It’s become mainstream to predict a recession this year. The Federal Reserve is on a steady path of interest rate increases – the latest was a 25-basis point hike announced today – to fight inflation, and the central bank has already indicated it will stay this course until inflation is well and truly down. By definition, that will involve increasing the cost of capital to choke off the money supply, and likely spark a recession in the bargain.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

But not everyone is jumping onto that train. Watching the situation from investment banking giant Credit Suisse, chief US equity strategist Jonathan Golub takes the contrarian stance. Predicting a lackluster year for stocks, rather than an outright collapse, Golub said, “If I’m correct in the way that we do avoid this recession in the near-term, the market will continue to give you a little bit of relief. So the call is for multiples rise up a little bit, earnings to fall a little bit, and then you end up with an entirely uninspiring 3-4% return for equities between now and the end of the year.”

What investors need to remember here is that Golub’s ‘uninspiring return’ represents an average – and there will be plenty of stocks beating that average and bringing serious growth to the table. His colleagues among the Credit Suisse stock analysts are highlighting this fact, by publishing recommendations for stocks that, in their view, will bring gains of 30% and go up from there. In any market condition, growth like that will earn a second look from investors.

For our part, we can give these Credit Suisse picks that second look. Using the data tools at TipRanks, we’ve pulled up the details on two of them; here they are, along with the analyst commentary.

Exelixis, Inc. (EXEL)

The first company we’re looking at is Exelixis, a biotech firm that has reached the brass ring – it has a line of approved medications on the market, generating steady revenues, and has a recent history of positive quarterly earnings. Exelixis’ lineup of medications is focused on cancer treatment, and the company bills itself as a ‘resilient leader’ in the oncology field.

The flagship product is cabozantinib, a medication used in the treatment of thyroid and renal cancers. Exelixis markets the drug under two brand names, Cabometyx and Cometriq, and these, along with the cobimetinib formulation Cotellic – marketed in partnership with Genentech – form the current core of the company’s business.

It’s a lucrative core, too. According to the recent release of its preliminary 4Q22 and full year 2022 financial results, Exelixis saw total revenues of $1.6 billion last year, compared to a total top line of $1.4 billion in 2021. Looking ahead, the company is guiding toward a top line between $1.575 billion and $1.675 billion for 2023. The most recent bottom line numbers come from 3Q22, when Exelixis reported a GAAP net income figure of 23 cents per share, beating the consensus estimate of 20 cents a share. Exelixis will report its complete data for 4Q22 on February 7.

Going forward in 2023, Exelixis’ main priority will be conducting the clinical trial program to expand the product line. Coming up this year, the company will have a data readout for a Phase 3 clinical trial of cabozantinib in the treatment of metastatic non-small cell lung cancer. This study is being run as a combination therapy with atezolizumab and has enrolled 366 patients. Also in a Phase 3 trial is zanzalintinib, a new drug candidate (previous called XL092) for the treatment of advanced non-clear-cell renal carcinoma. The study has 291 patients and is due for expansion.

The pipeline doesn’t come cheap, but in addition to its revenue stream, Exelixis has deep pockets. The company finished 3Q22 with $2.1 billion in cash and liquid assets on hand, an increase from the $1.9 billion available at the end of 2021.

Joining the bulls, Credit Suisse analyst Geoffrey Weiner takes an upbeat stance on this company and its stock.

“Based on our conversations with key opinion leaders (KOLs) and analysis of the renal cell carcinoma (RCC) landscape, we project product sales could grow to ~$2B in 2025, even without potential label expansions,” Weiner noted.

“EXEL has sufficient cash flow to bridge the gap between cabo and value creation from its pipeline, which includes several clinical-stage candidates and an underappreciated/growing antibody drug conjugate (ADC) pipeline… We think the prospects for the home-grown asset zanzalintinib/XL092 (next-generation cabo-like TKI) and XB002 (TF-ADC) are overlooked, as is EXEL’s move to build out an ADC pipeline. We believe there are multiple clinical catalysts to drive pipeline interest over the next one to two years,” the analyst added

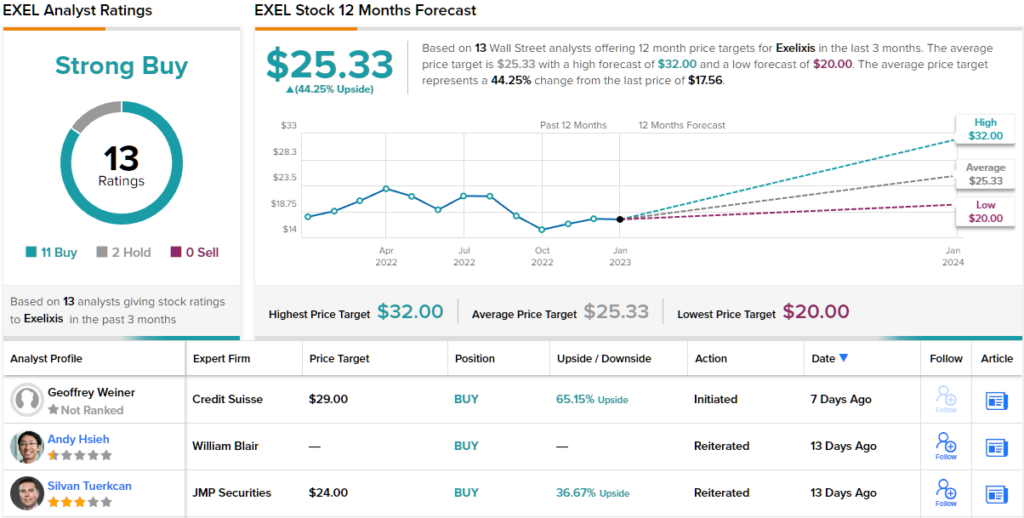

Gazing into the near future, Weiner sees fit to rate EXEL shares an Outperform (i.e. Buy), with a price target of $29 indicating potential for a robust 65% share appreciation over the coming year.

Overall, EXEL shares maintain a Strong Buy analyst consensus rating, based on 13 recent reviews. These reviews break down 11 to 2 in favor of Buys over Holds, and the company’s $25.33 average price target implies a 44% upside potential from the current share price of $17.55. (See EXEL stock forecast)

Boyd Gaming Corporation (BYD)

The next Credit Suisse pick we’re looking at is Boyd Gaming, one of the major casino operators in the gaming industry. Spreading out of its Las Vegas home, Boyd now has 28 gaming facilities and properties across 10 states, and in addition, the company has a 5% equity stake in FanDuel Group, a leading sports betting operator. Boyd’s expertise has also brought the company a management agreement with a tribal casino in northern California.

This array of properties has provided Boyd a strong revenue stream and income. The company will report its full-year 2022 results tomorrow after market close, but looking back to 3Q22, we see that Boyd had $877.3 million at the top line. This was up 4% year-over-year, and with a 9-month total revenue of $2.63 billion, the company is well on track to beat last year’s full-year figure. At the bottom line, Boyd’s Q3 adjusted earnings of $1.48 per share were up more than 13% y/y.

Boyd has gotten a boost from strong consumer spending coming out of the pandemic period. It remains to be seen if this will hold up going forward; a reduction in the rate of inflation will be supportive of the consumer discretionary spending segment generally.

Of interest to investors, Boyd this year reinstated its quarterly dividend payment. The company had suspended dividends starting in 2020, but restarted the payments in 1Q22. The current dividend is 15 cents per common share, more than double the last 2019 payment. At this rate, the payment annualizes to 60 cents and gives a small yield of 1%.

5-star analyst Benjamin Chaiken, in his write-up of Boyd for Credit Suisse, lays out several reasons why this stock should do well going forward: “(1) Growth in the Downtown Las Vegas market and BYD’s investment in the Freemont property. We think the Downtown market could inflect higher as corporate demand on the Strip returns… (2) BYD is spending $100m to move its Treasure Chest casino from a riverboat to a newly developed land-based asset adjacent to the existing property. We think new amenities, better access, and a more cohesive casino floor could drive a 20-30% ROI. (3) BYD purchased Pala Interactive in November ’22, so annualizing the acquisition should be a small tailwind in ’23… (4) BYD has a Tribal management contract for the Sky River Casino, which we estimate will drive $36m of mgmt. fees in ’23…”

Based on these four reasons, Chaiken rates BYD shares an Outperform (i.e. Buy) rating, along with an $82 price target that suggests a 12-month potential upside of 31.5%. (To watch Chaiken’s track record, click here)

Overall, this stock gets a Moderate Buy from the Street’s analyst consensus, based on 7 analyst reviews that include 4 Buys, 2 Holds and a single Sell. The stock is selling for $62.35 and its $71.33 average price target suggests an upside potential of ~14% on the one-year horizon. (See BYD stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.