Shipping companies might not dominate the headlines, but some are quietly delivering impressive returns for investors. The dry bulk sector, in particular, stands out. These shippers specialize in transporting unpackaged, bulk cargo like iron ore, coal, steel products, and grains – think of them as floating silos.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Despite flying under the radar, their role in the global economy is crucial. They transport the raw materials that drive key industries, and many of these companies also offer attractive dividends. For investors, this combination makes them strong candidates for long-term portfolio growth.

And, the dry bulk segment appears to be entering a cyclical upswing. A measure of charter rates for industry’s workhorse Capesize ships has more than tripled year-over-year, rising from $9,000 per day to $28,000 per day – and the companies are returning some of that lucre to shareholders, mainly in the form of high-yield dividends.

This action has caught the attention of Deutsche Bank analyst Chris Robertson, who has initiated coverage of two dry bulk shippers with particularly notable dividend yields – up to 13.5% in one case. Robertson focuses on these two strong dividend payers, and his comments, along with the general share data gathered on the TipRanks platform, are worth a closer look.

Star Bulk Carriers (SBLK)

The first stock we’ll look at here is Star Bulk Carriers, a global shipping company that moves both the ‘major bulks’ and the ‘minor bulks.’ The first category includes such items as iron ore, minerals, and grains, while the second category includes items that are still important but in less demand, such as fertilizers, steel products, and bauxite. Star Bulk has a market cap of $2.4 billion, and at the end of last year completed an acquisition transaction with a major competitor, Eagle Bulk. That transaction, conducted in stock and worth $2.1 billion, allowed Star Bulk to consolidate its business and to become the largest dry bulk shipper traded on the NASDAQ index.

The company’s size is clear – Star Bulk operates a fleet of 161 bulk carriers, ranging in size from the relatively small (~53,000 DWT) Supramax carriers to the giant (~210,000 DWT) Newcastlemax bulkers. These vessels have an average age of just over 11 years, and the company’s ship management operations cover both commercial and technical aspects of maintenance and ops on the global dry bulk carriage trade. In an interesting note, Star Bulk earlier this month announced the sale of its oldest ship, a Capesize carrier, for a gross price of $20 million. The company expects net proceeds from the sale of $13 million, and a net gain on the vessel of $7.7 million to be recorded during 3Q24.

On the financial side of its operations, Star Bulk reported 2Q24 revenues of $352.8 million. This was up an impressive 47.8% from the prior-year period, and beat the forecast by $82.88 million. The company’s earnings, reported as an EPS of $0.78 by non-GAAP measures, missed the forecast by a nickel – but it was up significantly from the 47-cent EPS reported in 2Q23.

The company also generated substantially more cash than it did in 2Q23. For 2Q24, Star Bulk’s net cash from operations came to $142.6 million, a marked improvement over the $96.9 million in the last quarter of 2023.

Star Bulk’s recent dividend history goes back to 2021, when the company resumed payments post-COVID. In that time, the company has adjusted the dividend as needed to keep it in line with earnings. The last declaration, in the 2Q24 report, was for a payment of 70 cents per common share that was paid out on September 6. At the annualized rate of $2.80 per common share, the dividend gives a forward yield of nearly 13.5%. We should note here that, since June of 2021, the company has paid out $1.25 billion in dividends to shareholders.

Looking at this dry bulk carrier, Deutsche Bank’s Chris Robertson is impressed by the firm’s cash generation and its strong dividend, as well as its ability to grow through acquisition. He writes, “Star Bulk has one of the strongest balance sheets of any public shipping company and its dividend policy is a sector-leading example of prudent capital management which rewards shareholders across the cycle in the form of quarterly cash dividends or via sustainable and accretive fleet growth… The Company has a long history of making transformative deals using its shares as currency and we expect Star Bulk will remain an active participant in the M&A market going forward as a market consolidator.”

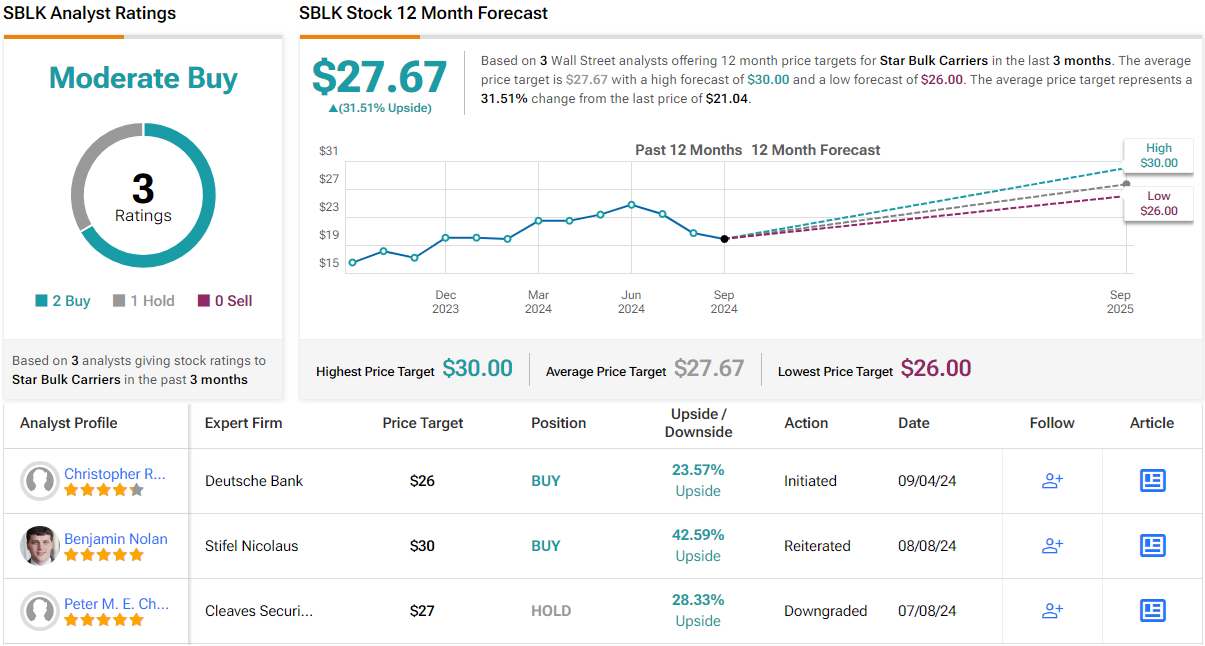

To this end, Robertson gives SBLK shares a Buy rating to kick off his coverage, with a $26 price target that implies a one-year upside potential of 23.5%. Based on the current dividend yield and the expected price appreciation, the stock has ~37% potential total return profile. (To watch Robertson’s track record, click here)

Overall, SBLK has a Moderate Buy consensus rating from the Street, based on 3 reviews that include 2 to Buy and 1 to Hold. The shares are priced at $21.04 and their $27.67 average price target is slightly more bullish than the Jefferies view, suggesting a gain of 31.5% in the next 12 months. (See SBLK stock forecast)

Genco Shipping (GNK)

The second dividend stock on our list today is Genco, another of the major players in the dry bulk shipping sector. Genco takes what it calls a ‘barbell’ approach to fleet composition and has put together a shipping fleet of 42 vessels, including 16 of the big Capesize carriers (bulk carriers ranging in size from 175,000 to 181,000 DWT) with the rest being smaller Supramax and Ultramax carriers (vessels approximately one-third of the dry weight tonnage of the Capesize class).

This fleet composition allows the company to transport major bulk cargoes on the larger ships, while carrying minor cargoes on the smaller vessels. It’s a strategy built around maximum flexibility, allowing Genco to benefit from both the large fees of the Capesize ships and the steadier income stream from the smaller carriers – all while maintaining a worldwide presence in the global shipping lanes.

All of this makes Genco one of the industry’s most efficient dry bulk carriers. Its fleet is modern and fuel efficient, and the company has built a reputation for meeting the highest standards of operational safety. Genco, with a market cap of $737 million, is the largest US-headquartered dry bulk shipper, and brings nearly 20 years’ experience to the shipping business. The company’s vessels make over 1,000 port calls every year.

Genco’s operations brought solid performance in its last reported quarter, 2Q24. The company’s top line, the voyage revenues, came to $107 million and beat the forecast by over $32 million while growing more than 18% year-over-year. The bottom line earnings were reported as a non-GAAP EPS of 46 cents, which was 2 cents per share ahead of expectations.

Through the full first half of 2024, Genco generated $61.3 million in net cash from operating activities, a figure that was up more than 57% year-over-year. As of June 30 this year, the company had more than $42 million in cash and other liquid assets on hand.

Turning to the dividend, we should note that Genco, on September 10, announced a new dividend calculation formula that will allow the company to pay out a higher proportion of its available cash as dividends. This new formula will be applied going forward, starting with the third quarter of this year. In the meantime, the last dividend declared was paid out on August 26, at a rate of 34 cents per common share. The annualized payment of $1.36 per share gives a forward yield of 7.9%.

Analyst Chris Robertson, in his write-up of Genco for Deutsche Bank, likes the company’s balance sheet and its available liquidity, seeing both as favorable for the long term.

“The Company has one of the strongest balance sheets in the industry, with an estimated net-loan-to-value of ~5%. It ended the most recent quarter with $42.3 MM in cash on the balance sheet and has access to liquidity of another ~$330 MM under its revolving credit facility. To note, the Company has reduced its outstanding debt by 78% since implementing its new value strategy in 2021. We believe the Company will continue to pay down debt until it reaches net-debt-zero,” Robertson opined.

It’s no surprise that Robertson follows these comments with a Buy rating on GNK, and his $22 price target shows his confidence in a 24% gain in the year ahead.

Overall, Genco’s Strong Buy analyst consensus rating is unanimous, based on 3 recent positive reviews. The shares are currently trading for $17.72 and have an average price target of $25, a combination that implies the stock will appreciate by 41% on the one-year horizon. (See GNK stock forecast)

To find good ideas for dividend stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.