Citigroup (NYSE:C) recently reported its Q4-2022 results, which I’ll discuss in detail in this article. The bank is sowing the seeds of resilient profitability. It’s building credit reserves in anticipation of a mild recession and is also frontloading investments to allow it to reach its medium-term profitability targets. Despite a strong capital position and an appealing tangible book discount, buybacks remain on hold. I expect a resumption in buybacks into H2 2023, or 2024 at the latest, once sufficient progress has been made on remaining divestitures and management has better visibility on the economy.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Citigroup reports results in four main operating segments: Institutional Clients Group at 50.9% of Q4-2022 revenues, Personal Banking and Wealth Management at 33.9% of revenues, Legacy Franchises at 11.4%, and Corporate/Other at 3.9% of revenues. Let’s analyze how each segment performed.

Operational Overview

Personal Banking & Wealth Management experienced the highest year-over-year revenue growth at 5%, driven by U.S. personal banking, which was up 10% from 2021. However, operating leverage was negative, with expenses increasing at a faster 7% pace due to investments in transformation and control initiatives.

The segment’s return on tangible common equity (RoTCE) was underwhelming at just 1.4%, driven by reserve build in the allowance for credit losses (allowance for credit losses are reserves for the amount of money that a lender doesn’t expect to collect from its debtors), partially due to volume growth in the cards business, as well as a deterioration in macroeconomic assumptions.

Overall, Citigroup’s provisioning can be described as somewhat conservative, given a 2% decrease in total loans from year-end 2021 to $657.2 billion against a 3.2% increase in the allowance for credit losses to $16.97 billion.

Institutional Clients Group reported a lower year-over-year revenue growth of 3% compared to the consumer business above but likewise saw negative operating leverage, with expenses up 6% from 2021. As outlined above, elevated expense levels were driven by transformation investments.

The segment’s RoTCE of 7.9% benefited from reserve releases in the quarter.

Legacy Franchises saw positive operating leverage, with a revenue decline of 6% against a cost decline of 38% from 2021, largely due to a non-recurring charge in the prior-year period.

Out of 14 non-strategic consumer markets earmarked for exit, five divestitures have already closed. The bank is on track to close the remaining four Asia businesses and is negotiating the exit of the Mexico consumer business. Citigroup still sees the potential capital impact in a range of severe stress scenarios in its remaining Russia business at $2 billion.

For the bank as a whole, RoTCE came in at 5.8% in Q4 and 8.9% for the full year, with tangible book finishing 2022 at $81.65 per share.

Citigroup Outlook – 2023 and Beyond

Against the underwhelming Q4-2022 results, the 2023 targets for Citigroup look promising, albeit continuing the trend of negative operating leverage:

- Revenues of $78 billion-$79 billion, or growth of 3.6%-4.9% over 2022.

- Expenses of $54 billion, or growth of 5.3% over 2022.

The immediate outlook for Q1 2023 is for expense growth in the mid-single digits, excluding divestiture-related impacts. The environment for investment banking fees should also start to improve into the new year after a dismal ~60% drop from Q4 2021.

The medium-term targets of the next three to five years remain in place, namely an 11%-12% RoTCE and a shift to higher-returning businesses. Management also expects to be able “bend the curve on expenses towards the end of 2024”, further elaborating, “The three main drivers of the necessary expense reduction will be benefits from the exit, which will be included in legacy franchise the benefits from our investments in transformation and control and the simplification of the organizational structure.”

Citigroup’s Capital Position

Citigroup’s CET1 ratio (which looks at a bank’s capital relative to its assets) finished 2022 at 13%, up 0.7% or 70 basis points quarter-over-quarter, benefiting mostly from risk-weighted assets optimization and the closing of consumer business sales (around 50 basis points impact). The 13% milestone is already 1% above the January 2023 requirement of 12% and is in line with the bank’s target for the middle of 2023. Longer term, Citigroup sees the appropriate ratio to be between 11.5%-12%.

Citigroup’s exit from the Mexico consumer business should have a negative impact on CET1 this year.

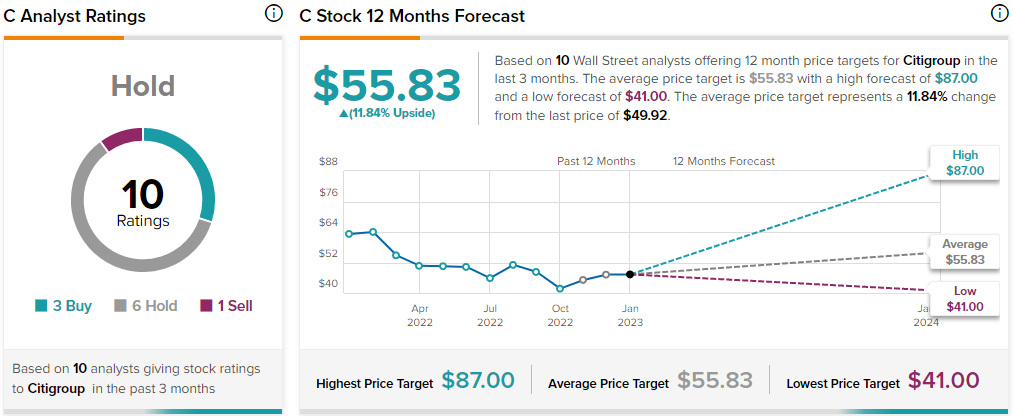

Is Citigroup Stock a Buy, According to Analysts?

Turning to Wall Street, Citigroup earns a Hold consensus rating based on three Buys, six Holds, and one Sell rating. Additionally, Citigroup’s average price target is $55.83, implying 11.84% upside potential.

The Takeaway

Despite having no immediate catalyst in the next few quarters, a resumption of buybacks later in 2023 should prove to be the first driver for the stock. Later in 2024, operating leverage is forecast to improve, which would allow the bank to reach its profitability targets into 2025 and beyond.

While turnaround risks remain for the next two years, the margin of safety you get with a tangible book discount of about 40% creates a disproportionate risk-reward opportunity. If Citigroup is successful in executing its RoTCE ambitions, the stock should rerate in line with peers (closer to its tangible book value). Even if management fails to deliver on its return aspirations, the stock could likely move sideways, awaiting a more fruitful turnaround plan.