The bulls took hold of the stock market narrative at the start of the year, and charged ahead all the way into mid-summer, but since then the bears have been rather noisy. On the back of rising oil prices, fears of interest rates staying high for longer than hoped for, and the possible prospect of a recession still looming, the markets have been shaky and have been handing back prior gains.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

However, against a backdrop of a ‘Goldilocks economy,’ i.e., “not too hot, not too cold… just right,” billionaire investor Ken Fisher thinks it’s all just a repeat of a scenario that played out earlier in the year.

“Recall how at the start of the year dire bearishness, with expectations of a recession, was in vogue,” says the Fisher Investments founder. “Since spring 2022, bears swore Fed hikes, with a list of other worries – Ukraine and Silicon Valley Bank among them – would kneecap GDP which they believed necessary to slow inflation.”

But Fisher notes inflation has meaningfully retreated from June 2022’s high of 9.1% (it is now at 3.67%), while GDP growth has exceeded expectations and claims most of the negativity is “hyperbole – multiple bouts of hand-wringing for every actual market break of short-term, downside volatility.”

These pullbacks are just a common feature of “young bull markets,” and the fact Goldilocks showed up is a sign people can “envision a better future.”

“Rather than getting too wrapped up in it,” Fisher concludes, “I’d advise you to stay put and keep eating your own porridge.”

That is exactly what Fisher is doing. Befitting someone who thinks the bearish noises only offer an unpleasant distraction to the ongoing bull market, Fisher, who has a net worth of ~$7.1 billion, remains heavily invested in certain equities. We ran pair of his picks through the TipRanks database to see what the Street experts make of their chances. Here are the details.

Oracle Corporation (ORCL)

For our first Fisher-backed stock, we’ll turn our attention to a software giant. Oracle is a globally renowned American multinational tech firm and since being founded in 1977, has evolved into a company boasting a market cap over $290 billion.

Oracle has a rich history in database management systems, and over the years has expanded its portfolio to encompass a wide range of software and cloud-based solutions, including customer relationship management (CRM), enterprise resource planning (ERP), human capital management (HCM), and cloud infrastructure services.

However, Oracle’s influence extends beyond its software and cloud solutions. The company is known for its hardware products, including servers and storage systems, which complement its software offerings. This combination of hardware and software allows Oracle to provide integrated solutions designed to meet the complex needs of large enterprises and organizations.

That said, Oracle might be an industry giant, but it hasn’t all been smooth sailing recently. After strong FQ3 results, the latest quarterly readout was a mixed affair. In the first quarter of fiscal 2024 (August quarter), revenue climbed by 8.7% year-over-year to $12.45 billion, falling just shy of expectations – by $20 million. And while cloud revenue increased by 29% year-over-year to $4.6 billion, that was well under the 55% y/y growth seen in F4Q23. On the other hand, there was a beat on the bottom-line, as adj. EPS of $1.19 came in ahead of the forecast by $0.04.

For Ken Fisher’s part, he remains long and strong here. His current ORCL holdings total 18,537,261 shares, amounting to a market value of $1.98 billion.

Oracle also gets the support of HSBC analyst Stephen Bersey, who sees good times ahead for the tech giant.

“After many years of its low- to mid-single digit organic top-line growth, we see the potential for Oracle to accelerate turnover growth and to drive earnings growth at a rate above revenue growth as we also see the potential for OPM (Oracle process manufacturing) expansion,” the 5-star analyst said. “Oracle has been building out its global cloud infrastructure, and as these cloud centers are completed, the work of selling and deploying begins. We believe that Oracle is at a turning point given its inventory of globally dispersed cloud centers and that selling momentum could be building, which we reflect in our near-term estimates for turnover growth.”

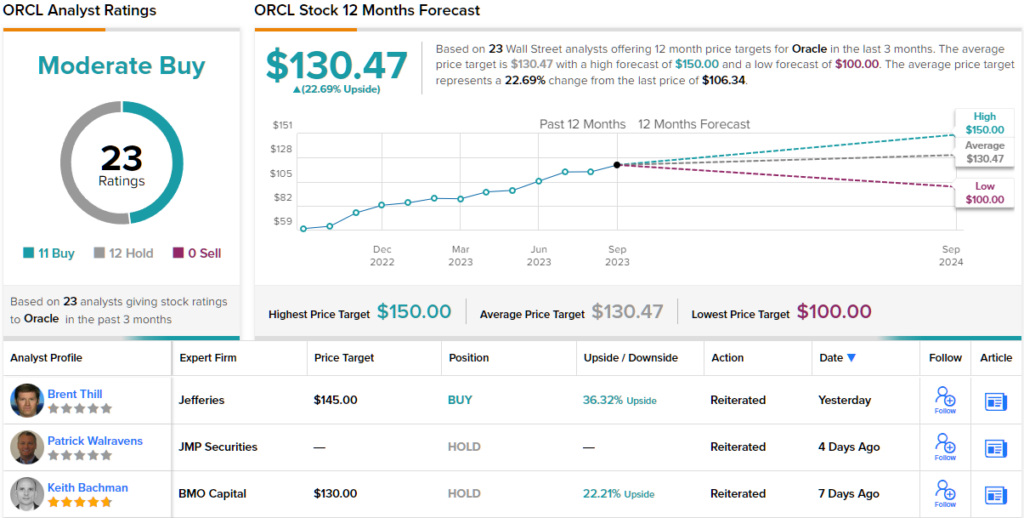

These comments underpin Bersey’s Buy rating on ORCAL, while his $144 price target makes room for 12-month returns of 35%. (To watch Bersey’s track record, click here)

A look at the consensus breakdown reveals there is a fairly even amount of Oracle bulls and fence-sitters on Wall Street. The stock’s Moderate Buy consensus rating is based on 11 Buys and 12 Holds. Going by the $130.47 average target, a year from now, shares will be changing hands for~23% premium. (See Oracle stock forecast)

Lam Research (LRCX)

For our next Fisher-endorsed stock, we’ll check out another industry giant. Lam Research is a leading global supplier of semiconductor manufacturing equipment and services, providing advanced solutions for the fabrication of integrated circuits.

The company specializes in the development and production of wafer fabrication equipment, including deposition, etch, and clean process systems, critical in the making of cutting-edge semiconductor devices. Lam Research’s tech and expertise enable semiconductor manufacturers to produce smaller, more powerful, and energy-efficient chips, thereby contributing to the advancement of electronic devices such as smartphones, data servers, and various other consumer and industrial applications.

The semiconductor industry is known to be heavily cyclical, and despite figures dropping sharply compared to the same period a year ago, Lam exceeded expectations in its fiscal fourth quarter of 2023 report (June quarter). Revenue fell by 30.8% from the same period a year ago to $3.21 billion, yet the figure trumped consensus expectations by $60 million. Adj. EPS declined from last year’s $8.83 to $5.98, yet that figure beat the forecast by $0.85. Moving forward, the company anticipates first-quarter revenue will hit the range between $3.1 to $3.7 billion, higher at the mid-point than the Street’s $3.28 billion estimate.

Fisher also has a big position here. He currently owns 2,813,207 LAM shares, which command a market value of $1.79 billion.

Wolfe analyst Chris Caso is the Street’s most prominent Lam Research bull, and he believes the company’s earnings are set to meaningfully improve once the cycle turns again in its favor.

“Lam has the most exposure to memory in our SCE (semiconductor capital equipment) coverage and memory spending has remained suppressed YTD. We believe that’s created a wide gap between Lam’s true earnings power and cyclically depressed CY23 numbers,” the 5-star analyst explained. “We see LRCX getting back to ~$36 in annual EPS by FY25 (about inline with consensus) on only $5.2bn memory spending (vs. $6.8bn peak, $4.6bn FY23). We think that still leaves room for estimates to move higher as memory spending eventually normalizes. We see line of sight to ~$40 EPS in CY25 with LAM trading at just 16.5x that EPS power.”

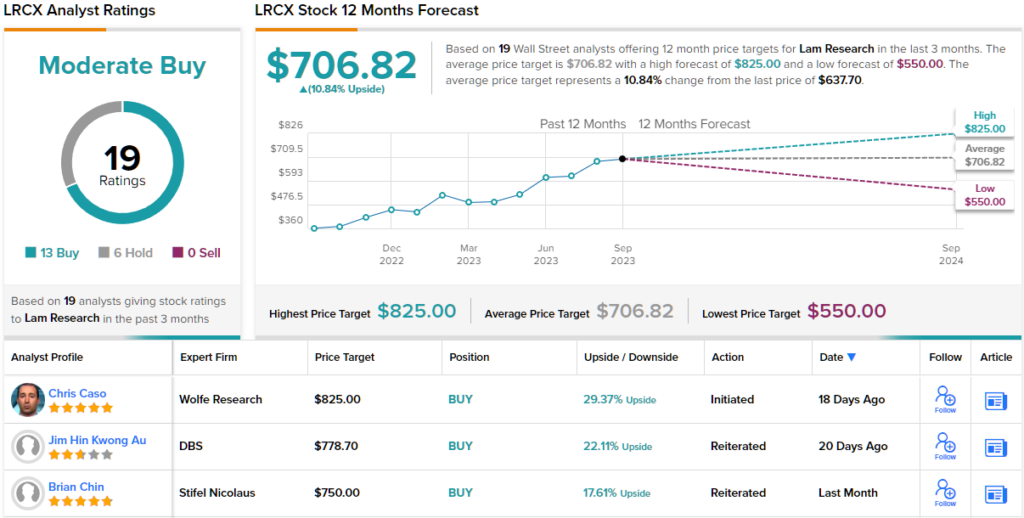

Along with an Outperform (i.e., Buy) rating, Caso’s Street-high $825 price target implies LRCX shares are set for growth of 29% over the coming months. (To watch Caso’s track record, click here)

Overall, LRCX stock has picked up a Moderate Buy rating from the Wall Street analyst consensus, based on 19 recent analyst reviews which include 13 Buys and 6 Holds. The shares are trading for $637.70 and the $706.82 average price target suggests a one-year upside of ~11%. (See LRCX stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.