Do you recall how online shopping evolved during the pandemic? For those of us with non-critical jobs, staying the majority of the time inside our homes meant requiring goods to be delivered to our doorstep. Suddenly, everyone and their mother ran an e-shop, and that’s why Shopify (NYSE: SHOP) was one of the biggest beneficiaries at the time. The pandemic has largely faded nowadays, and while many had expected Shopify’s performance to relax from its record, pandemic-driven results, the company has grown further. Yet, despite its solid growth, Shopify’s lack of profitability fails to inspire investors.

Even though the stock has lost more than 70% of its value year-to-date, I still find it quite hard to justify buying Shopify given its continued losses – especially during the current macroeconomic setup. Accordingly, I am neutral on the stock.

Robust Execution is Driving Revenues Higher

As I mentioned, what is impressive about Shopify’s performance is that the company continues to grow beyond its pandemic-driven numbers, even as COVID-19 has mostly evaporated. Its most recent Q3 results demonstrated that, steered by solid execution.

Total revenues rose to nearly $1.4 billion, a year-over-year increase of 22%. That’s a relatively massive increase considering that, if anything, results should have relaxed from last year’s record numbers with the pandemic fading. For context, on a three-year basis, Shopify’s revenue compound annual growth rate stands at 52%.

Another point that demonstrates how strong Shopify’s growth has been that many investors overlook is that the dollar has strengthened significantly over this period. Thus, the company keeps advancing forward despite potent headwinds.

Management deserves some credit here, as they have been focusing on all the key areas needed to drive these results. These include achieving improved Gross Merchandise Value penetration in Shopify Payments, enhancing Shopify Capital and Shopify markets, reducing barriers that help merchants go global, and sealing strategic partnerships, including the acquisition of Deliverr.

However, is Shopify’s compelling revenue growth enough?

Revenue Growth Means Little if Shopify Keeps Losing Money

Sure, Shopify’s growth continues to be stimulating, all things considered. However, the lack of sustainable profits keeps disappointing. After subtracting a massive $1 billion in operating expenses from Q3’s gross profit of $662.3 million and adding back $188 million from Shopify’s other investments, the net loss came in at a dreadful $158.4 million.

If Shopify can’t post meaningful profits against growing revenues after somewhat maturing over the past few years, when will it? I am particularly unhappy with the fact that, despite management’s meaningful operating developments, they seem to be not concerned at all when it comes to the lack of profits.

How do we know this? Because stock-based compensation surged from $79.6 million to $147.7 million in Q3. That’s outrageous, given the current trading environment.

At the current rate that Shopify is losing money and diluting shareholders, its equity value is going down the drain by the day. Year-to-date, stock-based compensation has amounted to $407.4 million, and the company has lost $2.9 billion. No wonder the stock has plummeted even as revenues continue to advance higher.

Consider This Before Deciding to Buy Shopify

Due to the lack of net income and net income growth prospects, it’s hard to tell where it makes sense to buy Shopify. Yes, we could make future projections and apply various profit margin scenarios, but at the end of the day, these are all meaningless if the company keeps printing stock in bulk.

Before even considering buying Shopify, make sure the company can actually post real profits. I am not talking about the artificial “adjusted” profits it has occasionally published, but actual positive GAAP net income.

Otherwise, excessive dilution is likely to keep eating away at the equity value per share, and who wants to own a business whose equity value is on the decline, anyway?

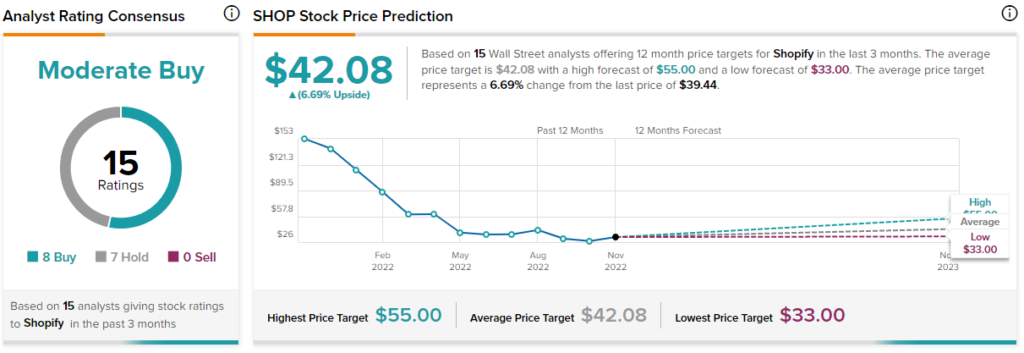

Is SHOP Stock a Buy or Sell, According to Analysts?

Turning to Wall Street, Shopify has a Moderate Buy consensus rating based on eight Buys and seven Holds assigned in the past three months. At $42.08, the average Shopify stock forecast implies 6.7% upside potential.

Who is Actually Right, Mr. Market or Wall Street Analysts?

Consensus estimates may be pointing to an upside north of 30%, but they have been bullish all this time that Shopify stock has been plummeting. So who is actually wrong? Are analysts wrong, being blindly optimistic about the stock, or is the market wrong, senselessly selling off a relatively good company? In my view, the market is largely right here. As I mentioned, it’s hard to justify being bullish on the stock when there is no light at the end of the tunnel when it comes to Shopify actually creating value for shareholders.

If management decides to take on some cost-cutting initiatives and stock-based compensation eases, Shopify’s margin expansion potential could transform its investment case for the better. Until then, however, I will be avoiding the stock. I could be missing something, but the risk here is just too high and certainly not my cup of tea.