Is the market truly ready for a sentiment shift? According to a recent BofA survey, there are signs the foundations for one are taking shape right now.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

The survey showed that the average cash level in investors’ portfolios in October hit 6.3%, a level not seen since April 2001 and some way higher than the long-term average of 4.8%.

So, there’s plenty of cash waiting on the sidelines and ready to be deployed. With the Fed potentially easing its monetary policy next year, BofA thinks a rally in the first half of 2023 is a real possibility.

A sustained rally will do good for the scores of stocks which have taken a sound thrashing in 2022 and are now trading at steep discounts.

With this in my mind, we delved into the TipRanks database and pulled out three names which fit a specific profile; all are down considerably this year but hold ‘Strong Buy’ ratings from the Street’s analysts, and boast triple-digit upside potential for the coming year. Let’s dig into the details, then, and find out why the experts are currently singing these stocks’ praises.

PLBY Group, Inc. (PLBY)

We’ll start with one of the world’s most recognizable brands. The pages of Playboy magazine were world famous for their combination of nudity and highbrow content with centerfolds sitting comfortably next to some of the world’s best writers. The magazine itself is no longer in print, but in recent years, Playboy has adapted to the modern era. Billing itself as a “pleasure and leisure” offering, the company has turned to the internet and now owns and operates several digital commerce retail platforms, in addition to online content platforms. It also sells plenty of sexual wellness products and licenses content for Playboy television, amongst other endeavors.

Playboy went public via the blank check route in February of last year. 2021 was a good year for the new SPAC stock, but it’s been thoroughly hammered in 2022’s bear market. The shares are down by a massive 87% since the turn of the year, a performance not helped by lackluster earnings such as in the latest financial statement – for 2Q22.

While revenue grew by 31.1% year-over-year to $65.4 million, that represented a slowdown from the two prior quarters. Additionally, the company showed a net loss of $8.3 million, which translated to EPS of -$0.18. Both figures missed the consensus estimates, and given the deteriorating economic backdrop, Playboy also took its FY22 outlook off the table. The company said it had put in place a strategic review to pinpoint the areas where it can reduce costs whilst also taking steps to bolster the balance sheet.

While cognizant of the current issues and heeding patience, Canaccord analyst Jason Tilchen remains firmly in Playboy’s corner.

“Shares of PLBY have remained under pressure as operational miscues have been compounded by easing demand and a lack of near-term visibility. While it may take several quarters for PLBY Group to show investors it is making progress on strategic initiatives, the stock price likely reflects much of these challenges, and we continue to see the current valuation as attractive for an iconic global brand such as this one,” Tilchen opined.

Accordingly, Tilchen rates PLBY shares a Buy while his $14 price target suggests the stock is undervalued by a hefty 324%. (To watch Tilchen’s track record, click here)

Overall, PLBY has garnered 5 analyst reviews over the past few months which break down 4 to 1 in favor of Buys over Holds, all culminating in a Strong Buy consensus rating. At $9.2, the average target implies one-year share appreciation of a robust 178%. (See PLBY stock forecast on TipRanks)

Porch Group (PRCH)

Next up is Porch Group, a company which began as a home services marketplace. However, over the years, it has transformed itself into a vertical software company that provides solutions to home service companies while also offering insurance and warranty products. All are designed to connect the dots between homeowners and service providers and offer a better home buying and ownership experience. Such is its reach, that today Porch plays a part in roughly 2 out of every 3 U.S. homebuyers’ activities every month.

The housing market has felt the force of the economic downturn and the company attributed the faster-than-anticipated slowdown and inflationary environment as the reasons behind a disappointing Q2 report.

While revenue climbed ~37.8% year-over-year to $70.8 million, the figure fell short by 9.4% of the Street’s expectation for $78.1 million. Likewise, the company showed an Adj. EBITDA loss of -$14.3 million, missing consensus at -$8.9 million. Partly based on the ongoing macro headwinds, Porch also lowered its full-year 2022 guidance.

If we’re on the subject of beaten-down stocks, then Porch certainly fits the bill; the shares have been thoroughly destroyed this year and have fallen by a merciless 91%.

However, despite the uncertain macro outlook, Cantor analyst Josh Siegler remains “very constructive on Porch’s business” and believes the company has what it takes to withstand the current headwinds.

“Although the slowing housing market applies downward pressure on Porch’s revenue, we believe the company may be more insulated from housing cyclicality than some other firms tied directly to the housing market,” the analyst explained. “In 2022, Porch expects only ~30% of revenue to be tied to transactions, including moving services and B2B2C. It expects the remaining ~70% of revenue to come from recurring software and insurance.”

Conveying his confidence, Siegler’s Overweight (i.e., Buy) rating is backed by an $8 price target, indicating room for huge growth of ~452% in the year ahead. (To watch Siegler’s track record, click here)

Other analysts are hardly less bullish; at $7.88, the average target is only a smidgen below Seigler’s objective and could yield returns of 443% over the coming months. Barring 1 Hold, all 5 other analyst reviews are positive, making the consensus view here a Strong Buy. (See Porch stock forecast on TipRanks)

European Wax Center (EWCZ)

European Wax Center, as the name implies, provides out-of-home waxing services, and since forming in 2004, the operator/franchisor has grown at a fast pace and now boasts over 890 salons spread out across 44 states. That the company is a leader in its field is obvious due to the fact that by center count, it is 6 times larger than its nearest competitor. That name, however, is a tad misleading; European Wax Center is headquartered in Plano, Texas.

The company believes that on account of its high-earning customer demographic, its business model will be able to withstand the inflationary environment, although management did note following the release of Q2’s financials that the average time between visits was increasing, which suggests that even its customers were feeling the pinch of the economic downturn.

In the quarter, total revenue reached $53.4 million, amounting to an 11.4% year-over-year increase while same-store sales rose by 6.7%. However, adjusted EBITDA fell by 5.9% from 19.8 million in the same period a year ago to $18.6 million. As for the outlook, the company stuck to its prior guidance and raised its anticipated new center openings for fiscal 2022 from 83 to 85.

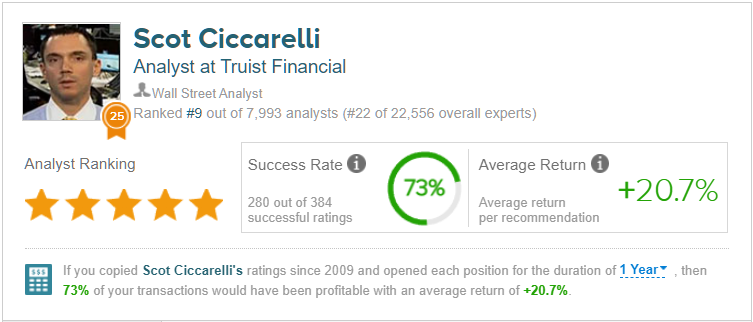

This is another name that has suffered badly at the hand of market forces; shares are down by 48% year-to-date. However, echoing the company’s comments regarding its ability to withstand the tough macro conditions, Truist’s 5-star analyst Scot Ciccarelli thinks EWCZ is well set up to do so.

“While inflationary pressures and mounting economic concerns continue to weigh on consumers, sales trends for the company remain strong, largely because many/most customers (female) view waxing as an ‘essential service’. Given the nature of its services and a seemingly more insulated customer base, we expect top-line trends to remain robust in an increasingly challenging macro environment,” Ciccarelli opined.

Overall, Ciccarelli believes this is a stock worth holding on to. The analyst rates EWCZ shares a Buy, and his $30 price target suggests a solid upside potential of ~113%. (To watch Ciccarelli’s track record, click here)

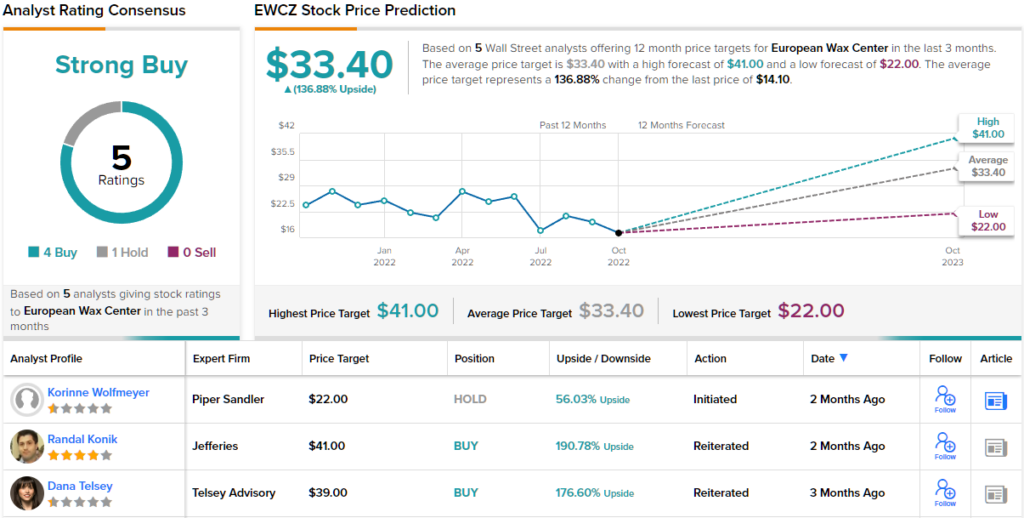

This is another stock the Street’s analysts are getting behind; EWCZ boasts a Strong Buy consensus rating based on 4 Buys vs. 1 Hold. The average target is even more bullish than Ciccarelli will allow; at $33.4, the figure represents upside of ~137% from current levels. (See EWCZ stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.