In this piece, I evaluated two cybersecurity stocks: CrowdStrike Holdings (CRWD) and Fortinet (FTNT). A closer look suggests a long-term bullish view for CrowdStrike and a neutral view for Fortinet.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

CrowdStrike offers advanced cloud-based endpoint security through its Falcon platform using a subscription-based software-as-a-service (SaaS) model that delivers various cloud modules. Meanwhile, Fortinet provides cybersecurity and networking solutions with the goal of securing people, devices, and data everywhere through its portfolio of 50 enterprise-grade products.

CrowdStrike stock has tumbled 27% over the last three months, although it’s still in the green year-to-date, up 12%. The stock remains up 69% over the past year. Concurrently, Fortinet shares have soared 29% over the last three months and are up 32% year to date.

CrowdStrike’s plunge and Fortinet’s surge can be attributed to the same thing: the July 19 global outage of airlines and various other industries that was blamed on an update from CrowdStrike that crashed computers worldwide.

Thus, a key question now is whether CrowdStrike offers a buy-the-dip opportunity, but there’s much more to consider, especially when it comes to how the company stacks up to Fortinet.

CrowdStrike Holdings

At a P/E of 409x, CrowdStrike certainly isn’t cheap, but its forward P/E of 78.1x suggests its earnings will soar. While there is a mix of positive and negative factors, the positives slightly outweigh the negatives. Thus, a long-term bullish view seems appropriate due to the company’s extreme growth and because the stock hasn’t been this cheap on a P/E basis since it became profitable.

One thing that sets CrowdStrike apart from Fortinet is that it offers its services entirely via the cloud, while Fortinet offers end-to-end solutions that include on-premises devices. CrowdStrike’s Falcon platform is designed to consolidate cybersecurity solutions and stop breaches. The company’s platform collects and integrates data across an entire enterprise, including cloud workloads, endpoints, and third-party systems.

While CrowdStrike’s absence of on-premises solutions might appear to be a limitation, it actually positions the company favorably, given the growing emphasis on cloud-based cybersecurity. On-premises devices are often expensive and difficult to scale, which makes CrowdStrike’s cloud-based offerings all the better, future-proofing its business model.

Of course, some things about CrowdStrike aren’t widely known. For example, renowned growth investor Louis Navellier has hinted that Amazon (AMZN) founder Jeff Bezos may be involved with CrowdStrike in some capacity, though the specifics remain unclear. Given Bezos’ history with Amazon, his involvement would be seen as a significant positive for CrowdStrike’s future.

However, a potential concern involves CRWD’s CEO George Kurtz, who was the Chief Technology Officer at McAfee in 2010 during a major outage caused by a faulty security update. Recently, Kurtz has faced scrutiny again after CrowdStrike experienced its own outage. However, his experience managing similar crises could be an advantage, as he’s likely familiar with strategies to navigate such issues effectively.

Unfortunately, another big negative is that CrowdStrike insiders have been unloading shares while the stock has been falling. Normally, insiders sell into strength. Thus, the fact that they’ve placed informative sells of $25.9 million over the last three months raises concerns about confidence in the company’s short-term performance.

Nevertheless, despite the global outage, CrowdStrike has apparently lost almost no clients, at least according to Jim Kramer. Wedbush analysts estimated that fewer than 5% of CrowdStrike’s customers are likely to switch providers, indicating that the outage is expected to have a minimal impact on the company’s long-term sales.

Importantly, CrowdStrike is priced like a growth stock, while Fortinet is not. CrowdStrike’s revenue is expected to grow by 25% to 30% in the coming years, nearly in line with its latest quarterly sales growth. CrowdStrike has also enjoyed a compound annual growth rate (CAGR) of 70% since 2017 as its revenue has exploded from $50 million to $3.5 billion over the last 12 months.

Thus, CrowdStrike does deserve a growth premium versus Fortinet, although the size of that premium is debatable. However, there’s no doubt the company will bounce back from the recent outage, so it would be wise to see the latest downtick as a buy-the-dip opportunity.

What Is the Price Target for CRWD Stock?

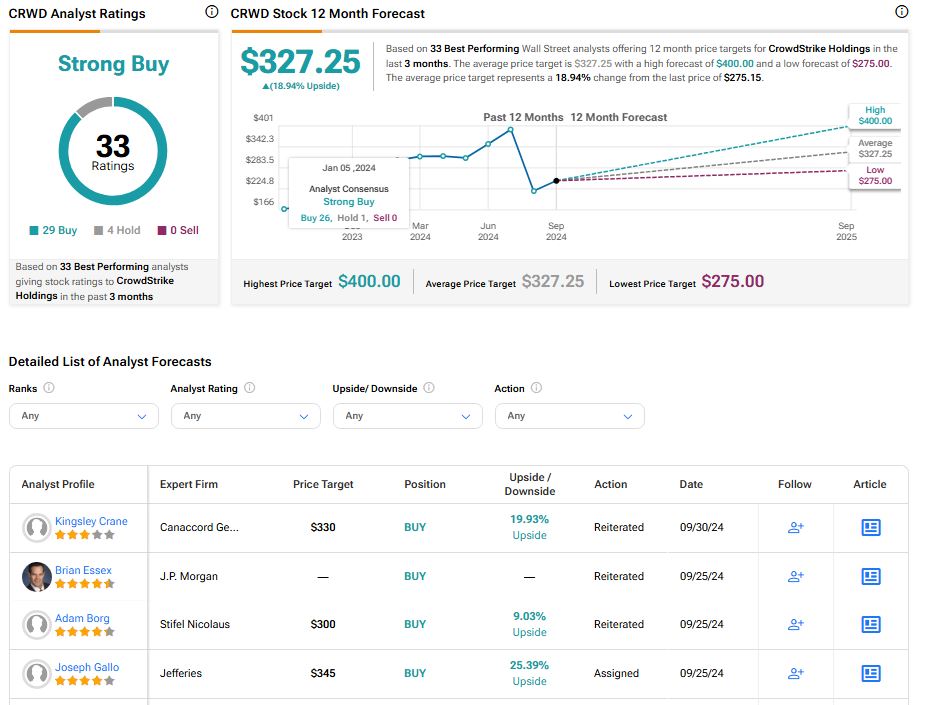

CrowdStrike Holdings has a Strong Buy consensus rating based on 29 Buys and four Hold ratings assigned over the last three months. At $327.25, the average CrowdStrike stock price target implies upside potential of 18.94%.

Fortinet

At a P/E of 45.8x, Fortinet is not priced for the tremendous growth expected from CrowdStrike. However, its current P/E is well below its mean P/E of 61.7x since November 2019. A balance of positive and negative factors suggests a neutral view might be appropriate for Fortinet.

Fortinet’s on-premises hardware suggests its customer base could be stickier than CrowdStrike’s because it’s more difficult to swap out old hardware. However, switching to a cloud-based provider like CrowdStrike could have its benefits as well due to lower costs and the lack of having to keep up with hardware upgrades.

Also, Fortinet is showing signs of a successful pivot to its non-firewall solutions, which it announced last year. CrowdStrike also offers secure access service edge (SASE) services, which puts Fortinet in direct competition with CrowdStrike. Moreover, Fortinet is switching to security operations (SecOps), another newer, more attractive offering than its legacy firewall solutions.

Unfortunately, Fortinet simply isn’t growing as fast as CrowdStrike, with a CAGR of 24% between 2017 and 2022. While the company experienced a 25% CAGR in billings during this period, its revenue growth slowed significantly in 2023, rising just 20%. This indicates a marked deceleration compared to CrowdStrike’s performance. Moreover, Fortinet’s billings rose just 14%, signaling that the company could have had its day in the sun — although it certainly isn’t going anywhere anytime soon.

Finally, the recent run-up in its shares also suggests that this might not be a great time to buy Fortinet stock. I might become more constructive on the shares if the price comes down, particularly if the company continues to report strong billings. Thus, I’d take a wait-and-see approach for now.

What Is the Price Target for FTNT Stock?

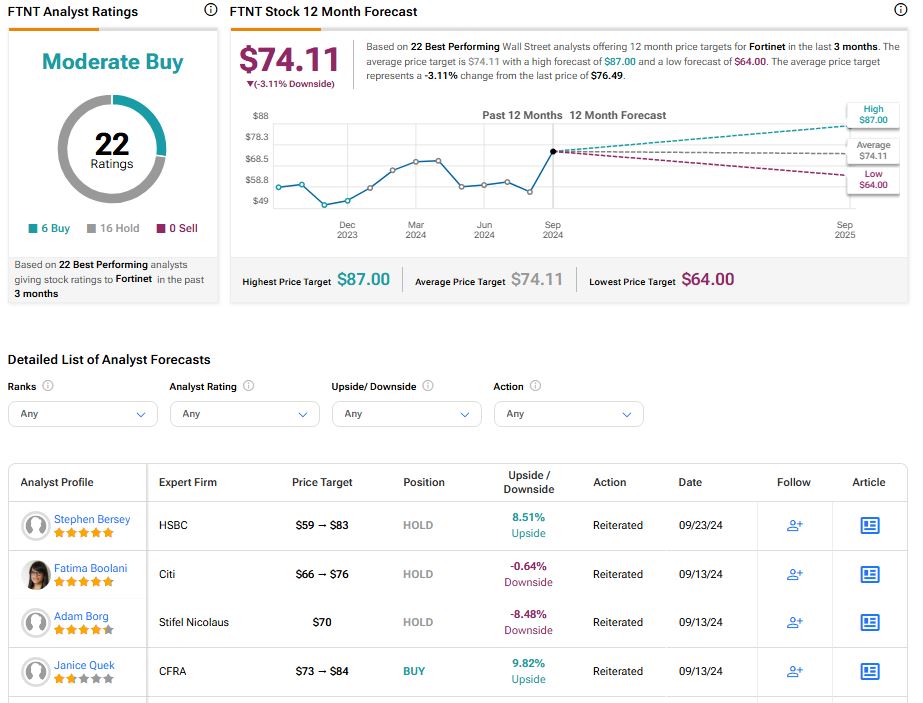

Fortinet has a Moderate Buy consensus rating based on six Buys, 16 Holds, and zero Sell ratings assigned over the last three months. At $74.11, the average Fortinet stock price target implies downside potential of 3.11%.

Conclusion: Bullish on CRWD, Neutral on FTNT

Both CrowdStrike and Fortinet are great long-term cybersecurity plays — as long as you can get past their valuations. Both stocks have enjoyed explosive long-term share price appreciation. CrowdStrike is up 17% over the last three years and 395% over the last five years. Meanwhile, Fortinet is up 34% over the last three years, 413% over the last five years, and 1,114% over the last decade. (Fortinet is much older compared to the emerging player, CrowdStrike.)

However, CrowdStrike is the clear winner of this pairing because it looks like it has more near-term opportunities than Fortinet does. As a result, a wait-and-see approach looks best for Fortinet, especially in light of the recent run-up in the shares. Meanwhile, it could be a good idea to buy the dip in CrowdStrike.