Coinbase Global (NASDAQ:COIN), the largest crypto platform in the U.S., has seen its market value surge by 225% this year, seemingly pushing its valuation ahead of the business. Bitcoin (BTC-USD) is up 124% this year, and this stellar performance has been a key ingredient of Coinbase’s success, as the company’s revenue is highly correlated with crypto trading volumes.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Growing expectations for the approval of a spot Bitcoin ETF have also played a role in boosting investor sentiment toward Coinbase. Despite the long runway for growth, I find Coinbase richly valued today, which forces me to stay neutral on Coinbase stock.

The Improving Business Fundamentals

In November 2021, Bitcoin prices peaked at just over $64,000. After reaching a low of close to $16,000 in December 2022, Bitcoin prices have recovered to $37,300 today, but the previous highs seem a long distance away. Coinbase generates the bulk of its revenue from transaction fees, which are correlated to the trading volumes of cryptocurrencies. During crypto bull markets, transaction revenues are bound to surge, while the opposite is true for crypto bear markets.

On the back of a substantial decline in crypto trading volume, Coinbase reported double-digit year-over-year revenue declines in six consecutive quarters from Q1 2022 to Q2 2023. This lackluster financial performance weighed on Coinbase stock, not surprisingly. Bucking the trend, the company reported a modest 8% year-over-year increase in revenue in the third quarter, aided by subscriptions and services revenue that came to $334 million.

Compared to the second quarter, Transaction revenue declined 12% to $289 million, while Subscription and Services revenue was flat in Q3, which is an early indication of the stability and predictability of subscription revenue.

During the third quarter, Coinbase registered growth in USDC (USDC-USD) on its platform alongside an increase in staked balances, boosting subscriptions and services revenue. The company’s efforts to diversify its revenue base are finally beginning to contribute to its financial performance. If Coinbase can continue on this growth trajectory, the substantial volatility associated with its stock is likely to subdue in the future.

For now, Coinbase mirrors the movements of major cryptocurrencies, but in the long run, the company has the potential to emerge as a crypto services provider that does not entirely rely on trading fees.

As a result of aggressive diversification efforts, Coinbase now offers various products and solutions to retail and institutional clients. These include exchange services, custodian services, crypto debit cards, and data analytics solutions. The growing depth of Coinbase’s product portfolio is likely to help the company build competitive advantages in the long term.

The firm’s aggressive cost-reduction efforts are yielding encouraging results, too. For the third quarter, Coinbase reported a net loss of $2.3 million on revenue of $623 million, in contrast to a net loss of $545 million reported in the third quarter of 2022. This notable improvement was enabled by a reduction in selling, general, and admin expenses to just 53% of revenue compared to 72% in the year-ago quarter.

Amid volatility in crypto markets, Coinbase has not been reluctant to expand into new markets. This year, the company has expanded into Brazil, Singapore, and Canada and has obtained a license to operate in Spain as well. This geographic expansion is hurting the company’s bottom line today but can prove to be value accretive in the future if the company can replicate its success in the U.S. in these international markets.

During the third quarter, Coinbase also obtained the necessary regulatory approval to offer derivative products, which is another milestone achievement. These approvals include a green light by the Bermuda Monetary Authority to offer crypto futures to eligible non-U.S. retail customers and approval from the National Futures Association to offer futures to U.S. clients via advanced trading.

According to CEO Brian Armstrong, derivative products account for nearly 75% of global crypto trading volume, which signifies the market opportunity for Coinbase. As an established crypto platform, Coinbase is likely to lure traders who are looking for leveraged derivative products in the future, creating an opportunity for trading revenues to grow.

Is Coinbase Stock a Buy, According to Analysts?

Coinbase continues to attract investor attention, with crypto markets making a strong comeback this year. The expected SEC approval of a spot Bitcoin ETF has further boosted investor confidence in the company.

However, JPMorgan (NYSE:JPM) analyst Nikolaos Panigirtzoglou recently claimed that approval of a spot Bitcoin ETF will not immediately attract a substantial amount of money to crypto markets. Barclays analyst Benjamin Budish shares a similar opinion, as he believes it is too early to predict how a Bitcoin ETF will contribute to Coinbase’s net income in the short term.

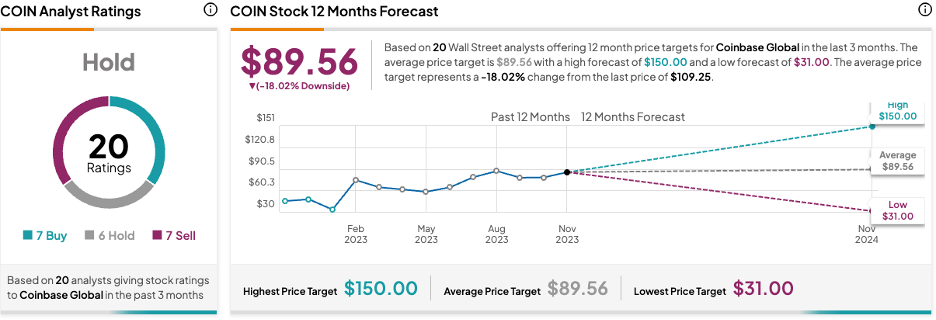

Based on the ratings of 20 Wall Street analysts, Coinbase stock has a Hold consensus rating. The average Coinbase stock price target is $89.56, which implies downside risk of 18% from the current market price.

This downside risk can be better understood by evaluating the current valuation level of Coinbase. The company is currently valued at a price-to-forward sales multiple of close to 9.0, which implies that the market is placing bets on stellar revenue growth in the coming years.

However, given Coinbase’s reliance on trading fees in the short term, paying premium prices to invest in the company seems irrational, as a crypto bear market will wipe billions of dollars worth of trading volume from the market.

The Takeaway: Coinbase is Richly Valued

Coinbase is moving in the right direction by diversifying its revenue streams, expanding into new markets, and cutting costs while not losing focus on growth. Although these positive developments deserve praise, the company’s current valuation seems to be ahead of its fundamentals, which poses a risk to investors betting on the company today.