The famous (or, shall we say, infamous?) coworking space provider WeWork (WE) has filed for bankruptcy protection. While the company’s plight is mostly blamed on its unruly founder and the flawed business model he’s built, the timing of WE’s final downfall is directly correlated with the ails of the commercial real estate market that are now coming to the forefront. As investors weigh high dividends against potential capital losses, they shouldn’t overlook one thriving corner of the real estate market.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Safe Space for Rent

WeWork’s bankruptcy couldn’t come at a worse time. The state of the office properties, and commercial real estate (CRE) in general, is shaky, and it certainly doesn’t need another hit to investor sentiment.

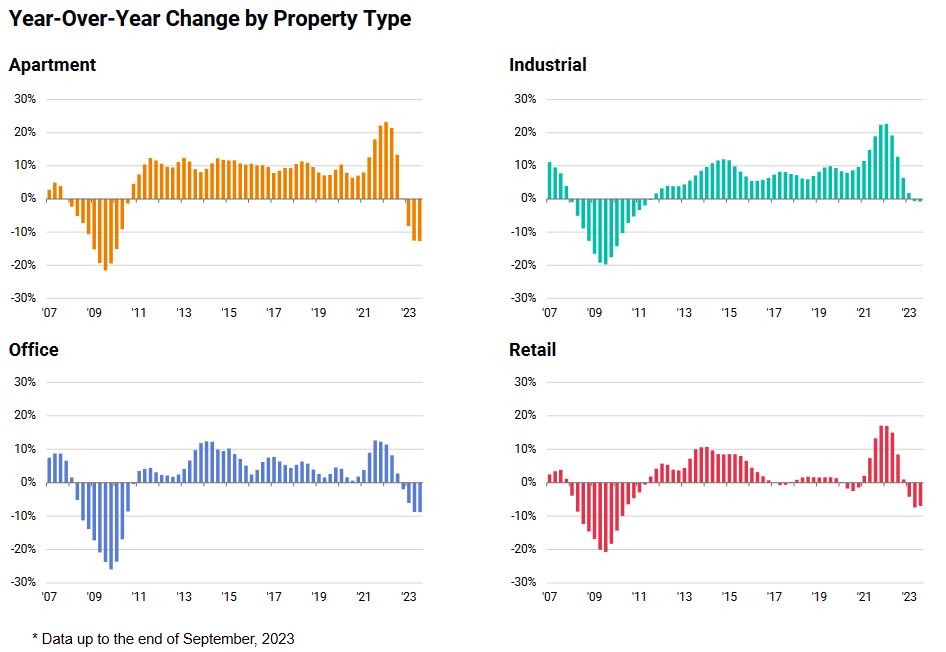

The fact is that commercial real estate had been on the decline before the current crisis, due to several long term-trends. The Covid-19 pandemic led to a sharp acceleration of these trends, with malls and office buildings bearing the brunt of a surge in online shopping and work-from-home tendencies. What’s changed is that now, instead of pockets of trouble in the generally robust market, the whole CRE market looks wobbly, with some exceptions on the margins.

As demand for commercial property is on the decline, prices are falling across the board. Numerous new projects throughout the country have been suspended, put on hold, or even canceled altogether because of the lack of financing, surging input and labor costs, and a much softer demand outlook. Meanwhile, existing CRE owners are facing rising vacancies at their locations, be that offices, malls, retail spaces, and even hotels and industrial use properties. They are saddled with higher utility bills, exploding insurance premiums, and mounting operating expenses. Investors have long viewed commercial real estate, whether in the form of individual companies’ stocks, Real Estate Investment Trusts (REITs), or ETFs that hold them, as a significant source of income, since the sector is known for its propensity to pay high dividends. However, as capital losses threaten to outpace that income, in some cases by a wide margin, property investors are recalculating their exposure to the sector.

Sources: Google Finance, Vanguard

Maturing Troubles

Since the Federal Reserve began its monetary tightening campaign early last year, the activity in the industry has been trending even lower, and lenders have been cutting back on financing. After the banking crisis of March 2023, regional and smaller banks, which account for the majority of CRE lending, have been pulling back new lending and refinancing on an increasingly larger scale, with real estate bearing much of the brunt. These banks are also reporting a sharp increase in non-performing CRE loans. For instance, PNC Financial (PNC) said that NPLs connected to commercial real-estate projects have doubled in the third quarter versus the second quarter of 2023.

As the interest rates are projected to remain at their 22-year high for some time, CRE lending doesn’t look any closer to a turnaround. While loans are still available, they are not affordable for less-than-stellar quality borrowers – and even the best of breed pay a steep premium due to the higher risk apparent within the industry. There’s little demand for high-cost loans from investors and developers; at the same time, the supply of loans is deteriorating.

Banks, private debt funds, real estate investment trusts (REITs), and other lenders, are bracing for a wave of delinquencies and write-offs, particularly in 2024 when more than $900 billion of CRE loans mature throughout the year. In total, $2.8 trillion in CRE loans are coming due by 2027. As interest rates are now roughly triple what they were just a couple of years ago, refinancing these loans will be a challenge.

Distressed to the Core

With the economy expected to weaken further and the Fed promising to keep rates “higher for longer,” CRE is facing prolonged pressures. According to Capital Economics research, office properties could lose up to 40% in price until the end of 2024 – a moderate outlook, as they’ve already lost 21% within the past year. Shopping malls aren’t expected to be hit as much just because their prices were already low even before the interest rates started to climb.

According to MSCI data, the dollar amount of the distressed loans associated with CRE reached its highest since 2013 in the third quarter of 2023. Of those slated as “distressed” in the past few months, 93% were office-building loans. According to analysts, about $1.2 trillion of CRE debt is labeled as “potentially distressed.”

Source: MSCI, Inc.

But it’s not only offices that are feeling the pain. Long thought to be commercial real estate’s “safe haven,” the niche of residential buildings is now looking shaky, too. For many years, investors were attracted to multifamily buildings, which provided them with stable, ever-rising rent income. As a result of the “safe bet” perception of residential CRE investments, many buyers of these properties have financed them through various floating-rate loans, and now they are underwater on those properties, or firmly on the way there.

Like in the past, right now there aren’t many vacancies in the residential space, and the demand remains robust. In the past two years or so, many would-be home buyers opted for rent instead, as high mortgage rates make home purchases unreachable for many tenants; surging demand, coupled with rising inflation, has led to a sharp increase in rent prices. The demand in the residential niche isn’t a problem – but the buildings’ owners, whether individuals, firms, or funds, face the same refinancing problems as the developers. In addition, they now have to deal with renters who can’t afford higher rents, which adds to mounting debt-repayment difficulties for owners.

Housing the AI Revolution

As with most investment themes, there are always exceptions to the overall trend. One niche that immediately stands out among the almost-ruins of the CRE market is the data-center corner of that space.

In the past two decades, the accelerating global shift to a digital economy has led to a strong increase in the prevalence of data centers – dedicated facilities that house a network of computing and storage resources used for building, running, and delivering applications and services, and for storing and managing the data associated with those applications and services.

The proliferation of cloud storage and computing, streaming services, and social media platforms, as well as the expanding network of connected devices known as the Internet of Things (IoT), are major factors fueling the current use of data centers. In recent years, the advancement of machine learning (ML) and artificial intelligence (AI), autonomous vehicles, and blockchain technology has significantly increased the necessity for data storage capacity; this increase is expected to accelerate greatly in the next years. Much of the expected parabolic growth in data storage volumes stems from the needs associated with massive amounts of data needed to run AI models. As we are just entering the AI era, these trends will greatly intensify, drawing vast amounts of investment.

These factors together have helped data centers maintain a stable source of income through various economic eras. High rates of tenant retention (due to high switching costs) and extended lease terms also play a role in ensuring the sector’s ongoing strength. With many tailwinds in place, the sustained need for data center facilities seems solid in the short- as well as long-term.

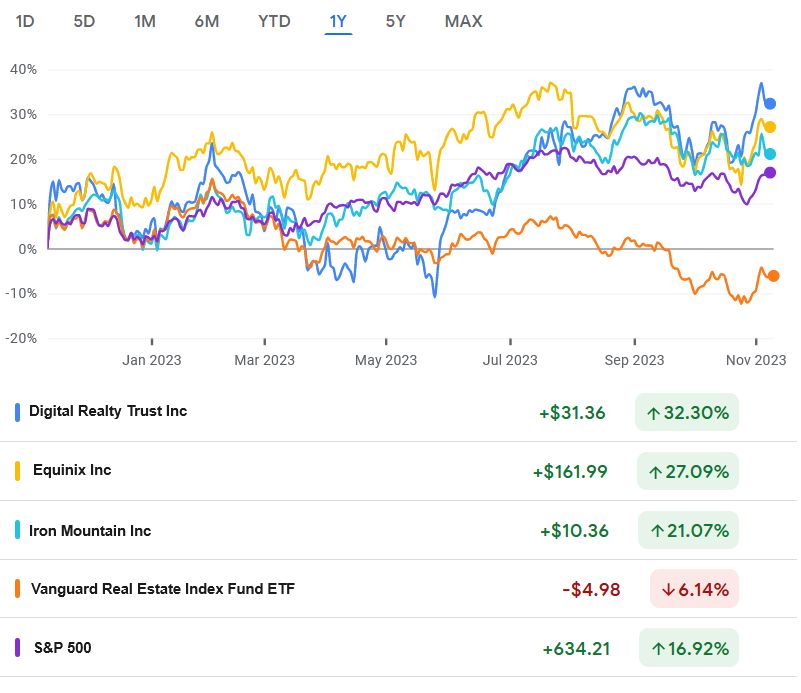

This is where data center REITs come into the spotlight. These REITs are investment trusts that own and manage these all-important IT infrastructure facilities. While all types of REITs carry risks, such as relatively high sensitivity to interest rates, their benefits strongly outweigh shortcomings, especially in the medium to long term. Besides growing demand, extra-low vacancy rates, and strong pricing power supporting the growth of investors’ returns, these investment vehicles feature high dividend yields. The average dividend yield of data-center REITs is 3.1%, versus the S&P 500’s (SPX) current average yield of 1.6%.

Investors can gain exposure to this lucrative niche whether by directly investing in REITs or by buying an ETF holding shares in the underlying trusts. The largest and best-known data center REITs are Digital Realty (DLR), Equinix (EQIX), and Iron Mountain (IRM). Their share performances in the past 12 months have outpaced not only other CRE investment vehicles but the broad market as well:

Source: Google Finance

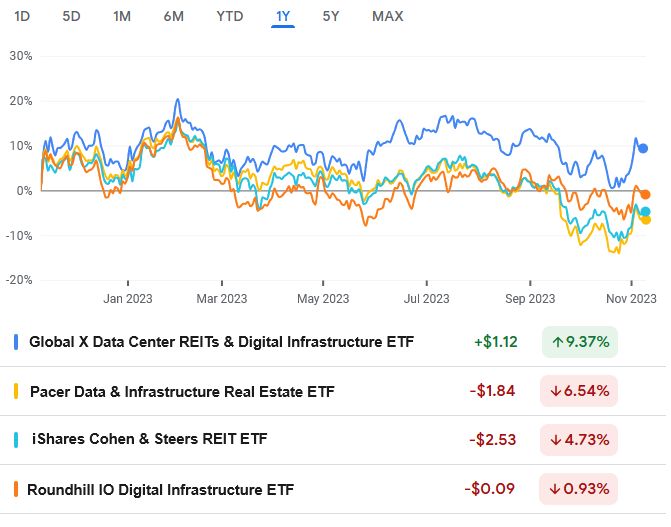

In addition, some ETFs provide investors access to data center REIT stocks. There is one pure-play data center REIT ETF, Global X Data Center REITs & Digital Infrastructure ETF (VPN), which invests in stocks of data center REITs and related digital infrastructure companies. In addition, there is the Pacer Data & Infrastructure Real Estate ETF (SRVR), which mostly holds stocks of real estate companies from developed markets that are related to data and infrastructure, but also includes telecom companies, general real-estate trusts, and ETFs, and more. There’s also Roundhill IO Digital Infrastructure ETF (BYTE), which holds global stocks that earn the majority of their revenues from digital infrastructure assets; most of its top holdings are global telecom companies, although it has significant exposure to major data-center REITs. Furthermore, there are a few broader property REIT ETFs with various degrees of exposure to data infrastructure, with the most well-known being iShares Cohen & Steers REIT ETF (ICF). However, these funds’ exposure to other CRE sectors leads to underwhelming performance compared to the pure-play data-center instruments.

Source: Google Finance

In conclusion, while the general commercial real estate market doesn’t provide many reasons for optimism, the data center niche can offer lucrative investment opportunities, combining high dividend income and an outlook for continued capital appreciation. As always, though, investors are strongly advised to take into account macro factors, company fundamentals, and sector outlook, when weighing potential investments, utilizing various research tools and harnessing expert analysis.