ~471% upside potential. (See KALV stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.