Domino’s Pizza stock (NYSE:DPZ) continues to trade notably lower from its past highs, with investors expressing concerns that the company’s growth momentum may have reached a plateau. Despite major market indices rebounding significantly, shares of the world’s largest pizza franchisor currently trade 30% lower than their December 2021 peak of ~$550. Nevertheless, I believe current concerns are exaggerated, and Domino’s remains a high-quality company. Therefore, I am bullish on the stock.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Declining Revenues Due to Changing Consumer Dynamics

Concerns about the end of Domino Pizza’s growth story arise from recent declines in the company’s revenues, which can be attributed to shifting consumer dynamics. In recent years, consumers have strategically tailored their menu preferences to maximize savings with each transaction in the wake of persistent inflationary pressures. This has translated into a heavy headwind to the company’s growth prospects.

The root cause lies in the escalating prices of food ingredients, experiencing a notable surge in recent years, leading to increased sourcing costs. It’s crucial to note that nearly all (99%) of Domino’s 20,205 locations are franchised. This means that the majority of the company’s revenues are derived from Domino’s own supply chain, which is responsible for providing all franchises with the necessary ingredients.

Consequently, franchisees had to adjust menu prices upwards to offset these elevated costs. Today, a large pizza starts at $17.99, and we all know they are not that large anyway. Personally, I couldn’t help but feel that I had overpaid when I recently ordered a large Memphis BBQ Chicken pizza. It seems evident that many consumers share this sentiment, as Domino’s has encountered resistance to its price hikes. People seek value for their money across all “fast-food” chains, and Domino’s is no exception.

However, it’s essential to recognize that steep price increases are not unique to Domino’s Pizza. All fast-food and budget-friendly chains encountered price increases. I mean, a Big Mac combo meal can cost $17.59 these days. Even the option of cooking at home offered little relief as grocery prices also soared. Consequently, although the demand for Domino’s pizzas did not experience a significant decline, consumers have been really careful with their menu selections in an effort to save money.

As an illustration, opting for the daily discounted pizza has increasingly become a favored choice for many, reducing the average order value for Domino’s. Evidently, the average basket pricing to stores decreased by 1.7% in the company’s most recent Q3 results, which, coupled with slightly lower sales volumes, contributed to a revenue decline of 3.9% to $1.03 billion.

Note that this result represents the company’s worst top-line year-over-year result since the equivalent period of 2009 during the Great Financial Crisis when revenues had fallen by 6.5%. Thus, you can see why investors have become increasingly skeptical regarding the sustainability of Domino’s growth story. The company appears to be falling short of replicating the double-digit growth it used to have in the previous decade.

Domino’s Remains a High-Quality, High-Margin Company, Nonetheless

While Domino’s revenue growth has faced a noticeable dip, I am confident in the inherent quality of the company. It deserves increased attention from investors, especially for its robust, high-margin business model. As I mentioned, 99% of the company’s restaurants are franchised, insulating the company from many of the underlying concerns investors have.

To start off, although the company experienced a 4.3% decline in supply chain revenues in Q3 (attributed to lower sales volumes), the noteworthy aspect lies in Domino’s strategic opening of new locations. This expansion contributed to the expansion of its franchise network, with each location generating a substantial 5% royalty on the top-line sales. Consequently, excluding foreign exchange impacts and the exit from the Russian market, royalty revenues experienced a commendable growth of 5.1%.

This is where the company truly thrives, as royalty cash flows essentially translate to a 100% net margin. In contrast, the supply chain segment operates on razor-thin gross margins, hovering around 10%. Hence, the decline in supply chain revenues becomes less concerning when combined with an equivalent surge in royalty revenues, which holds the potential for a more significant impact on Domino’s profits.

In fact, despite the overarching decline in revenues, Domino’s exhibited an increase of 7.3% in operating income, which reached $189.4 million. I believe that it is pivotal for investors to direct their attention to this key metric alongside the robust growth in earnings per share, which soared by nearly 50% to $4.18. This notable earnings expansion during a challenging trading environment should take precedence over potential transient setbacks in the company’s top-line figures.

Is DPZ Stock a Buy, According to Analysts?

Regarding Wall Street’s sentiment, Domino’s Pizza features a Moderate Buy consensus rating based on 13 Buys, nine Holds, and two Sells assigned in the past three months. At $411.32, the average Domino’s Pizza price target implies 4.8% upside potential.

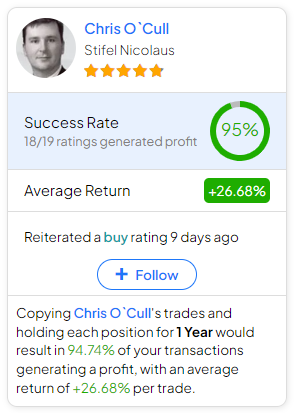

If you’re looking for the right analyst to guide your decisions in buying and selling DPZ stock, look no further than Chris O’Cull, who represents Stifel Nicolaus. Over the past year, he has consistently demonstrated exceptional performance, boasting an impressive average return of 26.68% per rating with a success rate of 95%. Click on the image below to learn more.

The Takeaway

In conclusion, while Domino’s Pizza has faced challenges in revenue growth due to changing consumer dynamics and rising costs, the company remains a high-quality, high-margin investment. The recent decline in revenues was offset by commendable growth in operating income and earnings per share.

Therefore, despite short-term concerns regarding the viability of the company’s growth story, Domino’s potential for sustained earnings growth forms a compelling investment case, given that the stock continues to trade far from its past highs.