There’s no denying we’re in a bull market. Over the past 18 months, with only a few blips, the markets have been trending upwards – and usually at a fast clip. Such rallies inevitably raise a few questions, particularly: how long will it last?

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

A recent note from J.P. Morgan explains why current conditions may indicate that we may not be anywhere near the end of this rally. Writing for the investment bank, global investment strategist Sarah Stillpass notes, “If this bull market merely matches the median, it could last another two years and come with an additional ~60% cumulative return. Given the strength of the market over the last nine months, we aren’t surprised that some investors are feeling ‘rally fatigue’ or think the market is due for a correction. But history indicates that time is on the bull’s side.”

Stillpass argues that investors should not shy away from buying at record high prices, adding, “The market has made an all-time high in one out of four trading sessions this year. While some investors are reticent to ‘buy high,’ the data suggests that investing at highs has not notably impacted returns. In fact, over the last 50 years, investors were better off getting invested at an all-time high than they were on any other day.”

The stock analysts at JPM are following this line and suggesting stocks to buy amid this market rally. And they are not the only ones recommending to buy in; according to the TipRanks database, both names have earned ‘Strong Buy’ consensus ratings from the Street. Here are the details and the JPM analyst comments.

Edgewise Therapeutics (EWTX)

We’ll start with Edgewise Therapeutics, one of the biotech industry’s many clinical-stage biopharmaceutical firms. Edgewise focuses on serious muscle diseases, of the skeletal muscles and the cardiac muscles. The company currently has two main drug candidate programs, addressing root causes of muscular dystrophy and hypertrophic cardiomyopathy. These drug candidates were developed using an approach that targets muscles as organs, creating small molecule agents that target specific proteins in muscle tissues.

Edgewise’s leading program studies candidate EDG-5506 – also called sevasemten – as a treatment for various muscular dystrophies, including Becker and Duchenne. Becker is a form of the disease with no currently approved treatments, and Edgewise’s drug candidate is currently undergoing several trials on this indication. These include the CANYON Phase 2 placebo-controlled trial in adult patients, with data expected in 4Q24, and the DUNE Phase 2 exercise challenge trial in adult patients. Preliminary data from the DUNE trial will be used in conjunction with already-published data from the 2-year ARCH open-label trial, to support the hypothesis that sevasemten can limit contraction-induced muscle damage and potentially halt disease progression.

The company’s second program involves EDG-7500. This drug candidate is under investigation as a potential treatment for hypertrophic cardiomyopathy (HCM). This is a serious heart disease, caused by abnormal thickening of the cardiac muscle walls, primarily in the left ventricle. The disease is inherited, chronic, and progressive in nature, and can cause complications including heart failure, stroke, or atrial fibrillation. EDG-7500 is described as a ‘first-in-class oral, selective, cardiac sarcomere modulator,’ intended to slow down early contraction velocity and also to improve cardiac relaxation. The drug candidate is undergoing a Phase 1 to evaluate safety and tolerability, and in April of this year the company dosed the first patient in the CIRRUS-HCM Phase 2 trial, a study of EDG-7500 in the treatment of adult patients with obstructive HCM. The study is scheduled to take place at 20 clinical sites across the US. Early data from these trials is expected to be available during 3Q24.

We should note here that this biopharma company’s drug candidates have impressed industry experts, and that EWTX stock has gained an impressive 178% in the last 12 months.

When we turn to the JPMorgan view, we find that biotech expert Tessa Romero is upbeat on Edgewise – and that her stance is based in large part on the potential of the drug candidates EDG-7500 and sevasemten. She writes, “At a high level, we think the upcoming EDG-7500 data later this year could represent the start of derisking of this novel mechanism in the clinic in HCM (with more to learn in 2025) and also note the broader optionality in the pipeline in other diseases (e.g., heart failure). Furthermore, we think that sevasemten could also offer additional opportunities for upside and are particularly intrigued by the BMD results so far. EWTX remains on U.S. Equity Analyst Focus List as a Growth Idea.”

Romero goes on to rate EWTX shares as Overweight (i.e. Buy), with a $30 price target that implies a 40% upside potential for the coming year. (To watch Romero’s track record, click here)

Overall, the JPM view is at the low end of the upside outlook here. This stock’s Strong Buy consensus rating is unanimous, based on 6 positive analyst reviews, and the $34.60 average price target suggests a 62% one-year upside from the current trading price of $21.36. (See EWTX stock forecast)

Tyler Technologies (TYL)

The next stock we’ll look at is a software company, Tyler Technologies. This company is a specialist, designing and offering software products and solutions for use by government entities and other public sector actors. The company’s products include a wide range of software packages, featuring secure data, easy maintenance, and public transparency. The company’s software products are used at all levels of government, from cities to counties to states to the Feds, and are found in court systems, K-12 school systems, health and human services departments, and more.

Providing services and technology for government – at any level – has long been a profitable endeavor, and Tyler has not only been succeeding, it has been expanding. Early this month, the company announced an agreement with the Arizona Supreme Court, to provide enterprise supervision solutions for juvenile probation services in all of the state’s 15 counties. The company has also launched a partnership with the New Jersey Motor Vehicle Commission, for an electronic lien and title service. In addition, the company has been opening new offices and facilities, in Maine and Tennessee.

In its last set of financial results, Tyler reported several strong positive metrics. First among these was the top line revenue, of $512.4 million. This was up more than 8% year-over-year, and beat the forecast by $4.45 million. Within the revenue total, recurring revenues from maintenance and subscriptions came to $430.5 million, or 84% of the total. These recurring revenues were up 8.8% year-over-year. The company’s subscription revenues, at $313.2 million, were up 11.7% from the prior year. Tyler’s bottom line figure, the non-GAAP EPS of $2.20, was 20 cents per share better than had been expected, and was up 25% year-over-year.

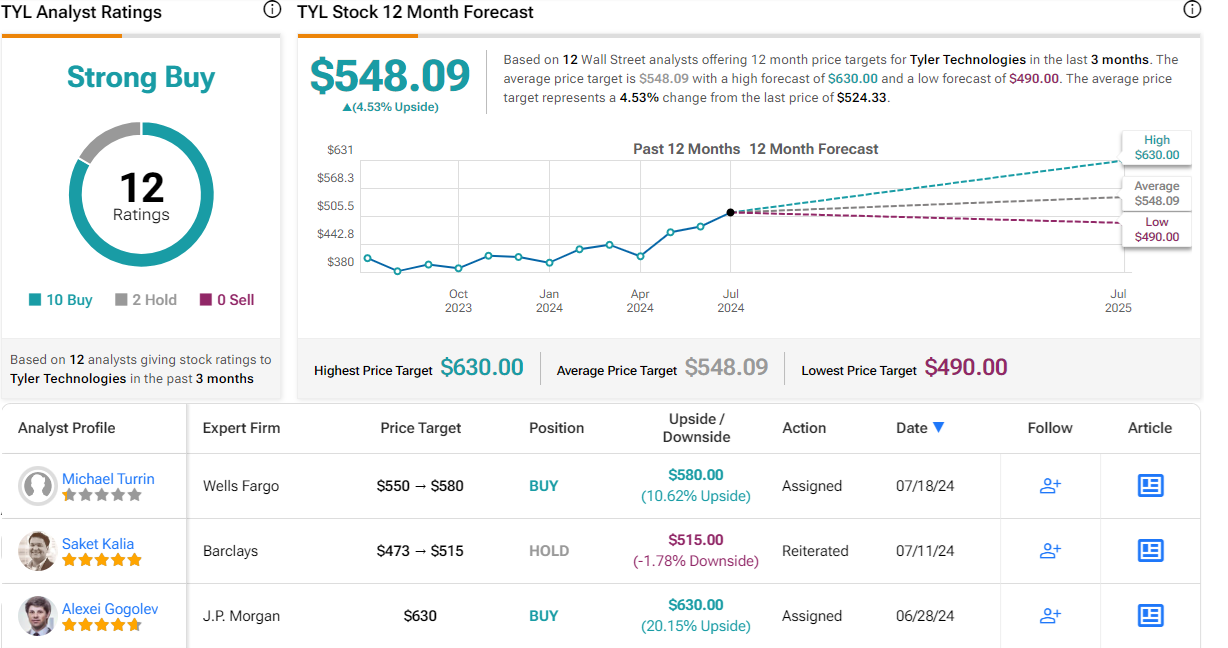

For 5-star analyst Alexei Gogolev, this company’s potential for expansion, on top of its recent growth, is the key point. He says of Tyler, “There is still significant runway for TYL to expand its footprint in public sector software. Accelerating revenue growth and better than guided margin expansion are likely to be key near-term catalysts for TYL shares and could become apparent to the Street over the next few quarters. Considering accelerating top-line growth and improving margins, which are likely to prompt management to raise their mid- and long-term guidance, we are adding Tyler shares to the J.P. Morgan Analyst Focus List (AFL) as a high-conviction OW among vertical software names.”

Along with that Overweight (i.e. Buy) rating, Gogolev sets a $630 price target that indicates room for a 20% upside on the one-year horizon. (To watch Gogolev’s track record, click here)

TYL shares have a Strong Buy consensus rating, based on 12 recent reviews that include 10 Buys and 2 Holds. The shares are trading for $524.33, and their $548.09 average target price implies a modest one-year upside of 4.5%. (See TYL stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.