Successful investors are also successful bargain hunters; buying low and selling high might be cliché, but it’s also a sure way to build up a profitable stock portfolio. The only trick to it is recognizing which low-priced stocks are the right ones to buy.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

It’s a trick because a stock may be down due to a whole range of circumstances, sometimes due to not quite meeting Street expectations and sometimes just due to shifting market dynamics, amongst other factors. The key, of course, lies in finding the names that have maybe taken too much of a beating and are poised for a recovery, making them ripe for the picking.

We’ve opened up the TipRanks database to look for bargain-priced shares, and found two that the Street’s analysts are tagging as solid Buys. Both are down by more than 40% so far this year – but both have analysts saying that they’re likely to jump sharply in the coming months. Let’s give them a closer look, to find out just what makes these beaten-down stocks stand out – and why the analysts are recommending to grab them now, before they rebound.

Li Auto (LI)

We’ll start by looking at Li Auto, one of the leading electric vehicle (EV) companies in the Chinese market. The company has built up a leading reputation as a producer of high-end electric drivetrains, a key technology field in the larger realm of EVs. Li bills its drivetrains as an important technical differentiator from the competition – another important point, in a field as crowded as China’s EVs. In addition to its technology and its lineup of full production electric cars, Li also boasts a network, across China, of dealerships and vehicle service centers to provide support for its customers.

Currently, Li has a family of electric SUVs in production. These vehicles include the L-series, launched in March 2024 and including the L7, L8, and L9. Also launched this year was the L6, which features extended range capability, provided by a four-cylinder gasoline combustion engine capable of engaging and recharging the battery when it runs low. The L6 is not a true gas-electric hybrid, as the gasoline engine is not capable of running the vehicle – the drivetrain is entirely electric.

The same cannot be said, however, for Li’s MEGA, also launched in March of this year. The MEGA is the company’s high-tech flagship MPV, with an 800-volt battery electric platform. The vehicle features a next-generation body design optimized for low drag and efficient energy consumption.

In Li’s most recent delivery update, for June of this year, the company announced delivery of 47,774 vehicles for the final month of the first half, a figure that was up an impressive 46.7% year-over-year. Li’s total 2Q24 deliveries came to 108,581, and the company’s total cumulative deliveries, as of June 30, 2024, were given as 822,345 vehicles, the highest among China’s emerging EV firms.

Li’s last earnings release, made public on May 20, covered 1Q24, and featured a top line of $3.6 billion in US currency. This was up more than 36% from the prior year, but it missed the forecast by $200 million. The company’s Q1 bottom line, of 17 cents per ADS, by non-GAAP measures, was 3 cents below the forecast.

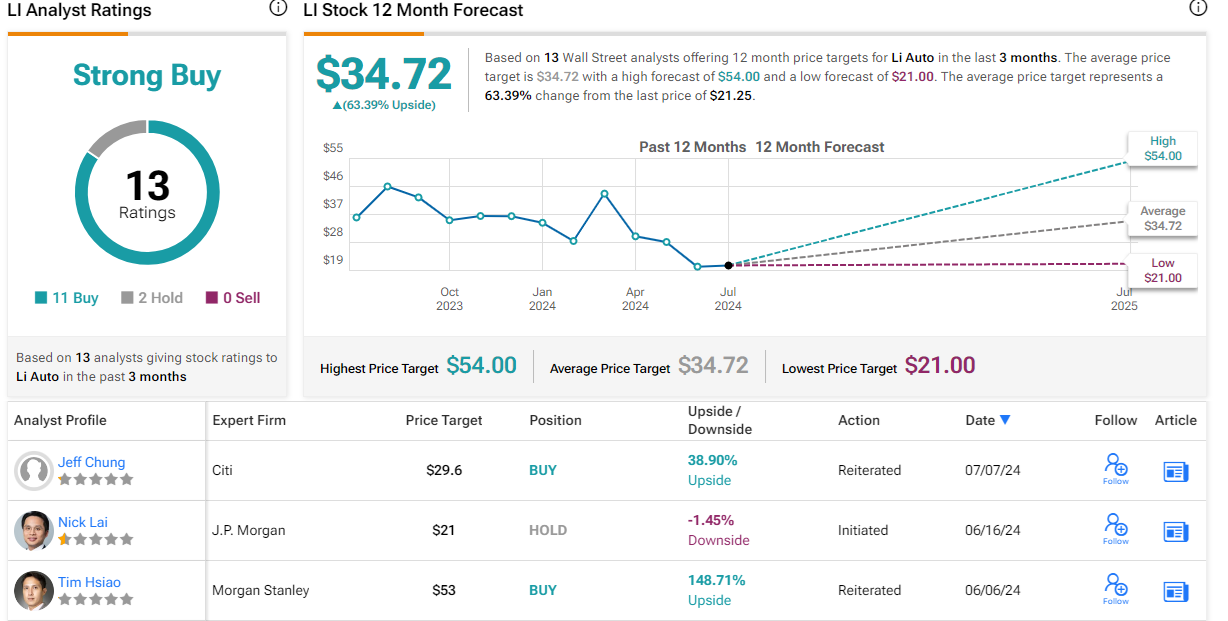

Shares in LI are down 43% so far this year, but Morgan Stanley’s Tim Hsiao thinks there could be an opportunity here for investors. “We think the stock has been punished by the missed expectations on the part of both management and the capital market, resulting in de-rating,” Hsiao explained. “With an average 30k monthly run rate in 2Q, US$10.5bn in net cash, and 18% vehicle margin (vs. guided 20%+), with minimal contributions from BEV and overseas, we think the company is worth revisiting with consensus’ expectations being reset materially.”

Looking ahead, Hsiao adds, “Although negative sentiment around deliveries, BEV recalibrating, competition, and macro risks could linger in the near term, we think the share price correction since its prior peak late in February 2024 should have more than discounted the fundamental disappointment. With the stock at 1x 2024e P/S (vs. peers at 1.1-1.2x) with reasonable profits and cash flow, we think investors may start to reconsider the potential for more positive outcomes at the company.”

The analyst goes on to maintain his Overweight (Buy) rating on the shares, and sets a price target of $53, pointing toward a robust 149% upside potential for the coming year. (To watch Hsiao’s track record, click here.)

There are 13 recent analyst reviews of this stock on file, and their breakdown of 11 Buys and 2 Holds gives LI a Strong Buy consensus rating. The stock is trading for $21.25 and its $34.72 average target price implies a 63% gain on the 12-month horizon. (See Li Auto’s stock forecast.)

Five Below (FIVE)

Next on our beaten-down list is Five Below, a relatively recent entrant to the discount store niche. The company was founded in 2002, and caters to lower-income customers as well as tweens and teens, offering a wide variety of discount and specialty goods, mainly priced at $5 or lower. The company is based in Philadelphia, Pennsylvania, and the chain counts more than 1,600 stores across 43 states.

The discount store niche has been showing strength in the early 2020s, especially during the pandemic lockdown period when customers were looking for bargains. While that trend is fading, the company still registered a total of $3.56 billion in sales last year, and saw a compound annual growth rate of 18% in the last 6 full years (2018 through 2023). Despite this solid background, however, the company’s stock is down more than 51% for the year-to-date.

A look at the company’s fiscal 1Q24 report, the last released, may help explain why. The report covers the fiscal quarter that ended on May 4 of this year, and it missed the forecasts at both the top and bottom lines. Revenues, at $811.9 million, were up almost 12% year-over-year – but were also more than $22.5 million below expectations. The company’s quarterly bottom line, of 60 cents per share by non-GAAP measures, was 3 cents per share less than had been anticipated.

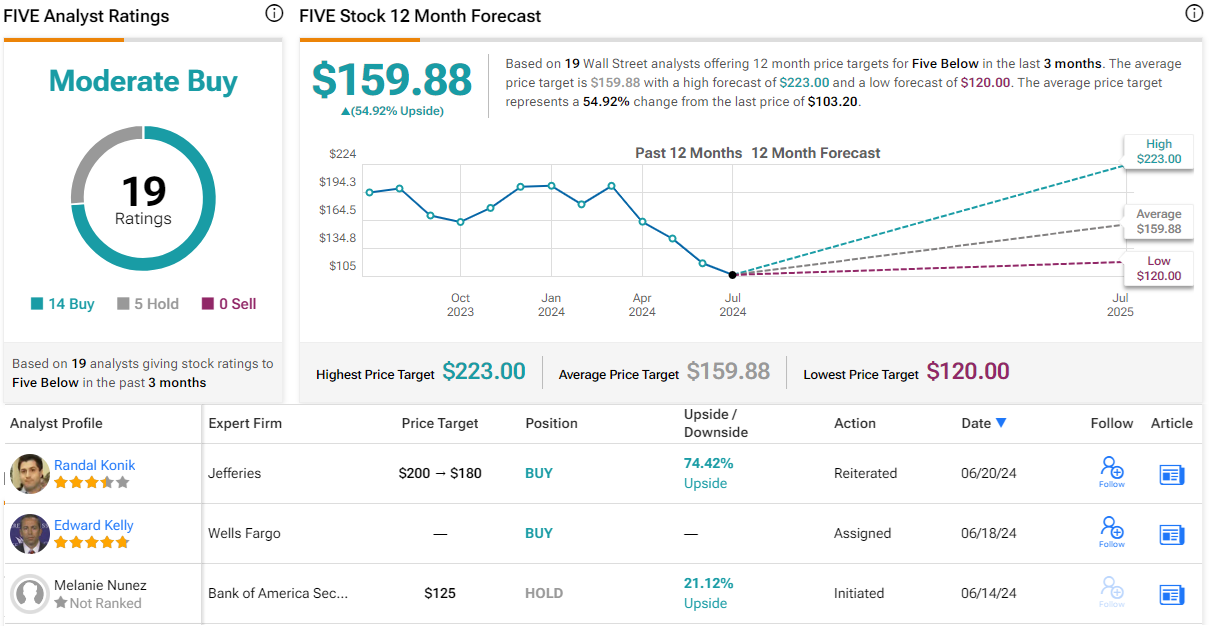

Nevertheless, covering this stock for Jefferies, analyst Randal Konik sees plenty of underlying positives in this company. He says of Five Below, “We like FIVE’s value-oriented offering, nimble and scaling business model, ample real estate growth opportunity, and the upside potential offered by Five Beyond. We see a path to FIVE’s LT store-count target of 3,500 units, which we think may be conservative. The inclusion of higher-price-point products in its assortment should enhance FIVE’s value offering and yield many benefits.”

These comments back up Konik’s Buy rating, and his $180 price target implies that the stock has a one-year upside potential of 74.5%. (To watch Konik’s track record, click here.)

The 19 current analyst reviews of this stock include 14 Buys and 5 Holds, giving the shares a Moderate Buy consensus rating. The stock is trading for $103.20 right now, and its average target price, at $159.88, suggests it has an upside potential above 55% this coming year. (See Five Below’s stock forecast.)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.