David Einhorn’s hedge fund, Greenlight Capital, enjoyed some big gains in 2022, being one of the few to benefit from last year’s bear market. The conditions suited the value investor’s style, and the fund had its best year in a decade. However, it has been a different story so far this year, as Greenlight has been underperforming the broad markets.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

Einhorn, however, is not about to bang his head against the wall and try to fit a square into a circle. In a recent letter to shareholders, he stated, “Many have commented that what worked in 2022 didn’t work in the beginning of 2023, and vice versa. That seems about right to us.”

While the economy is flashing conflicting signals – employment, wages, and household balance sheets look “quite strong” against concerns that tightening lending standards will “constrain the economy and create a substantial slowdown” – Einhorn remains receptive to whichever way the wind blows. “Our net long exposure is now back in line with its long-term average,” he stated. “We are equally open-minded to becoming even more net long or pivoting back to bearish as economic events unfold.”

In the meantime, Einhorn has been doubling down on the equities he believes will do well whatever the economic backdrop and among those are a pair of under-the-radar energy stocks. We ran these tickers through the TipRanks database to find out Wall Street’s stock experts’ view of them. Let’s check the results.

Gulfport Energy Corporation (GPOR)

The Energy sector was one of the few segments to shine in 2022, and while Einhorn is open to new ideas, it appears that he is still backing its chances. He has been loading up on shares of Gulfport Energy Corporation, an independent oil and natural gas exploration and production (E&P) firm based in Oklahoma City.

With operations primarily focused on the Appalachia and Anadarko basins, the company engages in the acquisition, development, and production of oil and gas reserves. Gulfport boasts a portfolio that includes both conventional and unconventional assets, with a particular emphasis on shale formations such as the Utica Shale in Ohio and the SCOOP play in Oklahoma.

The company adheres to a disciplined approach to capital allocation, prioritizing high-quality assets with favorable risk-reward profiles. It’s a strategy that helped Gulfport deliver a solid set of results in the most recently reported quarter – for 1Q23.

In the quarter, revenue rose by 5% year-over-year to $1.05 billion. The company exceeded expectations with a total production of 1,057.4 MMcfe (million cubic feet of gas equivalent) per day. Gulfport achieved $523.1 million of net income and $229.7 million of adjusted EBITDA, surpassing consensus estimates. Additionally, the company generated $63.1 million of adjusted free cash flow.

The market reacted well to the results, and most likely, Einhorn too. In Q1, he increased his GPOR stake by 126% with the purchase of 157,500 shares. He now holds a total of 283,000 shares, currently worth $28.26 million.

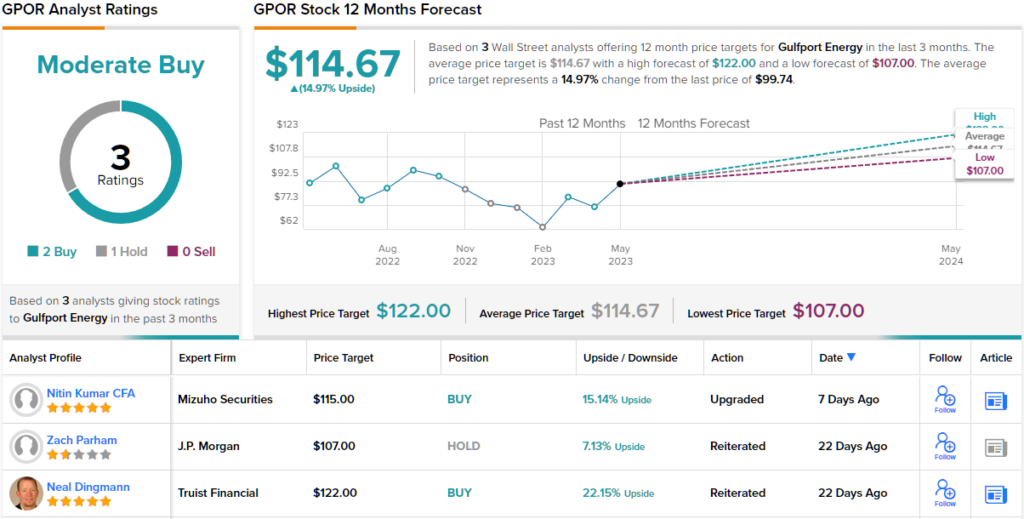

Truist 5-star analyst Neal Dingmann is also a fan and thinks the company has some differentiating attributes.

“Gulfport has a number of variables that set itself apart from most other small cap, gassy E&Ps resulting in continued, notable FCF generation despite weak natural gas prices. The company’s minimal/maintenance capital will drive production growth in a program that should see upside from operational efficiencies and lower OFS costs, all the while having nearly all production hedged this year and 60%+ next year at +$3/mcf. The low existing debt allows GPOR to distribute most FCF to shareholder return in the form of material share buybacks,” Dingmann opined.

Putting these thoughts into ratings and numbers, Dingmann considers GPOR a Buy while his $122 price target suggests shares will climb 22% higher over the coming months. (To watch Dingmann’s track record, click here)

Elsewhere on the Street, this under-the-radar name receives an additional 1 Buy and Hold, each, all coalescing to a Moderate Buy consensus rating. Going by the $114.67 average target, the shares have room for ~15% growth in the year ahead. (See GPOR stock forecast)

CONSOL Energy (CEIX)

The next Einhorn-endorsed name we’ll dig into is CONSOL Energy, a leading U.S. coal producer and exporter. With its active mining operations dating back to 1864, the company owns a diversified portfolio of coal assets, encompassing both underground and surface mining operations.

Its flagship operation is the Pennsylvania Mining Complex, which has the capacity to produce around 28.5 million tons of coal per year. The complex consists of three large-scale underground mines: Bailey Mine, Enlow Fork Mine, and Harvey Mine. Additionally, the company owns a full export terminal in Baltimore. In fact, given the anticipated drop in US coal consumption, CONSOL Energy has been shifting its focus overseas, making the export business increasingly important.

The company has also benefited from Russia’s war on Ukraine, as Europe has looked for alternative coal supplies rather than rely on Russia’s coal exports. The latest set of quarterly results show how CONSOL has been positively impacted.

Q1 GAAP net income reached $230.4 million compared to a $4.4 million loss displayed in the same period last year, while adjusted EBITDA climbed from $169.2 million a year ago to $346.3 million. On the top-line, revenues increased by 92.1% year-over-year to $688.6 million, while beating the Street’s forecast by almost $96 million.

Along with the quarterly results, CONSOL also announced its dividend distribution, set at $1.10 per common share. This represented 17% of the cash available for distribution. The $1.10 dividend annualizes to $4.40 per share and gives a high yield of 7.52%.

As for Einhorn, he must have been pleased with the results. In Q1, he bought 904,190 shares, upping his stake in the firm by 50%. In total, he now holds 2,716,741 shares, representing a current market value of $158.41 million.

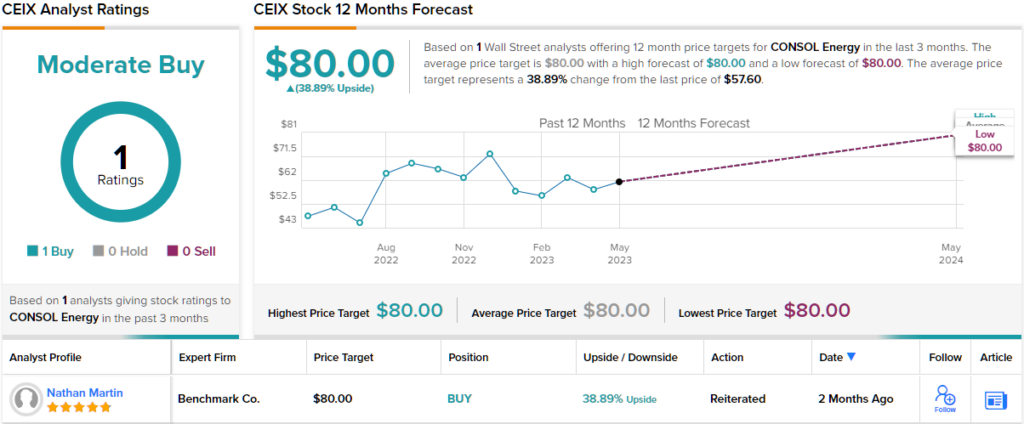

Einhorn is not the only bull on CONSOL. Nathan Martin, a 5-star analyst with Benchmark, is impressed with the company’s execution in recent months, writing, “CEIX is now near-fully contracted for 2023 and 60% committed and priced for 2024 based on our estimates, providing improved cash flow visibility. Moreover, it has nearly completed its debt reduction goals. As such, the company has increased its shareholder return program to 75% of FCF and raised its repurchase authorization to $1 billion as it expects to pivot to buybacks.”

These comments underpin Martin’s Buy rating while his $80 price target implies investors will be pocketing returns of ~39% a year from now. (To watch Martin’s track record, click here)

CEIX definitely fits the under-the-radar description. Martin is currently the sole analyst to have posted a review of the company’s prospects over the last 3 months. (See CEIX stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.