Should investors prepare for a winter full of persistent headwinds? Inflation remains high, rising interest rates are putting a squeeze on capital as well as making consumer credit more expensive, and both the China COVID lockdowns and the Russian war in Ukraine continue to crimp global supply chains.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

But even though the markets are facing serious headwinds, not every stock is going to react by falling. According to the analysts at Wall Street giant Deutsche Bank, two interesting stocks are likely to see substantial gains going forward.

Turning to the TipRanks database, we find that both are Buy-rated, and both have shown heavy losses in recent months, severely underperforming the broader markets. Even so, the Deutsche Bank analysts believe that these stocks have room to gain in 2023, on the order of 40% or more. Here are the details.

BlackSky Technology (BKSY)

We’ll start with a microcap satellite intelligence company, BlackSky. This company owns and operates a leading network of low earth orbit small satellites, and can capture imagery in a cost-effective, efficient matter wherever and whenever its customers require. BlackSky’s services include data processing on its Spectra AI software platform, which can integrate data from third-party sensors for critical insights and analytics. The company’s customer base includes US and international governmental agencies, as well as global commercial businesses and organizations.

BlackSky controls a substantial constellation of small satellites, and the company can bring multiple advantages to its customers. These include a 90-minute average product delivery, a 60 minutes average on satellite revisits, and up to 15 satellite revisits per location per day. In addition, BlackSky can provide direct satellite downlinks to both ground- and maritime-based operations.

All of this adds up to a solid business in a unique niche. BlackSky leveraged this to an impressive 113% year-over-year revenue gain in 3Q22, to a total of $16.9 million. This gain was powered by solid gains in imagery and software analytical services, which increased their share of total revenue to 89%. While BlackSky, like many cutting-edge tech firms, operates at a net loss, the EPS of -$0.12 beat the Street’s -$0.20 forecast.

Nevertheless, while BlackSky showed some impressive growth numbers this year, including a major contract with the US government’s National Reconnaissance Office (NRO), loss-making firms have been out of favor in 2022, and the company’s shares have fallen sharply. Year-to-date, BKSY is down 62%.

Covering BlackSky for Deutsche Bank, analyst Edison Yu notes that the company has had its difficulties recently – but also that it has built up plenty of momentum to carry through the next year.

“BlackSky has been inconsistent operationally but is laser focused on leveraging its flagship Spectra AI software to generate valuable actionable insights and is supported by lucrative government/defense contracts which we believe ultimately make it an attractive strategic target given the current depressed valuation… BlackSky is benefitting from higher customer activity related to Russia/Ukraine conflict and also other contracts coming in stronger… BlackSky is growing its sale force and network of partners, which should bring onboard more customers,” Yu opined.

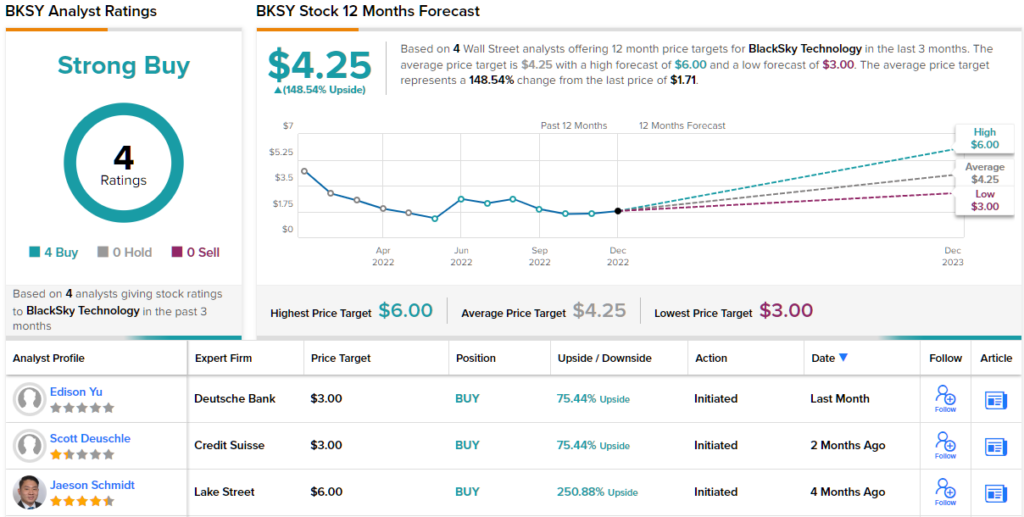

Considering BlackSky’s potential going forward, Yu rates the stock a Buy along with a $3 price target to indicate his confidence in a one-year gain of 75%. (To watch Yu’s track record, click here)

Turning now to the rest of the Street, other analysts also like what they’re seeing. 4 Buys and no Holds or Sells add up to a Strong Buy consensus rating. The shares are trading for $1.71 and their $4.25 average price target suggests a potential upside of ~148% for the next 12 months. (See BSKY stock forecast on TipRanks)

Coherent Corporation (COHR)

The second stock we’ll look at, Coherent, has a new ticker but a long history. Until July of this year, the company was known as II-VI, and held an important position in the silicon semiconductor chip industry. It still lives in that niche, designing and manufacturing precision equipment for engineered materials and optoelectronic component systems. But on July 1 of this year, the company completed its acquisition of Coherent, Inc., and starting on September 8, the combined firm adopted the Coherent name and began using the COHR ticker on the NASDAQ. Even though the company has taken on new branding, a new name, and a new ticker, it will continue to use the II-VI stock history in continuity with COHR.

On the business end, the new firm has added Coherent, Inc.’s laser technology to its own high-tech precision machining and optoelectronics. Overall, the combination is expected to bring added value to enterprise customers in the chip sector.

In the most recent quarter, Q1 of fiscal year 2023, Coherent saw a large sequential jump in revenues, from $887 million in fiscal 4Q22 to $1.34 billion in the current period. This was a q/q gain of 51%; year-over-year, the revenue gain came in at 68%. The strong revenue gain was supported by y/y organic revenue growth of 20%. Looking forward, Coherent can rely on a record work backlog of $3.05 billion, up 119% from the year-ago quarter.

Like many others, the stock has suffered badly in 2022; COHR shares are down more than 49% since the turn of the year.

However, noting the share price drop and the issues worrying investors, Deutsche Bank’s Sidney Ho takes an upbeat stance.

“COHR shares have underperformed the broader market year-to-date on fears that the growth of its organic business will decelerate and the newly-acquired legacy Coherent business has too much exposure to GDP-driven markets, while debt leverage post-deal is also too high. However, based on the company’s outlook and through our recent work, we believe investors’ concerns to be overly pessimistic,” Ho explained.

“We also believe some of the growth drivers in Comms, silicon carbide (SiC), sensing, semicap and display are underappreciated by investors, which will likely more than offset risks associated with the rest of business,” the analyst added.

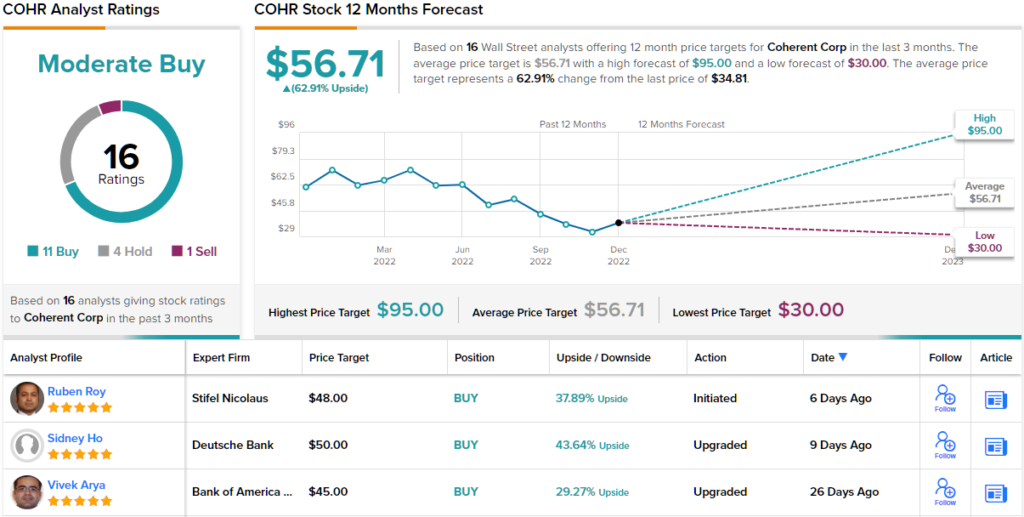

Considering the disconnect between the company’s share performance and its strong potential, Ho rates COHR as a Buy going forward, and sets a $50 price target that implies a one-year upside potential of ~44%. (To watch Ho’s track record, click here)

Overall, this chip-related tech company has picked up 16 recent reviews from the Street’s analysts, and these include 11 Buys, 4 Holds, and 1 Sell, for a Moderate Buy consensus rating. The average price target is $56.71, implying a bullish 63% upside from the current share price of $34.81. (See COHR stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.