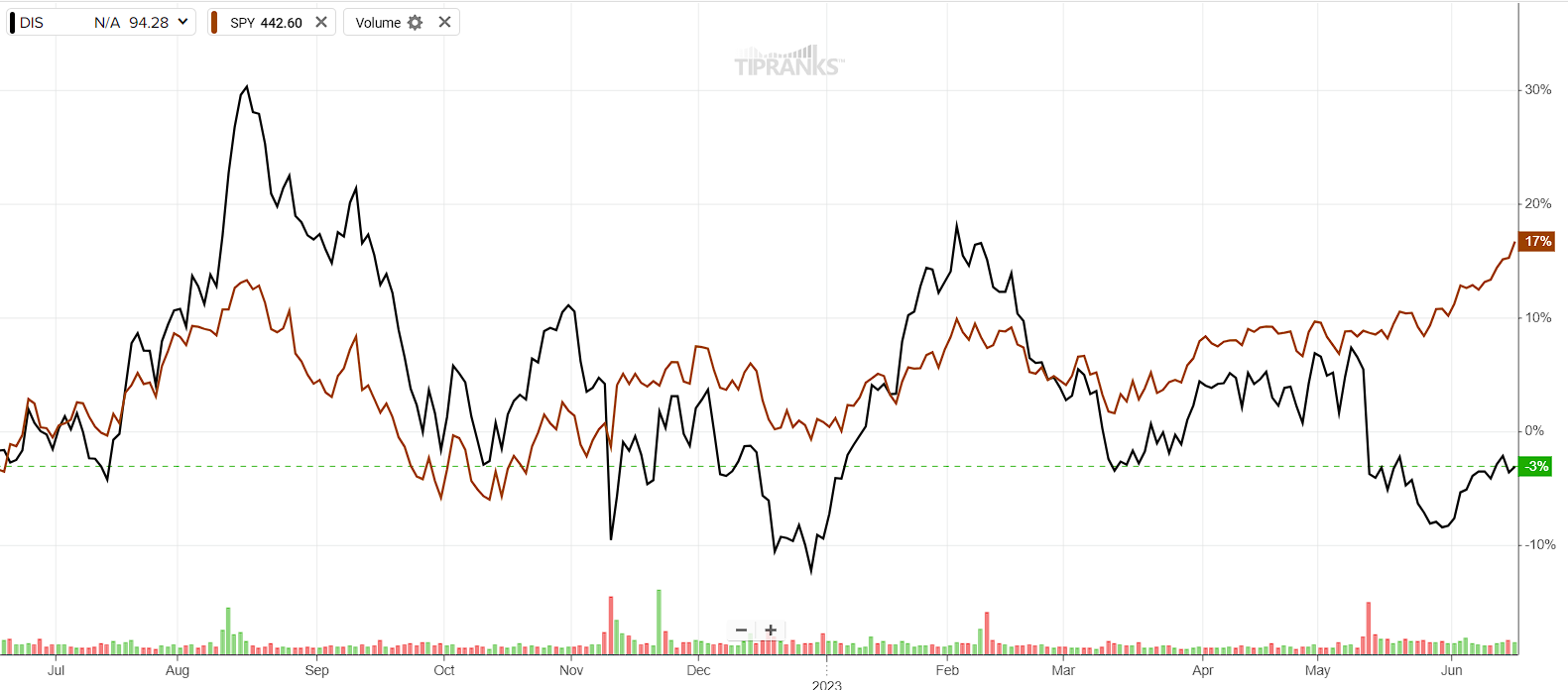

The Walt Disney Company (NYSE:DIS) stock’s performance hasn’t been very magical for quite some time now. The multinational media behemoth has struggled to find solid ground in the post-COVID media landscape, resulting in significant underperformance compared to the overall market. In contrast, shares of the SPDR S&P 500 ETF Trust (NYSEARCA:SPY), a leading ETF that tracks the S&P 500 Index (SPX), have experienced a notable 17% increase over the past year.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

Meanwhile, Disney stock has declined by approximately 3%. Remarkably, Disney’s stock is currently stagnant at levels last seen in the summer of 2014, despite the company’s extensive efforts to achieve various breakthroughs across all aspects of its business.

In my view, investor sentiment in Disney stock is likely to remain muted as the company’s results continue to disappoint. Its legacy media segments struggle, the streaming business has a hard time scaling, and while its parks deliver strong numbers, it’s only due to aggressive pricing, which can only last so long. Therefore, I don’t see Disney offering any meaningful upside and remain neutral on the stock.

Legacy Media is Slowly Dying

Disney’s legacy media division, which basically comprises its Linear Networks businesses, such as ESPN, Disney Channel, ABC, National Geographic, etc., has historically been the backbone of the company’s profitability. However, the declining demand for traditional media networks has been brutal for the industry, and Disney is not an exception.

Specifically, in its Q2 results for Fiscal 2023, Linear Networks revenues fell by 7% to $6.6 billion, while the segment’s operating income plummeted by 35% to $1.8 billion. In fact, both the domestic and international divisions underperformed.

On the Domestic Channels side, revenues fell by 4% as both cable and broadcasting struggled from a decline in subscribers and lower ad revenues. On the International Channels side, revenues also fell by a substantial 18% due to decreases in average viewership at Disney’s sports and non-sports channels.

So, while Disney’s legacy media remains quite profitable, still managing to post an operating income margin of about 27%, its long-term deterioration trend shouldn’t pause anytime soon. Consumers have been migrating from traditional networks to more dynamic channels for quite some time, which should keep translating to Disney’s legacy media’s slow death over time.

Parks Post Strong Results, but Higher Pricing Could Backfire

Disney’s Parks, Experiences, and Products division has been the more cheerful part of Disney’s recent reports, and this was once again demonstrated in its second-quarter report. Revenues for the quarter rose 17% to $7.8 billion, while the segment’s operating income rose 23% to $2.2 billion.

Higher results were driven by growth at Shanghai Disney Resort, Disneyland Paris, and Hong Kong Disneyland Resort. In turn, this was driven by higher volumes and guest spending growth in parks, which is another way for the company to attribute this growth to higher average ticket prices, average daily hotel room rates, and food.

In my view, such growth from this division is not sustainable over the long term. The company has been able to raise prices strongly lately and blame it on inflation, but with inflation easing and the likelihood of consumers getting tired of Disney’s aggressive pricing, we could see this strategy eventually backfire.

Streaming Suffers from Industry Saturation

Finally, Disney’s streaming division has also been a source of disappointment lately, as industry saturation has made it hard for the company to scale its platforms. With Amazon’s Prime Video, Netflix, HBO Max, and several other competitors fighting for consumers’ attention, scaling viewership beyond this makes for a significant challenge.

While Disney’s Direct-to-Consumer (DTC) revenues for the quarter rose by 12% to $5.5 billion due to a 20% increase in domestic (U.S. & Canada) average revenue per user (ARPU), the company once again lost money, posting an operating loss of $0.2 billion. In fact, higher pricing combined with brutal competition in the industry resulted in Disney+ subscribers declining by 2% to 157.8 million. That’s a terrible result, suggesting that Disney’s subscriber base has already reached a plateau.

Even Netflix, which is a much more mature platform, continues to grow its subscriber count. With investors seeing the limited growth beyond increased pricing and ongoing operating losses, which can only be reversed by achieving scale through subscriber growth (which the company lacks), it becomes evident how even Disney’s relatively more dynamic and growth-focused division becomes a cause for skepticism within the market.

Is DIS Stock a Buy, According to Analysts?

Turning to Wall Street, Walt Disney somehow features a Strong Buy consensus rating based on 13 Buys and four Holds assigned in the past three months, despite the stock’s struggle to advance higher. At $122.69, the average Disney stock price prediction suggests 34% upside potential.

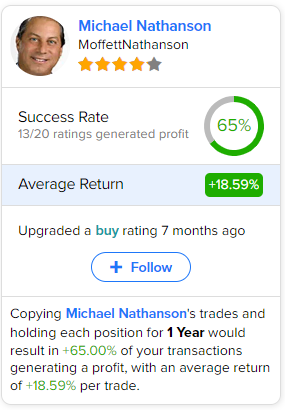

If you’re wondering which analyst you should follow if you want to buy and sell DIS stock, the most profitable analyst covering the stock (on a one-year timeframe) is Michael Nathanson from MoffettNathanson, with an average return of 18.59% per rating and a 65% success rate.

The Takeaway

Overall, Disney’s stock performance has been disappointing for a long time, reflecting the challenges it faces in the evolving post-COVID media landscape. The company’s traditional media division is grappling with the decline in demand for linear networks, resulting in decreased revenues and viewership.

While the Parks, Experiences, and Products division has delivered positive results, the sustainability of its growth through aggressive pricing is questionable in the long run. Moreover, its streaming business is contending with industry saturation, hindering its ability to expand its platforms and leading to a decline in subscriber numbers. Considering these factors, investor sentiment toward Walt Disney stock is likely to remain subdued, with limited prospects for significant growth.