The current economic situation is turbulent for investors, to say the least. From the threat of a looming recession to high inflation, current market conditions mean that it is becoming increasingly difficult for investors to predict what’s happening next.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Wall Street’s analysts, however, are up to the task, and from BMO, chief investment strategist Brian Belski has noted some important factors that investors will need to consider.

First, in Belski’s view, is the fact that bear markets typically end during a recession rather than afterwards, and second is that recession indicators are typically lagging indicators. Taken together, this means that we likely won’t know exactly when a bear ends when it happens, but only some months later. For Belski, this means that investors need to start preparing now the return of bull market conditions.

“It is safe to say that the current tightening cycle is nearing an end, which has historically been a positive for US equity performance,” Belski opined.

So, let’s find some stocks that are primed for gains. Using TipRanks’ database, we identified two names that feature both low prices now – and solid upside potential for the coming year. Not to mention each one gets a “Strong Buy” consensus rating from the analyst community. Let’s dive in and find out what’s driving that prospect.

Tremor International (TRMR)

First up is Tremor International, an ad-tech company offering users a platform optimized for video, data, and CTV capabilities. The company focuses on providing end-to-end solutions in the video advertising world. Tremor has a global reach, and is rapidly expanding its footprint in the realm of connected TV.

Digital advertising has faced severe headwinds given the rising and stubbornly high inflation of the past two years. Advertisers have had to retrench in the face of increased costs, and have pulled back on their ad budgets; companies like Tremor have been feeling the effects. While we won’t see Tremor’s latest financial results until next week, when it reports 4Q22, we can look back at Q3 and see how the company has been faring.

At the top and bottom lines, Tremor has reported declines. Revenues was down 19% year-over-year, to $70.1 million, while adjusted earnings came in at $30.1 million – down 28% y/y. That was the headline bad news. On a positive note, the company did maintain its strong margins in 3Q22, with an adjusted EBITDA margin of 43%. Tremor has deep pockets, too, reporting a net cash position of $109.1 million as of September 30 last year.

Slipping revenues and earnings, however, are not the only story here. Last summer, as inflation was roaring and the company’s earnings were declining, Tremor was confident enough to acquire a competing global ad platform, Amobee. The move, a strategic acquisition that combines Tremor’s and Amobee’s assets into one of the market’s largest CTV and video ad platforms, was valued at $239 million.

Also last summer, Tremor closed its investment in VIDAA, a smart TV operating system and streaming platform. Tremor’s move was a $25 million equity investment into VIDAA, which it covered through cash resources.

The story here is a company that is facing headwinds, but has the wherewithal to survive a difficult time. Overall, for the past 12 months, Tremor shares are down 49%.

Tremor has been attracting positive attention from Wall Street analysts, who see the low price as an attractive entry point.

Among the bulls is Lake Street analyst Eric Martinuzzi who writes: “After a difficult 2022, in which demand for Tremor International’s ad services contracted and earnings declined, we believe recent events have the company teed up to return to growth…. We believe the company is on a sustainable path for growth and expect the valuation gap to close as investors better appreciate the upside. Despite the negative market sentiment towards TRMR shares, we believe the stock’s low valuation creates a high floor.”

To this end, Martinuzzi rates Tremor shares a Buy, while his $12 price target implies a one-year gain of 54% for the stock. (To watch Martinuzzi’s track record, click here)

The Lake Street view is not the only bullish take – there are three recent analyst reviews on file here and all are positive, for a Strong Buy consensus rating. The shares are trading for $7.77 and the $12.33 average price target suggests ~59% upside in the next 12 months. (See TRMR stock forecast)

Nurix Therapeutics (NRIX)

Next up is Nurix Therapeutics, a biopharmaceutical firm at the clinical trial stage. Nurix has a pipeline of drug candidates designed to work on proteins, either through the targeted protein degradation, or through the opposite, targeted protein elevation. The company’s small-molecule therapeutic agents are under study for their application in a wide range of cancers; the company currently has a few Phase 1 clinical trials underway, and several additional programs in pre-clinical testing.

The Phase 1 clinical trials feature two leading drug candidates from the protein degrader portfolio, NX-2127 and NX-5948. The first of these, 2127, is the subject of a Phase 1a/1b clinical study in the treatment of adults with relapsed or refractory B cell malignancies, and a clinical update is expected from this study in 2H23. The company is also looking to define a regulatory strategy for this drug candidate, based on FDA feedback.

The second program, 5948, is also at Phase 1 in the treatment of adults with relapsed or refractory B cell malignancies; however, the drug candidate’s therapeutic action is differentiated from that of 2127 by the lack of cereblon immunomodulatory activity. Data should be available from the Phase 1a portion of this study in 2H23. Also later this year, Nurix expects to define the dosing for the Phase 1b cohort of this program.

Also coming up this year, Nurix expects to move another drug candidate from pre-clinical to clinical testing. And, finally, the company expects to achieve multiple milestones on its collaboration agreements with Sanofi and Gilead, which will boost the company’s bottom line.

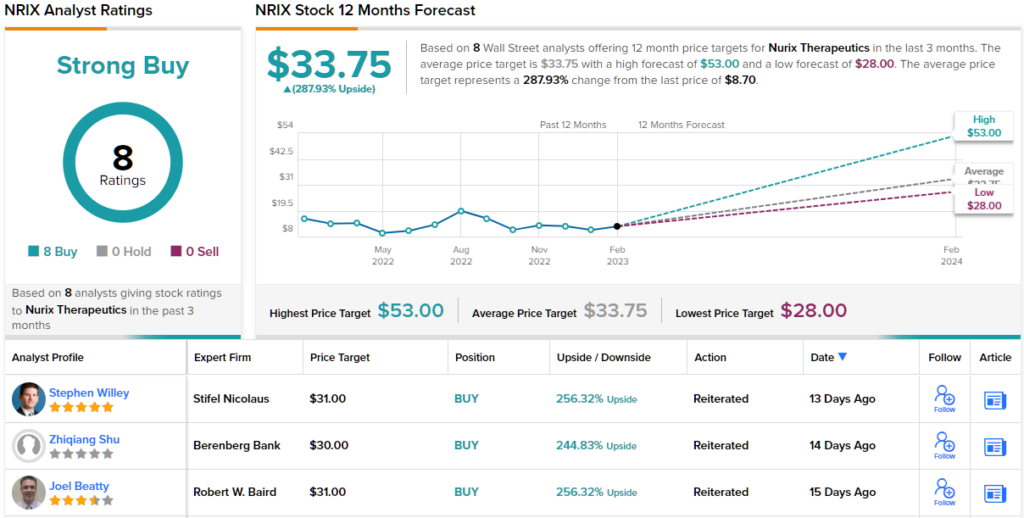

All that said, we should note that the last 12 months have seen Nurix’ shares drop 46%. In the view of Baird analyst Joel Beatty, however, this adds up to an attractive stock.

With a low price and plenty of upcoming catalysts, Beatty writes of Nurix: “We view NRIX as an attractively-priced protein modulation platform stock, with strong scientific validation for its stage of development. We believe clinical data updates in 2H23 for each of the three lead clinical programs provide attractive risk/reward… Achievement of additional milestones from collaborators should help provide support for a floor value in 2023, and add non-dilutive funds to extend the company’s cash runway,” Beatty opined.

In concrete terms, this adds up to an Outperform (i.e. Buy) rating, and Beatty’s $31 price target suggests a robust one-year upside potential of 256%. (To watch Beatty’s track record, click here)

Overall, all 8 of the recent analyst reviews on this stock are positive, making the Strong Buy consensus rating unanimous. Nurix’ stock is priced at $8.70, and the average price target, now at $33.75, is even more bullish than Beatty allows, implying a ~288% potential gain for the year ahead. (See Nurix stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.