ContextLogic (WISH) is set to release second-quarter 2021 earnings on August 12.

ContextLogic is an American online ecommerce platform that facilitates transactions between sellers and buyers.

Since going public last December, shares of the company have lost around 51%, and are now trading at over $9. A strong set of numbers in Q2 could help the stock regain investors’ confidence, so let’s take a closer look at what analysts on the Street are expecting.

Q2 Expectations

For Q2, the Street expects ContextLogic to report a loss per share of $0.14 and revenues of $723.02 million.

Meanwhile, the Earnings Whisper number, or the Street’s unofficial view on earnings, stands at a loss of $0.17 per share. (See ContextLogic Dividend Date and History on TipRanks)

For the second quarter, ContextLogic expects revenues in the range of $715-$730 million, indicating year-over-year growth of 2%-4%.

ContextLogic’s Prior Quarter Snapshot

ContextLogic witnessed strong top-line growth in the first quarter.

The company reported revenues of $772 million, which were up 75% year-on-year. The revenue growth was driven by strength in marketplace revenue and logistics revenue.

Meanwhile, losses widened to $128 million in Q1 from a loss of $66 million in the year-ago quarter.

What to Watch for in ContextLogic’s Earnings

ContextLogic, like other online marketplaces, is currently benefiting from the significant rise in ecommerce. The majority of the items sold on its marketplace are unbranded, and aimed at budget-conscious buyers who are not looking for luxury or high-quality items.

The company mainly generates its revenue from core marketplace, logistics, and its ProductBoost advertising business.

WISH’s core marketplace, which includes commission fees earned from the sale of products, grew 40% year-over-year to $477 million.

Specifically, Core Marketplace revenues are expected to have increased in the second quarter as a result of WISH’s rising monetization activities and strong focus on lifetime value (LTV) consumers.

In addition, the company is working to increase its product offerings on the platform. It is attempting to expand its inventory to include high-frequency items as well as branded goods. Further, the company is making efforts to diversify its merchant network by expanding outside of China. That will reduce the dependence of WISH on China, making its revenue stream more reliable.

Already during Q1, the number of merchant partnerships outside of China climbed 351% year-over-year, which remains quite encouraging.

Coming to logistics, this segment’s revenue grew 338% year-over-year to $245 million in Q1. The Wish Express listing grew by 414% year-over-year, and shipping-related refunds fell by 43% year-over-year.

Wish Express, to put it simply, is a shipping program that that offers express shipping to online shoppers, similar to Amazon Prime (AMZN) and Walmart 2-day delivery.

The logistics division is likely to have performed strongly, owing to merchants’ high level of adoption of the company’s shipping services. The company is making efforts to strengthen its logistics capabilities through strategic partnerships with local carriers. These agreements, as well as the increased number of listings on Wish Express, are likely to be big positives.

Meanwhile, investors should also consider WISH’s important metrics, such as mobile monthly active users (MAU) and core marketplace income per active buyer.

To note, core marketplace revenue per active buyer increased 76% year-over-year, driven by the company’s focus on acquiring higher LTV users. On the other hand, monthly active users (MAU) fell 7% year-over-year, and LTM active buyers decreased 3% year-over-year to 61 million. The company hopes that trend will reverse as its logistics improve.

To conclude, ContextLogic’s management has expressed belief in the company, but remains cautious about the future prospects due to the unpredictable climate.

In the last earnings call, the company stated, “We are cautiously optimistic about the remainder of 2021. However, we continue to navigate uncertainty given the ongoing COVID-19 pandemic and other factors, including implementation of value-added tax in Europe starting in July 2021, which could have an impact on our results later this year.”

Analysts’ Recommendations

On July 21, Justin Post of BofA downgraded the rating to Hold from Buy and set a price target of $12.00. This implies 22.1% upside potential to current levels.

On July 2, another analyst, Shweta Khajuria of Evercore ISI, downgraded the rating to Hold from Buy and set a price target of $13.00. This implies 32.3% upside potential to current levels.

The Wall Street community is cautiously optimistic about the stock, with a Moderate Buy consensus rating based on 2 Buys and 4 Holds. The average WISH price target of $16.00 implies 62.8% upside potential from the current levels.

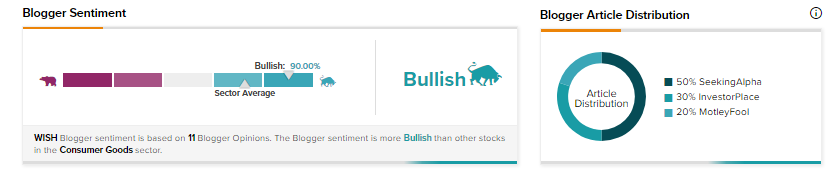

TipRanks data shows that financial blogger opinions are 90% Bullish on WISH, compared to a sector average of 73%.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.