Veeva Systems (NYSE:VEEV) stock has suffered a more than 50% haircut since peaking back in the middle of 2021. The niche cloud software company serves clients in the life sciences industry with hit products such as Veeva CRM (Customer Relationship Management) and Veeva Vault. Like most other niche software plays that heated up in 2020-21, VEEV stock has now gone bust after years of booming on the back of low rates and investor enthusiasm.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Though analysts have lowered the bar on their price targets in recent months, most analysts remain upbeat on the name for 2023. I’m bullish on VEEV as it navigates a higher-rate world en route to winning more business within a very niche market where it’s a standout player.

Despite lowering the bar modestly for its coming quarter, due on February 28, management still sees “strength” in its “innovation engine.” At this juncture, I think investors are losing track of the longer-term growth story at hand due to recent macro headwinds that I view as temporary in nature.

For context, management’s Fiscal Q4-2023 outlook called for $1.05 in EPS, two cents shy of the original consensus estimate. The current Q4 EPS estimate stands at $1.04.

Veeva’s innovation engine will likely shine through once macro headwinds have a chance to blow over. For now, investors aren’t nearly as willing to pay up for growth as they were just a year ago.

With a new line in the sand following the firm’s vicious sell-off, questions linger as to how much investors should value continued growth in a more challenging environment.

VEEV Ended 2022 Near Lows, Even after Sound Q3

The company closed off 2022 on a pretty low note despite clocking in a fairly decent third-quarter earnings beat. Per-share earnings came in a $1.13, just ahead of the $1.07 consensus estimate. Meanwhile, revenues rose 16% year over year.

With shares trading at around 66.5 times trailing earnings and 12.5 times sales, VEEV stock is trading at a discount relative to its five-year historical average multiples of 95.6 and 23.7, respectively, making it relatively attractive on this basis. Back in 2020, VEEV stock commanded a price-to-sales (P/S) multiple north of 30 times.

Still, it’s tough for a lot of investors to justify paying more than 60 times earnings for a firm whose sales growth has slid to the mid-teens.

It’s unlikely Veeva stock will command such a pie-in-the-sky multiple again now that higher rates have knocked the hyper-growth plays off their podiums.

In any case, I view Veeva as a company that will rise from the tech bust of 2022. The company has really found a spot with customers within its niche and, like most Sofware-as-a-Service (SaaS) companies focused on specific industries, I expect Veeva could benefit from significant cross-selling opportunities over time as it continues to win over new customers in a niche where Veeva has impressed.

Veeva: Slated to Move on from Salesforce’s CRM Platform

Last year, Veeva noted its plans to move on from the Salesforce (NYSE:CRM) CRM to its own platform in time. Indeed, it’s a good sign to hear that a firm is ready to use its own offering over that of a long-time partner. As a part of the transition, Veeva could be hit with expenses relating to the migration. In a rising-rate environment, that’s the last thing investors want to hear.

That said, such costs aren’t expected to weigh down results anytime soon, as the potential costs associated with the ending of the Salesforce-Veeva relationship aren’t expected to kick in until 2025.

If all goes smoothly with the transition, Veeva may be able to enjoy long-lasting cost savings from the move. If anything, it was worse news for Salesforce than Veeva, given the storm of headwinds the CRM kingpin has endured over the past year.

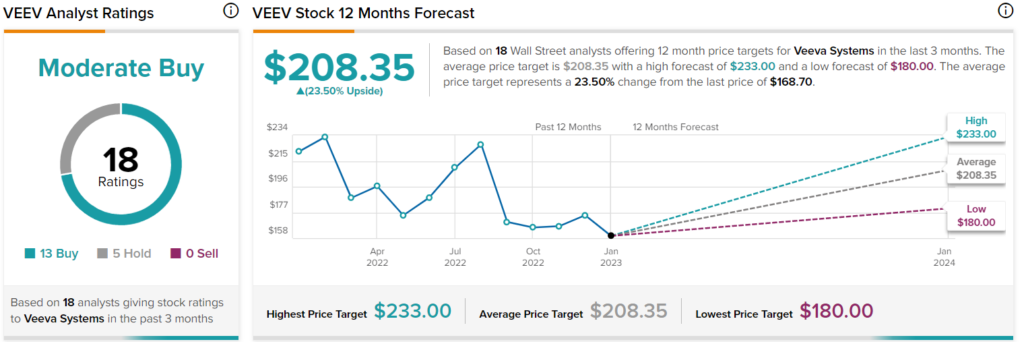

Is Veeva Stock a Buy, According to Analysts?

Turning to Wall Street, VEEV stock comes in as a Moderate Buy. Out of 18 analyst ratings, there are 13 Buys and five Holds.

The average Veeva price target is $208.35, implying upside potential of 23.5%. Analyst price targets range from a low of $180.00 per share to a high of $233.00 per share.

The Bottom Line on VEEV Stock

Veeva’s high revenue retention rate (a metric that measures the amount of revenue a company retains over a given period, expressed as a percentage) of 119% as of the last quarter speaks a lot about how customers view the platform. This means that the company retained 100% of its subscription revenue compared to last year and then added more on top of that.

It’ll be tough sledding for Veeva as more macro headwinds move in, but further out, I view Veeva as a dominant growth story that can form a moat around a niche market that still has plenty of growth runway.

Join our Webinar to learn how TipRanks promotes Wall Street transparency