Crocs’ (NASDAQ:CROX) performance continues to impress, with management’s superb execution supporting the company’s momentum. Despite some investors anticipating a decline in Crocs’ growth following the 2020-2021 frenzy, supporting the notion that the company’s unique designs would eventually go out of fashion, Crocs continues to thrive!

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

The core brand continues to sell rapidly, while the acquisition of HEYDUDE has further boosted the company’s revenue growth and profitability prospects. Yet, despite the stock’s considerable gains lately, it remains rather cheap, in my view. Accordingly, I remain bullish on CROX stock.

Crocs Sell Like Hotcakes, and So Do HEYDUDEs

You can hate on Crocs and its “ugly” designs all you want, but sales don’t lie. The clogs, as the company calls them, sell like hotcakes. By partnering with a variety of celebrities and influencers, Crocs has created hundreds of unique clog designs that cater to a diverse range of target groups. This approach has proven highly successful in attracting a broad customer base and driving sales.

And then, you have HEYDUDE, the brand known for its lightweight and comfortable shoes, which Crocs acquired last year. With Crocs’ existing sales channels and infrastructure in the same market, HEYDUDE is poised to achieve even greater heights in the future. All this was reflected in the company’s most recent results, which, once again, were explosive.

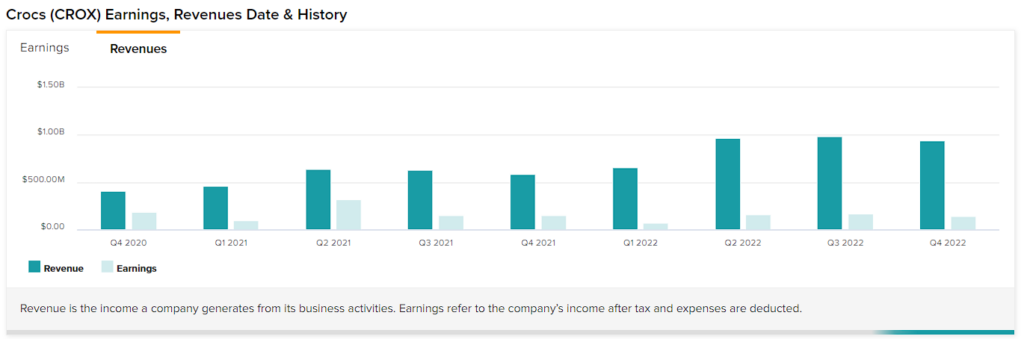

For its fiscal Q4, Crocs reported revenue growth of 61.1% to $945.2 million, or 64.8% on a constant-currency basis. Speaking of momentum, this figure compared with revenue growth of 63% in the previous quarter, sending the bear case regarding decelerating momentum down the drain.

More specifically, in Q4, the Crocs brand grew 13.5%, with growth once again driven by vigorous DTC (direct-to-consumer) comparable sales growth of 18.5%.

Again, I want to highlight that Crocs’ one-hit-wonder growth of the past couple of years was supposed to be backed by a TikTok trend. Other bear cases supported that Crocs’ massive sales growth in 2020-2021 was due to the pandemic driving sales of comfy in-house shoes.

Few cared to admit that Crocs had become a staple in the streetwear and “wear-what-you-like” fashion scene. And indeed, the core Crocs brand (ex-HEYDUDE) continues to grow on top of last year’s record numbers in the double-digits.

The HEYDUDE brand wasn’t in the company’s portfolio last year to have comparable metrics, but according to management, the $279.2 million in sales HEYDUDE achieved during Q4 are 34% higher than last year. This is a very impressive pace of growth, given that the company is transforming HEYDUDE’s sales channels while also shutting down its Russian operations.

Building the Most Profitable Shoe Company

Following the acquisition of HEYDUDE, it appears that Crocs’ management is essentially building the most profitable shoe company (margins-wise) possible. The company is using a tried-and-true recipe, similar to the one that has made Crocs successful, i.e., to produce lightweight shoes at scale with below-average production costs.

This approach allows the shoes to be sold at reasonable prices and easily fly off the shelves. Crocs typically retail for $35-$55, while HEYDUDEs are priced at $50-$60, which is significantly lower than the average price of most footwear on the market.

The result? Fantastic margins. The company’s adjusted operating margins, including both Crocs and HEYDUDE, came in at 26%, driven by outstanding gross margins of 52.5%.

To give some perspective of how impressive these margins are, Skechers U.S.A.’s (NYSE: SKX), Steven Madden’s (NYSE: SHOO), and Shoe Carnival’s (NASDAQ: SCVL) gross margins stood at 48.4%, 41.2%, and 38%, respectively, in their most recent quarterly reports.

Even Nike (NYSE: NIKE) and Adidas (OTC: ADDYY), which have way more efficient production and scaling capabilities while also selling shoes (and other high-margin products) at higher price points, featured gross margins of 42.9%, and 49.0%, respectively.

No wonder that following higher sales, Crocs was able to achieve another record in terms of its profitability, with adjusted earnings per share landing at $10.92 for Fiscal 2022. This implied a robust year-over-year increase of 31.3%.

Is CROX a Good Stock to Buy, According to Analysts?

Regarding Wall Street’s view on the stock, Crocs has a Moderate Buy consensus rating based on five Buys and two Holds assigned in the past three months. At $156.43, the average CROX stock forecast implies 31.8% upside potential.

The Takeaway

CROX stock is up 62% in the past 12 months. Yet, it appears that the stock has more gas in the tank. Management projects another year of record financials, expecting double-digit revenue growth and adjusted earnings per share to be between $11.00 and $11.31.

At the midpoint of this range, shares of Crocs are currently trading at a forward P/E of 10.6. This is an objectively inexpensive multiple (a 9.4% forward earnings yield), given the company’s double-digit growth being sustained.

Additionally, this suggests that Crocs is trading at a considerable discount compared to its competitors, who are trading at higher forward P/Es in the mid-teens or above. Thus, I am confident that there is a strong opportunity for Crocs’s stock to appreciate in the future.