With the Federal Reserve holding its November FOMC meeting now, there’s plenty of speculation on the central bank’s next move. The conventional wisdom says the Fed will hike rates again, by another 75 basis points – the fourth such hike in a row this year. But after that, no one knows.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Inflation remains above 8%, so the Fed’s tighter monetary policies have clearly not reined in high prices – yet. According to Fundstrat, however, the Fed has moved far enough in that direction, and we’ll start to see the results as early as the first half of next year. The firm’s head of research, Tom Lee, notes that with a probably Republican midterm victory likely to lead to pullbacks in Federal spending, the Fed may soon be perceived as winning against inflation.

Lee sees the current status as “a dramatic wealth effect loss and tightening of financial conditions,” and looking forward, he believes 1H23 will likely see a substantial market rally, perhaps pushing the S&P as high as 4,600, or a 19% gain from current levels.

If Lee is right, then now is likely a propitious time for investors to buy in, especially into stocks with depressed share prices. We’ve opened up the TipRanks database to look at three stocks that are simply too cheap to ignore right now – especially given their Strong Buy consensus ratings and hefty upside potentials for the coming year. Let’s take a closer look.

WeWork (WE)

We’ll start in the co-working space, with WeWork, the leader in the coworking space niche. WeWork’s model is well known – allow freelancers and the self-employed access to high-end office space, available according to their needs. Customers can rent space for a few hours, or a few weeks or months, or even a couple of years; the advantage is not having to put up the overhead for an office facility. WeWork’s model quickly proved popular, and the company now owns over 44 million square feet of work space in more than 700 locations in 150 cities in 38 countries. Almost half of the total is in the US and Canada, and the company boasts 658,000 physical memberships.

WeWork has been seeing rising revenues in recent quarters; in August, the company reported Q2 numbers showing a top line of $815 million. This was up 7% from Q1, and an impressive 37% year-over-year. WeWork typically runs a net loss each quarter, but that net loss moderated by 31% y/y for Q2, to $635 million. During the quarter, the company reported 72% consolidated physical occupancy rate. The company has deep pockets, despite the steep quarterly losses, and reported having $1.7 billion cash assets and other liquidity as of the end of Q2. Looking forward, WeWork expects to bring in $3.4 billion to $3.5 billion in total revenue for 2022. By comparison, the company saw $2.6 billion in revenues for 2021. The company will report its Q3 results on this coming November 10.

So, overall, WeWork is looking at increasing revenues and solid customer sign-ups. Its ‘Space-as-a-Service’ model has proven popular – and has spawned numerous copycat competitors. This is the background to WeWork’s current share price, which is down 69% year-to-date.

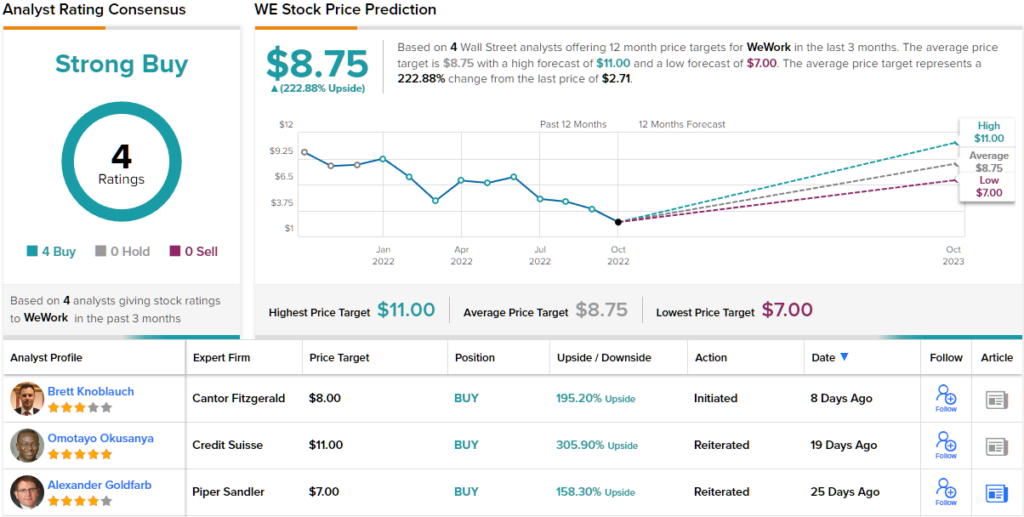

This interesting company has caught the attention of Canter analyst Brett Knoblauch, who initiated coverage of the stock with a bullish case.

“Demand for flexible workspace has remained robust post-pandemic, and we believe the shift away from traditional office lease strategies by enterprises will act as a decade-long tailwind. Further cost cuts combined with revenue growth result in our view that WeWork could generate $1.19/share in FCF in 2027E… The biggest near-term catalyst for shares, in our view, is an announcement pertaining to extending maturities of its debt. Ultimately, we believe investors have ignored WeWork due to its much scrutinized history, which creates an asymmetric risk/reward opportunity at current levels,” Knoblauch opined.

Knoblauch starts off his coverage with an Overweight (i.e. Buy) rating on WE, and a price target of $8 that suggests a robust one-year upside potential of 196%. (To watch Knoblauch’s track record, click here)

Looking at the consensus breakdown, other analysts are on the same page. With 4 Buys and no Holds or Sells, the word on the Street is that WE is a Strong Buy. WE shares are priced at $2.71 and their $8.75 average target implies ~223% gain in the next 12 months. (See WeWork stock analysis on TipRanks)

Guardant Health (GH)

We’ll now switch over to the biotech sector where Guardant Health has taken an interesting approach. The company is developing new lab methodologies and blood tests to improve the pathology and diagnostics that are so important in precision oncology research. Basically, the pharmaceutical researchers need accurate testing – and Guardant aims to give that to them.

Guardant offers the first complete genomic blood test approved by the FDA, the Guardant360 CDx, which can give genomic results in just 7 days, based on a simple blood draw. In addition, the company’s Guardant360 TissueNext can provide tissue biopsy results – and a genomic readout – based on the same technology. Guardant boasts that its testing is widely covered by Medicare and private payers which among them cover over 200 million patients.

Since introducing its tests, Guardant has seen wide acceptance. Over 300,000 tests have been performed, ordered by more than 12,000 oncologists, and over 300 peer-reviewed publications have printed articles on them.

Wide acceptance and proven results have helped Guardant at the top line; the company has posted 7 sequential revenue gains in the past two years. The last quarter reported, 2Q22, showed $109.1 million in revenues, up 19% year-over-year. Those revenues were supported by 29,300 tests reported to clinical customers, and another 6,000 reported to biopharma customers, in the quarter, for y/y gains of 40% and 65% respectively.

The company continues to work at expanding its test offerings, and has several trials ongoing to evaluate new tests. The most prominent of these is the ECLIPSE trial, which is evaluating the Shield blood screening test for colorectal cancer. The study has reached its target enrollment of 12,750 patients between ages 45 and 84, across the US.

At the same time that the company is seeing sales growth, it is also seeing deepening losses. The Q2 net loss of $229.4 million, or $2.25 per share, was more than double the net loss in 2Q21. On the trading side, Guardant shares are down 51% so far this year.

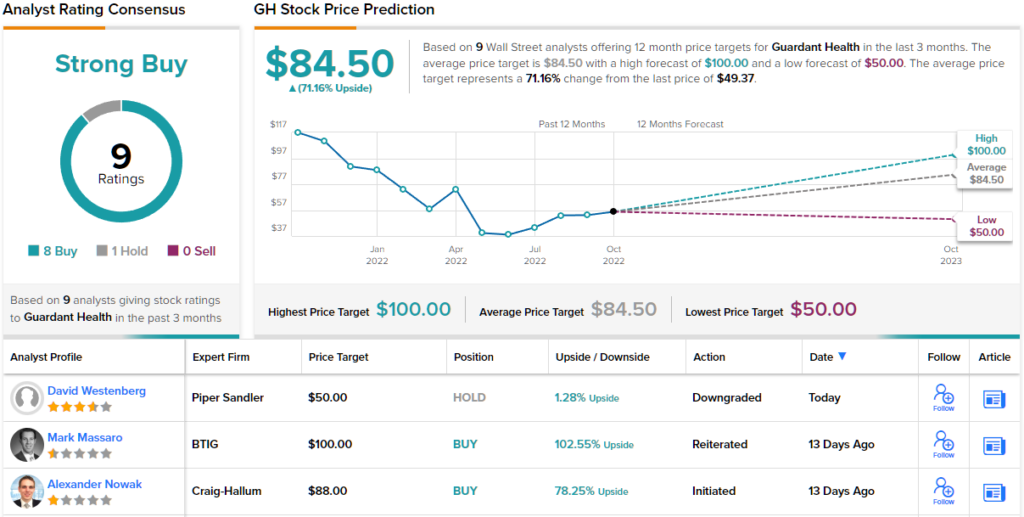

These losses haven’t stopped analyst Alexander Nowak, of Craig-Hallum, from taking a bullish stand on GH, based on the company’s prospects.

“The company will dramatically change cancer care in the next five years using liquid biopsies. A key factor is ECLIPSE, a pivotal study to demonstrate GH’s Shield test can screen for colorectal cancer (CRC) using blood, potentially replacing a colonoscopy and/or providing an easier option to the ~40% of people not screened today. Our work indicates the study will be successful, change how CRC is screened forever and open the door to multi-cancer screening via a blood test,” Nowak opined.

“This is not a risk-less trade – ECLIPSE failure is plausible (our opinion unlikely) – but if successful it puts GH on a path to $1.5B sales in five years and a multiple of that in ten,” the analyst summed up.

In Nowak’s view, GH stock deserves a Buy rating, and his $88 price target predicts a 79% upside in the coming year. (To watch Nowak’s track record, click here)

Cutting-edge biotech generally picks up plenty of Wall Street attention, and Guardant has 9 recent analyst reviews on file, including 8 Buys and 1 Hold, for a Strong Buy consensus rating. The stock’s average price target of $84.50 implies a 71% gain from the current trading price of $49. (See GH stock analysis on TipRanks)

Akili, Inc. (AKLI)

And now for something completely different. Akili has developed a digital medicine for the treatment of cognitive issues, particularly attention deficit, in kids. The digital platform is designed to target neural systems in the brain that are connected to attentional control, using specific sensory stimuli and motor challenges – delivered through a video game.

In 7 years of research before releasing the EndeavorRx, Akili conducted 5 clinical trials with more than 600 patients in 15 states. The digital medicine game is not designed as a stand-alone therapy, and is intended to be used, by prescription only, in conjunction with tradition medications.

This company is new to the public markets, having gone public on NASDAQ index just this past August. Akili entered the public market through a business combination with Social Capital Suvretta Holdings Corp. I (SCS). The combo, which was completed on August 19, saw Akili gain $163 million in gross proceeds, and the company started trading under the AKLI ticker on August 22. Since entering the public market, however, Akili has seen its stock tumbling 78%.

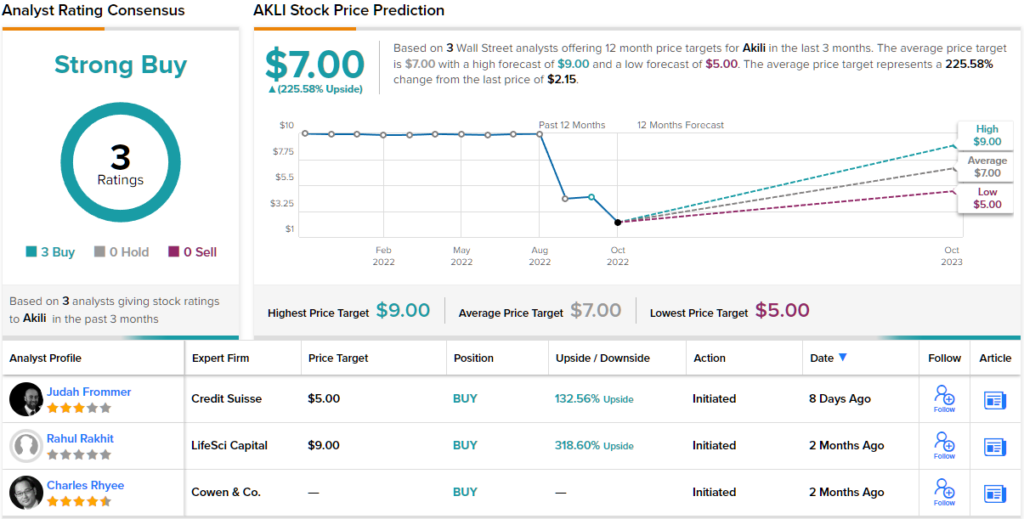

Analyst Judah Frommer, of Credit Suisse, sees an interesting path forward for Akili. Looking toward the next year or so, Frommer rates the shares an Outperform (i.e. Buy), and his $5 price target implies a gain of ~133%. (To watch Frommer’s track record, click here)

Baking his bullish stance, Frommer writes: “Our rating takes into account the risk/reward skewing to the upside following the stock’s sell-off after the de-SPAC and accounts for the evolving payor/provider landscape for prescription digital therapeutics (PDTs), the general unmet need within attention deficit/hyperactivity disorder (ADHD) care/therapy, and the mixed nature of data generated for Akili’s lead product, EndeavorRx, that likely necessitates additional real-world evidence.”

Overall, this new stock has a unanimous Strong Buy consensus rating on the Street, based on 3 recent positive analyst reviews. The shares are trading for $2.15 and their $7 average price target is highly bullish, suggesting a ~226% one-year upside potential. (See AKLI stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.