The most recent set of economic data paints a confusing picture. The jobs market remains strong, inflation remains stubbornly high, and the Fed is likely to stick to its guns on interest rates. But Goldman Sachs CEO David Solomon has made some recent comments that should help clarify the picture.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

We should expect that economic growth will be more sluggish in 2023, according to Solomon. In his view, China’s ongoing reopening will catalyze growth – but also bring additional inflationary pressures. Inflation itself will remain ‘sticky,’ reinforcing the Fed’s rate-hike policy. But Solomon is less worried about the recessionary risks, believing that we’re in for an easier let-down going forward.

Of the chance that we’ll avoid a recession, Solomon said, “The consensus has shifted to be a little bit more dovish in the CEO community that we can navigate through this with a softer economic landing. The chance of a softer landing feels better than it did six to nine months ago.”

A softer landing means less risk – and that should open up opportunities that investors might not otherwise see. The stock analysts at Goldman Sachs have made it easier to find these opportunities. They have pinpointed two equites that they believe are primed for further growth. Using the TipRanks database, we can get idea what the rest of the Street thinks lies in store for these stocks. Let’s take a closer look.

Monday.com (MNDY)

We’ll start with Monday.com, a work management software firm that went public a little more than a year and half ago. The company’s product line is available by subscription through a cloud-based platform, and users can optimize their office systems, including CRM, marketing, project development, and sales operations. Monday.com’s products connect people, processes and systems in the service of a streamlined workflow, and its enterprise customer base includes big names such as Coca-Cola, Lionsgate, and Hulu.

A quick look at some macro numbers draws the outline of Monday’s story. The company has posted 6 consecutive quarters of sequential revenue gains since entering the public market, and currently boasts over 186,000 active customers, of whom more than 1,470 generate more than $50,000 each in annual recurring revenue.

Earlier this week, Monday reported its financial results for Q4 and full-year 2022, and the results were impressive. The quarterly top line reached $149.9 million, up 57% year-over-year, and full-year revenues, at $519 million, was up 68% y/y. The company ran a net loss, but that loss moderated somewhat in Q4, from $31.6 million in the year-ago quarter to $10.1 million in this report.

In addition to the top and bottom line success, Monday.com achieved positive cash flows for the second consecutive quarter, a fact that boosted the full-year numbers into positive territory. The Q4 cash from operations came to $34.1 million, and the free cash flow came to $29.7 million. These numbers compare favorably to the figures of $13.5 million and $10.1 million reported in 4Q21 – and accounted for more than the full-year total of $27.1 million in cash from operations and $8.1 million in free cash flow.

That forms the background for the comments by Goldman Sachs’ 5-star analyst, Kash Rangan, who says of this company: “Monday.com continues to be one of the few companies in software largely evading a pronounced impact from the weaker demand environment. While we acknowledge the surfacing of softer spending trends, we see management driving a healthy balance between net-new user additions, enterprise expansion, and operating income/FCF profitability.”

“Actions to move upmarket also create a longer-term tailwind as current investments in go-to market and platform enhancements (i.e., Monday DB, app marketplace) can scale over time, growing with existing users and potentially attracting new customers. Strong traction in recent productlaunches, such as CRM Sales which was able to increase thenumber of accounts by a healthy 13x on the platform since 1Q22 (to2,458), bolsters our conviction on this thesis,” Rangan added.

Going forward, Rangan puts a Buy rating on MNDY shares, along with a price target of $210 to suggest ~24% upside for the coming year. (To watch Rangan’s track record, click here)

Leading tech firms have no trouble getting analyst attention from the Street – and Monday.com has 15 recent analyst reviews, with a breakdown of 14 to 1 favoring the Buys over Holds for a Strong Buy consensus rating. (See MNDY stock forecast on TipRanks)

AppLovin Corporation (APP)

The second Goldman Sachs pick we’re looking at is AppLovin, another software platform – this one designed for mobile app developers. AppLovin provides tools for its target customer base, the legion of mobile app developers who have jumped into the app creation niche opened up by the proliferation of mobile smart devices in the last decade or more. AppLovin’s features include development optimization tools, as well as advertising, analysis, and publishing services.

AppLovin has been in business since 2012, and now boasts over 10,000 developers using the software. The company processes over 2.5 million requests per second through its platform, and processes more than 6 petabytes of data per day. In all, AppLovin has built itself an impressive footprint in the online developers’ world.

The company’s latest financial release, for 4Q22 as well as the full year, showed some mixed results. Quarterly revenues came in at $702 million, for an 11% year-over-year decline. At the bottom line, the company saw a quarterly net loss of $80 million, which compared unfavorably to the $31 million in net profit recorded in the year-ago quarter. On the bright side, the company issued strong first-quarter guidance. The company expects revenue to be within a range of $685-$705 million, beating the consensus estimate of $677.13 million.

AppLovin’s performance has caught the eye of Goldman’s 5-star analyst, Eric Sheridan, who believes APP is a great stock to buy for the long term.

“While we expect the short-term investor debates to stay focused on the volatility in the advertising/gaming end markets, we continue to look long-term at the collection of businesses under AppLovin as producing above average industry growth and a strong margin profile in a recovered mobile ads/mobile gaming landscape,” Sheridan opined.

Sheridan adds a Buy rating to these comments, and his price target of $23 indicates his confidence in an upside of 36% for the next 12 months. (To watch Sheridan’s track record, click here)

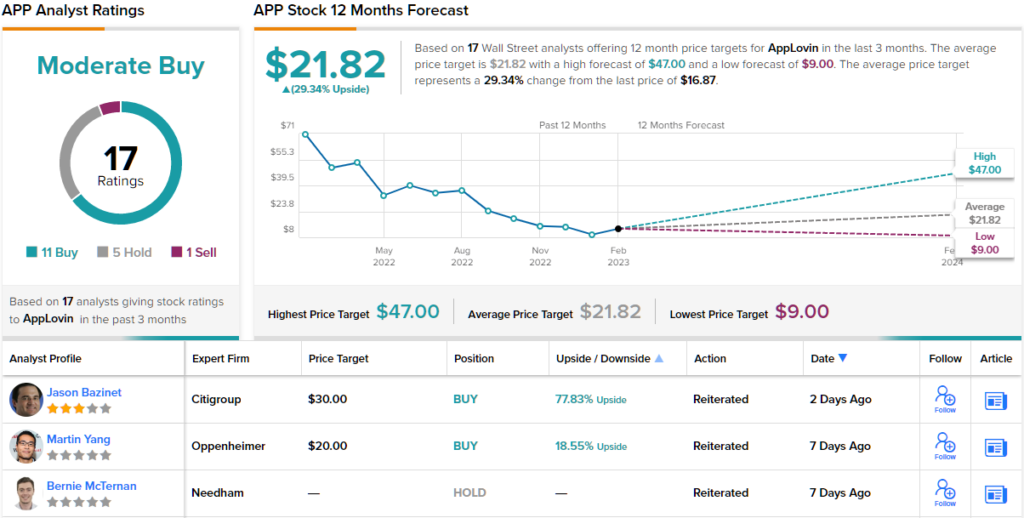

Overall, there are 17 recent analyst reviews on this stock, with a breakdown of 11 Buys, 5 Holds, and a single Sell, for a Moderate Buy consensus rating. (See AppLovin stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.