Crocs Stock (NASDAQ:CROX) is now my largest consumer discretionary holding, making up about 9% of my portfolio. After a strong Q4 and full-year report, I added to my position, impressed by the company’s numbers. It was another year of double-digit revenue growth for the Crocs brand. Further, despite facing some challenges, the HEYDUDE brand also shows strong growth prospects. Given that the shares appear substantially undervalued relative to Crocs’ future outlook, I remain very bullish on the stock.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Breaking Down Crocs’ FY2023 Results — Record Financials Across the Board

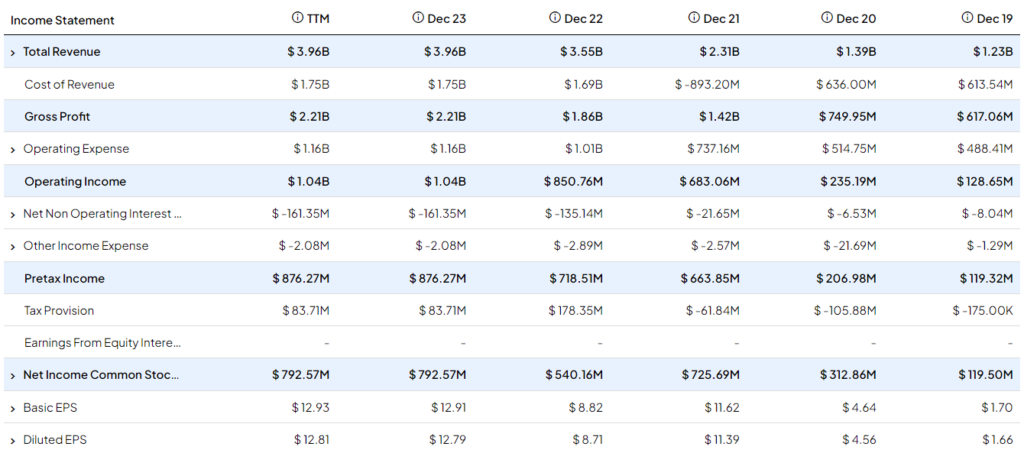

Crocs’ FY2023 results were very strong, characterized by record revenues, a record operating margin, and record earnings per share. In particular, revenues came in at nearly $4.0 billion, up 11.5%, or 12.0% on a constant-currency basis, compared to last year. Further, Crocs’ operating income margin reached an all-time high of 26.4%, expanding by 150 basis points during this period. Finally, EPS was a record $12.79, up 46.8% over FY2022, or $12.03 on an adjusted basis, up 10.2%, and also a record.

Let’s take a look at Crocs’ two separate brands, the core Crocs brand, and HEYDUDE, which collectively led to this performance.

The Crocs Brand Is Not Losing Any Steam

From my experience reading investors’ theses on the stock, the company’s core Crocs brand has long been anticipated to start losing steam. The argument here is that, at the end of the day, its iconic clog shoe remains ugly, and the only reason the brand saw increased traction in recent years is due to a fashion trend that is destined to eventually fade away. I have been hearing this argument for at least two years since Crocs saw a notable revenue boost in 2020-2021. Yet, these concerns have yet to materialize.

Particularly, the Crocs brand continues to see strong consumer demand, with its revenues reaching $3 billion last year, up 13.3%, or 14.0%, on a constant-currency basis. The fact that Crocs, which again is considered a “cult brand,” keeps posting double-digit revenue growth should not come as a surprise. The company has diversified the brand into sneakers, boots, loafers, and even sandals.

Clogs, despite their love-them-or-hate-them nature, grew revenues by 12% for the year, driven by solid developments in both the company’s Classic and new Clog franchises (e.g., partnerships with artists). At the same time, sandal sales surpassed the $400 million mark for the first time, growing 29% versus last year. In fact, sandals, a product category the company introduced as recently as in 2022, now make up 13% of Crocs’ sales mix.

I believe that the Crocs brand will continue performing very well, driven by its vibrant and enthusiastic customer base. Besides the Crocs brand surpassing last year’s record sales, there are also many other compelling indicators reinforcing this argument. I will give you two noteworthy ones.

Firstly, in 2023, a significant 61% of consumers who bought sandals via Crocs’ e-commerce channels were entirely new to the brand, showcasing its expanding appeal in the space.

Further, the Jibbitz business, the charming accessories sold by Crocs for shoe customization, posted a remarkable 17% increase, exceeding $250 million and now constituting approximately 9% of Crocs’ total revenue. Considering the novelty nature of this product and the fact that it’s typically bought as an add-on to the basic shoe, its strong sales growth truly underscores the fondness of Crocs’ customer base for the brand.

HEYDUDE Is Struggling, But a Turnaround Is Possible

Moving to the HEYDUDE brand, I have to admit that this one is struggling. It’s pretty hard to ignore this fact. It seems that management has struggled to integrate the brand into its overall ecosystem smoothly.

Its revenues for the year rose by just 6% to $949 million. While DTC (Direct-to-Consumer) sales did grow by a significant 18.9%, wholesale revenues — a much larger chunk of the business — fell by 1.3%, hampering the brand’s growth.

Nevertheless, I believe HEYDUDE is poised for a significant acceleration in growth, as management has multiple available levers to make this possible. As shown through the notable uptick in DTC revenues, the HEYDUDE brand should be able to leverage Crocs’ successful retail playbook. The company has already bet on this avenue for growth.

HEYDUDE opened five outlet locations in the second half of 2023, and management stated that they have been pleased with the results thus far. The company now plans to launch 30 outlet stores in 2024 over the course of the year. For context, retail is about one-third of the North American business for the Crocs brand and is highly profitable.

Crocs Stock Appears Cheap Relative to Its Optimistic Outlook

Crocs is set to maintain strong traction in 2024, with management’s outlook pointing to another year of record revenues and profits. Based on the projected numbers and Crocs’ overall brand value, I find the stock to be notably undervalued.

Specifically, for FY2024, management expects revenue growth between 3% and 5% and adjusted EPS of $12.05 to $12.50. Note that this estimate doesn’t include the positive impact of any potential buybacks, which are expected to pick up this year.

Still, if we are conservative and assume the company achieves the midpoint of this target (~$12.28), then the stock is trading at a forward P/E of just 9.4x. I believe this a very attractive multiple for a high-margin iconic brand, even if we were to assume stagnated financials, let alone growth.

Is CROX Stock a Buy, According to Analysts?

Loomg at Wall Street’s sentiment on the stock, Crocs currently boasts a Strong Buy consensus rating based on 10 Buys and two Holds assigned in the past three months. At $133, the average Crocs stock price target implies 13.4% upside potential.

If you’re wondering which analyst you should listen to if you want to buy and sell CROX stock, the most accurate analyst covering the stock (on a one-year timeframe) is Sam Poser from Williams Trading. His track record is incredible, with an average return of 62.56% per rating and a 67% success rate. Click on the image below to learn more.

The Takeaway

Crocs’ FY2023 results solidified my conviction in the stock. Its core Crocs brand continues to defy skeptics and deliver impressive revenue growth. Further, despite some challenges, HEYDUDE shows promise for a turnaround, leveraging strategies from Crocs’ successful playbook.

With management sharing an optimistic outlook for 2024 and the stock appearing undervalued against the company’s adjusted EPS target, I remain bullish on Crocs stock. I will keep adding to my position occasionally throughout any potential dips, despite Crocs already being my largest position sector-wise.