One of the pandemic’s darlings, DocuSign, Inc. (DOCU), is scheduled to release its second quarter Fiscal 2023 results on September 8, after the market closes. DocuSign is facing several macro and micro issues, such as shifting consumer preferences post-pandemic, falling demand for products, and the absence of a CEO, all of which could impact the upcoming results.

DocuSign makes remote work easy by offering cloud-based electronic signature solutions. It also automates almost all documented business transactions.

The Street expects DocuSign to post an adjusted profit of $0.42 per share in Q2, lower than its comparative prior year period’s figure of $0.47 per share. Meanwhile, revenue is pegged at $602.25 million, representing year-over-year growth of 17.7%, and a modest 2.3% jump over Q1FY23 revenue of $588.69 million.

On the other hand, DocuSign had guided Q2 revenue to fall between $600-$604 million. Also, full-year Fiscal 2023 revenue is projected between $2.470 billion to $2.482 billion.

Macro & Micro Issues

Notably, DOCU stock has lost a whopping 65.7% so far this year vis-à-vis gaining a massive 101% between the start of 2020 and the end of 2021. During the pandemic, corporations relied on DocuSign and rival Adobe’s (ADBE) products to complete transactions online. However, as the pandemic faded, the demand for DocuSign’s products dimmed.

Also, the massive growth registered in the previous year is making comps difficult. Further, the abrupt exit of CEO Dan Springer has left the company searching for a suitable head.

Moreover, the TipRanks Website Traffic tool shows that in Q2, the global estimated visits to docusign.com decreased 5.3% compared to Q1FY23. The estimated visits fell 8.03% in Q2 compared to the same period last year.

What Do Analysts Expect from DocuSign?

Needham analyst Scott Berg expects DocuSign to report in-line Q2 results. The analyst has a Hold rating on DOCU stock. Berg believes an update on the vacant position of CEO will be much awaited on the conference call.

As per Berg, the company’s current challenges include “slowing business, rep turnover, new sales leader, and most recently, the announced departure of CEO Dan Springer.” Also, the company has set a very low bar of 1% billings growth. All these indicate an in-line Q2 performance.

On the contrary, analyst Patrick Walravens of JMP Securities remains optimistic about DocuSign despite the odds. Although he slashed the price target on DOCU to $84 (56.1% upside potential) from $151, he still maintains a Buy rating on the stock.

Walravens conducted some due diligence on DocuSign and collected 13 data points; five positive and eight negative. The positives mostly included good feedback on the products, an expansion opportunity at a Fortune 500 financial services company, and a large private company selecting DOCU for all its contract lifecycle management (CLM) requirements because of its tie-up with Salesforce (CRM).

On the other hand, the negatives mostly include a caution about the sales targets being too high or unrealistic. Based on the data points and the difficult macroeconomic backdrop, Walravens has reduced the model estimates up to Fiscal 2025. Interestingly, Walravens also believes DocuSign may be a potential takeover candidate.

What is the Target Price for DocuSign?

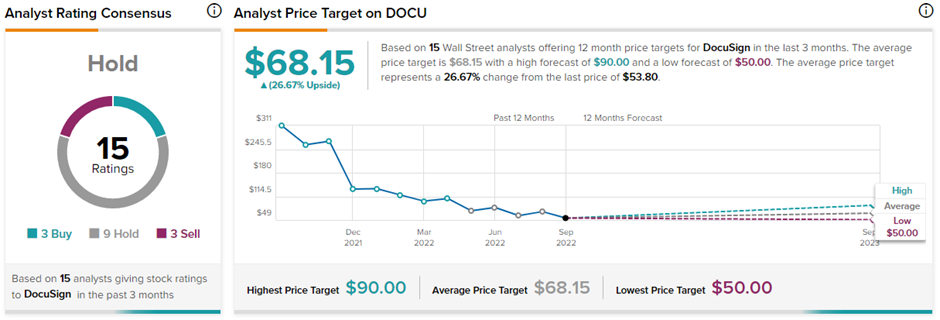

On TipRanks, DOCU stock has a Hold consensus rating. This is based on three Buys, nine Holds, and three Sells. The average DocuSign price target of $68.15 implies 26.7% upside potential to current levels.

Ending Thoughts

DocuSign is certainly facing one of the toughest times to prove its existence. The shifting consumer trends post-pandemic have reduced demand for its products. Nonetheless, several companies used DocuSign’s products even before the pandemic and will continue to do so even post-pandemic. DocuSign must continue to target the right customers to bolster its sales.