To presume that we have reached a market bottom would be thoughtless. This is one of the wildest environments the capital markets have seen in decades, and the truth is, nobody knows if there is more room for equities to descend. Nevertheless, with the S&P 500 (SPX) down roughly 22% from its highs and the Q3 earnings season starting rather favorably, it may be sensible for investors to start considering which equities may have indeed bottomed out.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

In my view, one industry, in particular, may include equities that have gotten too cheap to pass on at current price levels – like TGT and LOW. In particular, the share prices of giant retailers have already suffered quite dramatically while some of their prior headwinds have apparently started to relax.

Why Retailers Could be an Attractive “Rebound” Play

Assuming that the general market sentiment may be headed for a reversal, retailers could be bearing significant upside as their stock prices have remained depressed despite the industry’s outlook improving lately.

One of the harshest challenges the industry has undergone lately comprised soaring shipping costs amid the supply-chain crisis that persisted following the COVID-19 pandemic. Last month, we discussed how supply-chain bottlenecks impact e-commerce stocks, but conventional retailers were equally harmed by surging freight costs.

Containership freight rates may still be more than twice their 2017-2020 levels, but they have corrected by nearly 70% from last year’s highs. This should reduce transportation costs for retailers and allow for inventory management optimization, which is likely to lead to an expansion in margins and, thus, higher profits.

Further, most major U.S.-based retailers do not have noteworthy international exposure. This is important to note, as the ongoing strength in the dollar should not result in any meaningful foreign exchange headwinds.

Finally, inflation levels may remain quite elevated. However, most retailers operate within the consumer defensive sector, which is the one sector that should withstand highly-inflationary environments rather firmly.

Consumers will frequently stop by retail stores to purchase their everyday necessities – products whose demand is highly inelastic and mostly uncorrelated to the underlying state of the economy.

Even home improvement retailers (which are included among consumer discretionaries) should perform well as consumers may prioritize improving their homes during a market downturn versus buying property – especially with rates on the rise.

In my view, as retailers adjust to these factors and the new reality, including the possibility that above-average inflation levels shall be the new normal for a while, their earnings growth should quickly resume. Wall Street analysts seem to agree with this argument.

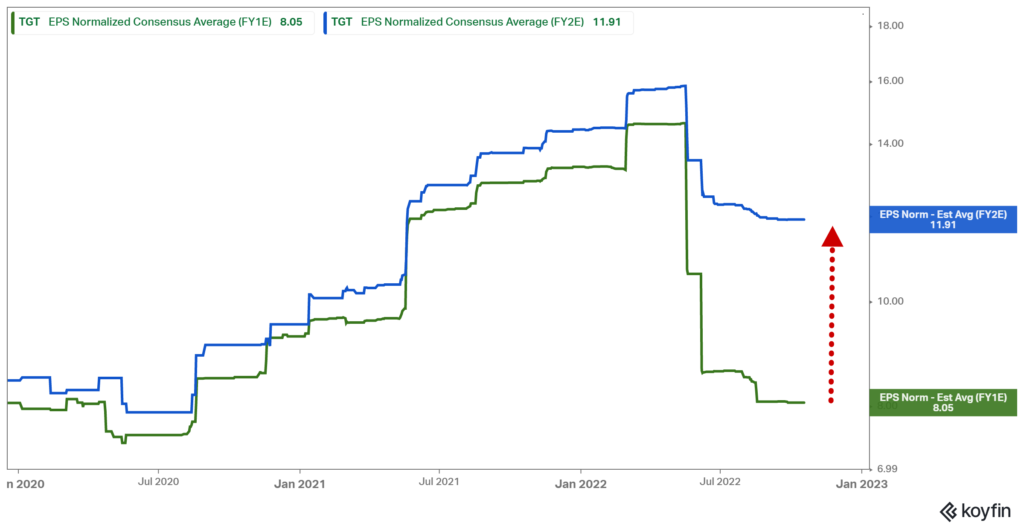

Take Target Corporation (NYSE: TGT), for instance. While the company is expected to post Fiscal 2022 earnings per share close to $8.00, implying a year-over-year decline of around 40%, earnings are then expected to rebound by nearly 48% in Fiscal 2023.

This seems to be a consistent trend in the industry. Let’s consider Walmart (NYSE: WMT) too. The company’s earnings per share for this year are expected to decline by 9.4% to $5.85 but rebound by nearly 13% to $6.60 by next year.

Which Retailers Should You Go For?

As I mentioned, we simply can’t know if equities, including retailer stocks, have further room to decline. Any exogenous shock can easily sway the markets forcefully in either way these days.

Therefore, I would go for quality names that trade at a discount while also offering strong dividend prospects. This is in order to have as much of a wide margin of safety as possible against further share price declines.

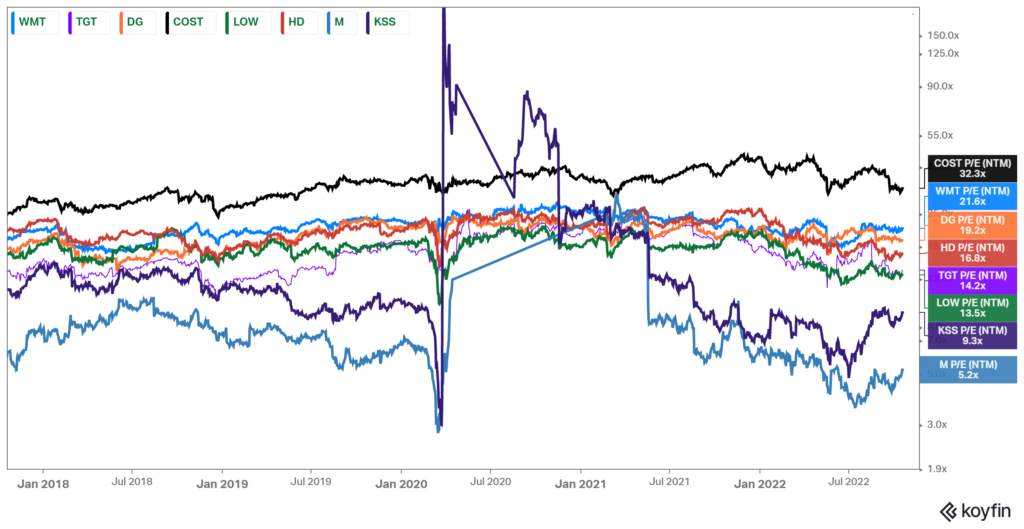

Thus, while Kohl’s Corporation (NYSE: KSS) and Macy’s (NYSE: M) are trading at forward P/Es in the single digits, I wouldn’t touch them since their qualities are questionable and their balance sheets are poor.

Simultaneously, while Costco Wholesale Corporation (NASDAQ: COST) is arguably one the highest-quality names amongst its peers, paying 32x its forward earnings in a rising-rates environment is crazy in my book.

Then, you have Target and Lowe’s Companies (NYSE: LOW), which trade at reasonable multiples while offering quality dividends. For context, the two companies have hiked their dividends for 60 and 54 years, respectively. This makes for a great validation in terms of their ability to generate robust cash flows and keep providing investors with growing payouts even during the harshest economic environments.

Sure, Walmart also boasts 50 years of successive dividend hikes, and I consider it a quality company too. However, by paying 23x times forward earnings, there is a large crack for an investor’s total-return prospects to be impaired should markets decide to move further south.

Conclusion: Go for Cheap, Quality Retailers

All around, I think that if we are indeed nearing a market bottom, giant retailers are likely to be proven fruitful investments following their steep share price declines.

Supply-chain bottlenecks are easing, which should allow for a potential expansion in margins, while their robust pricing power should make for a great advantage during the current highly-inflationary environment.

Still, make sure you get solid value for what you’re paying for and that there is a strong dividend attached to the stock of your choice. This way, even if the market goes south in the short term, you are still invested in a quality company you feel comfortable holding over the long term. Enjoying growing payouts in the meantime is a great plus as well.