Investing is often a game in reverse psychology. There’s a natural tendency to chase stocks that are outperforming the market, but the savvy investor will know that finding the ones languishing in the doldrums could potentially generate the best returns. The key of course is to sort the wheat from the chaff and find the beaten-down names that for one reason or another are severely undervalued.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

This is where Wall Street’s stock pros come in handy. They can point investors toward such temporarily defeated yet promising equities that are ready to bounce back.

With this in mind, we delved into the TipRanks database and got the lowdown on 3 stocks that fit a certain profile; all have shed a huge amount of value over the past year, but the analysts believe they are primed for resurrection – they envisage these names rising up by a good deal over the coming months. What’s more, all three are rated as Strong Buys by the analyst consensus. Let’s see what makes them ripe for the picking right now.

Aspen Aerogels (ASPN)

First up, we have Aspen Aerogels, a company that aims to contribute to building a more sustainable world. It achieves this by developing and selling high-performance aerogel insulation products. These mostly target the energy infrastructure and building materials markets. Aspen touts an installed base of more than $1 billion of aerogel materials and a broad global IP portfolio as proof its technology is sound and protected.

The company has been showing consistent year-over-year top-line growth, and that was the case again in the most recently reported quarter, for 4Q22. Revenue climbed by 89.2% year-over-year to $59.6 million whilst beating the consensus estimate by $2.69 million. EPS of -$0.20 also came in some distance above the -$0.30 forecast.

The market reacted positively to the report but the general trend over the past year has been negative. In general, unprofitable names have been out of favor. The company has also been spending heavily, while investors have feared the impact of inflation and high interest rates.

The result has been a stock that has shed 76% of its value over the past 12 months. However, Craig Hallum analyst Eric Stine believes there’s a big opportunity at play and he thinks taking the long-term view is appropriate here.

“Aspen Aerogels should see meaningful multi-year growth given a disruptive product offering with a compelling value proposition, blue-chip customer list, low penetration (~4%) of the massive $3B+ energy insulation market opportunity and working towards an overall serviceable market opportunity of $5B+, plus the emerging $65B+ EV thermal barrier & EV battery materials opportunities, along with secular energy & energy efficiency tailwinds,” Stine opined.

“In the near-term,” the 5-star analyst went on to add, “we think investors will have to deal with volatility and a level of uncertainty as to ramp timing, and heavy spending to fully capture the EV opportunity with a substantial multi-year growth outlook. In our view, it is not about 2023 or even 2024 for ASPN, but rather how it is positioned for 2025/2026/2027 and beyond. In short, we see ASPN as ideally positioned, view it as our top name…”

A big opportunity, indeed. Along with a Buy rating, Stine’s $32 price target makes room for 12-month returns of a huge 420%. (To watch Stine’s track record, click here)

Stine’s take is no anomaly on Wall Street. ASPN’s Strong Buy consensus rating is based on a unanimous 6 Buys. Additionally, at $25.25, the average target represents potential one-year gains of ~310%. (See ASPN stock forecast)

Lsb Industries (LXU)

Next on our tour of beaten-down stocks is Lsb Industries, a North American producer of industrial and agricultural chemicals. The Oklahoma City-based company’s products range from nitrogen-based fertilizers (such as ammonia), high purity ammonium nitrate and urea ammonia nitrate fertilizer for corn and other crops to sulfuric acids and carbon dioxide, amongst plenty of other offerings. All are sold in the the United States, Canada, and Mexico.

The company’s most recent quarterly report was something of a mixed bag. While revenue rose by 23.2% year-over-year to $234 million, the figure fell short of consensus expectations by $8.31 million. That said, Lsb posted a beat on the bottom-line as adj. EPS of $0.90 beat the $0.71 forecast. The company also executed a buyback of approximately 5.6 million shares during the fourth quarter.

The market liked these results, but in general, over the past 12 months, the shares have been on a downward ride, tumbling 64%.

Surveying this performance, Deutsche Bank analyst David Begleiter notes the shares’ fortunes have “round-tripped” alongside the rise and fall of European natural gas prices. But now he thinks investors should take advantage of the low share price.

“We believe the decline in LSB shares is an opportunity for investors, as i) strong Ag fundamentals are expected to persist for at least 2-3 more years highlighted by low stocks-to-use ratios and high commodity prices and ii) US nitrogen producers continue to enjoy a significant cost advantage versus European producers as European gas prices are still 7x those of US gas prices. As such, 20-30% of European nitrogen production remains offline in ’23. Together, these drivers support LSB’s projected mid-cycle earnings power of $250-$300MM (EBITDA), or 4x its earnings in ’18-’20,” the 5-star analyst explained.

These comments underpin Begleiter’s Buy rating on LXU, while his $16 price target suggests the stock will surge 69% over the one-year timeframe. (To watch Begleiter’s track record, click here)

And what about the rest of the Street? Most are on board. The stock garners a Strong Buy consensus rating, based on 6 Buys vs. 2 Holds. At $16.13, the average target is almost the same as Begleiter’s objective. (See LXU stock forecast)

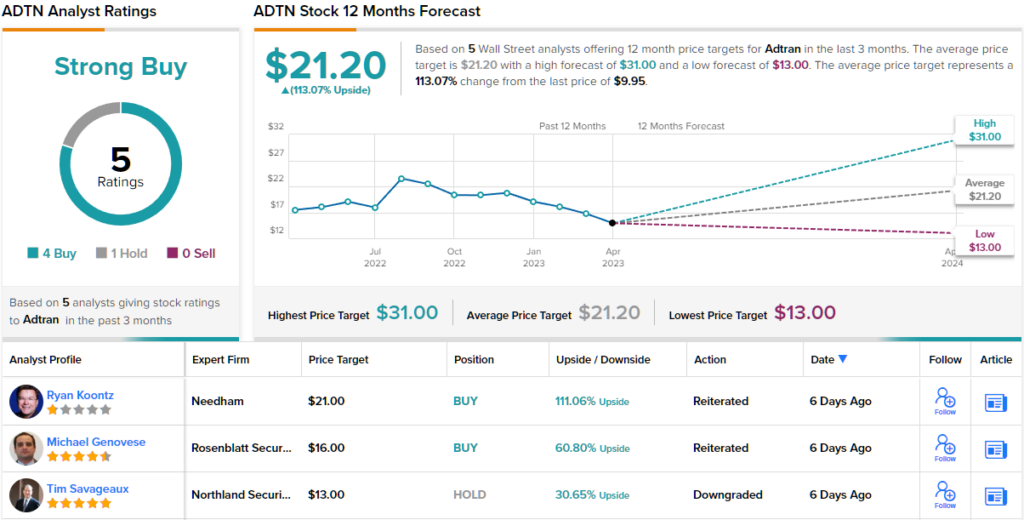

Adtran Holdings (ADTN)

For our last bargain stock, we’ll pivot to the communications infrastructure sector. Adtran is a supplier of networking and communications equipment and serves both customers domestically and internationally across 68 countries. The Huntsville, Alabama-based firm provides a wide range of management and orchestration solutions, customer premises equipment software and network infrastructure solutions.

Whereas once the company’s Broadband Access business leaned toward fiber-to-the-curb (FTTC) plus xDSL hybrid Copper/Fiber systems, it has evolved to mainly concentrate on Gigabit and 10 Gigabit PON (passive optical networking) fiber-to-the premises (FTTP) solutions.

Despite notching some impressive growth in its most recent quarterly report, for 4Q22, the company missed Street expectations. While revenue saw a 132.4% year-over-year jump to $358.27 million, the figure fell shy of consensus by $8.42 million. Likewise, EPS of $0.12 missed the $0.15 forecast.

More recently, the company had other disappointing news. Adtran released preliminary Q1 numbers which were lower than the previous guide. The company now sees Q1 revenue hitting the range between $322-$326 million, below the prior $355-$375 million. Consensus had $364.11 million in mind. The company cited customer inventory corrections that affected the subscriber solutions product line and supply snags as the reasons behind the softness.

The cumulative effect of underwhelming results is a stock that has dropped by 59% from the peak it reached last August.

Nevertheless, despite the reduced outlook, Rosenblatt analyst Mike Genovese believes there are better days ahead for Adtran.

“We are disappointed in the 1H23 miss, but we still find ADTN to be a compelling stock,” the analyst said. “We think the CPE inventory correction will be temporary, and the multi-year Fiber cycle is on track. Stimulus through the BEAD program should be a major driver starting in 2024. ADTN is trading at 9x our 2024 EPS forecast and 0.5x EV-to-2024 sales. We think this valuation is too low for a company with a solid balance sheet and long-term demand drivers, as well as Opex synergies from the ADVA deal (the companies merged last July) still ahead.”

Accordingly, Genovese has a Buy rating for ADTN shares and backs it up with a $16 price target. The implication for investors? Upside of 61% from current levels. (To watch Genovese’s track record, click here)

Genovese’s colleagues mostly agree. While one analyst remains on the sidelines, all 3 other reviews are positive, providing the stock with a Strong Buy consensus rating. The forecast calls for one-year gains of 113%, considering the average target clocks in at $21.20. (See ADTN stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.