DigitalOcean (NYSE:DOCN), a leading American cloud provider helping start-ups and small and medium-sized businesses (SMBs) scale cloud-stored data, is capitalizing on the AI revolution in cloud computing. DOCN is a growth-focused opportunity that is still trading below its Q2 peak while making waves in the increasingly demanding AI and machine learning (ML) arenas. Strategic initiatives, impressive earnings, and an imminent leadership change present a bullish growth opportunity I wouldn’t want to miss.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Why is DOCN Poised for Growth?

DigitalOcean has been riding the AI wave following its acquisition of Paperspace, which provides cloud infrastructure for graphic processing units (GPUs) — a key component for Cloud Hosting. The acquisition closed in Q3 but has seen Paperspace customers migrating through November, with full integration expected by December 1.

The company is poised for growth, doubling down on the new trend of cloud hosting. In October, it introduced a cloud-hosted scalable storage for managed databases, further addressing the growing demand for AI and ML. This strategic initiative enables businesses to scale up to 15TB storage capacity efficiently, meeting the data-intensive requirements of AI/ML applications. DOCN’s move caters to a key demographic increasingly adopting AI/ML technologies: start-ups and SMBs.

How do DOCN’s Financials Look?

In Q3, DigitalOcean continued its upward trajectory, reporting revenue of $177 million, a year-over-year increase of 16%. The company’s annual run-rate revenue (ARR) also grew by 11% year-over-year, reaching a significant $713 million compared to $682 million in Q2. The improved financial performance reflects strong demand for DigitalOcean’s services, driving the company’s profits, with non-GAAP EPS nearly doubling on a trailing-nine-month basis to $1.16 per share.

The company last reported quarterly adjusted earnings of $0.44 per share, giving the stock a price-to-earnings (P/E) of 20.1, well below the sector average of 43.7. Adjusted EBITDA also grew apace at $76 million versus $72 million in Q3, with the EBITDA margin at 43% compared to 40% last year. DOCN also provided guidance suggesting stronger growth in Q4. The company anticipates its Q4 adjusted earnings to moderate to $0.36-0.37 per share, a significant improvement over last year’s $0.28.

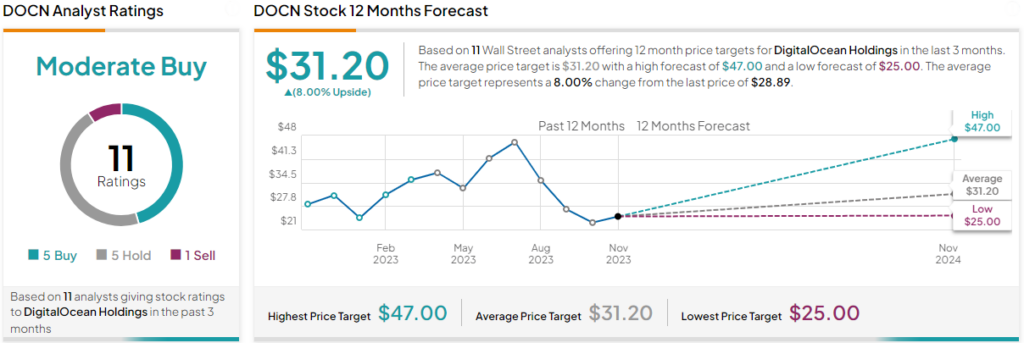

Is DOCN Stock a Buy, According to Analysts?

The optimistic outlook is supported by several Wall Street analysts who have either maintained their ratings or upgraded their price targets for DOCN. Based on the 12-month price targets given in the past three months, the average DOCN stock price target represents 8% upside potential.

Both Oppenheimer and Goldman Sachs have also upgraded their ratings recently. Oppenheimer has shifted its rating from Perform (Hold) to Outperform (Buy), citing strong AI demand. Meanwhile, Goldman Sachs (NYSE:GS) has reversed its rating from Sell to Buy, citing changes to cyclical risks and structural improvements in the company. Both expect improved revenue growth and view DOCN as a promising growth opportunity.

Is Now a Good Time to Buy DOCN?

In addition to capitalizing on the new cloud hosting trend, DOCN has fallen by 15.9% in the past six months. While this might seem alarming initially, the stock is still a decent investment opportunity since it has dropped by over 40% since its July peak of $51.67, primarily for administrative reasons.

Shares fell after it reported a discrepancy in its earnings, but it was an overstatement of its tax liability. Today, it trades almost 50% higher from its November 1 low of $19.39 per share, at $28.89, leaving about 79% upside potential to July’s top.

In August, the company announced the replacement of its CEO, Yancey Spruill, following the discrepancies in past reporting. This news unsettled investors, leading to a significant drop in DOCN’s share price. Investors were also wary due to the CEO selling his shares. However, the sale occurred after the company’s solid earnings report on November 2 boosted the stock, suggesting Spruill was likely capitalizing on the move before advancing his career elsewhere.

Appointing a new CEO could restore market confidence in the company’s administrative functionality, driving the share price back to valuations seen before the reporting mishaps.

DOCN: A Promising Growth Opportunity

DigitalOcean’s focus on scalable solutions for data-intensive applications positions the company well to capitalize on the growing demand for AI and ML technologies. Combined with its impressive financial performance and an imminent leadership change, DOCN presents a promising growth opportunity for investors. The company’s focus on scaling start-ups and SMBs positions it favorably to capitalize on future market trends.