Chip stocks have had a brutal ride in 2022. The tables have turned on a sector particularly sensitive to cycles; after seeing outsized growth during the pandemic, and despite the global chip shortage, waning demand has seen many in the segment hit hard. Factor in some lofty valuations, a slowing economy and fears of a full-blown recession and the result is the SOX (the main Semiconductor index) is down by 38% year-to-date.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

That said, there are many good companies operating in the space whose shares are now at very depressed levels. In fact, Rosenblatt Securities’ Hans Mosesmann, one of Wall Street’s top analysts and an expert on all chip matters, thinks some names in the sector are due to push much higher over the coming months.

So, let’s take a look at two of this 5-star analyst’s picks and see why he finds them so appealing right now. With help from the TipRanks database, we can see that Mosesmann is certainly not alone in his bullish stance; both are rated as Strong Buys by the analyst consensus too.

Marvell Technology, Inc. (MRVL)

We’ll start with one of the semiconductor sector’s heavyweights, Marvell, a maker of integrated circuits. This large-cap caters to numerous end markets such as data centers, enterprise, automotive, cloud, consumer and carrier infrastructure. While several years ago most of the firm’s business came from the consumer electronics segment, following several acquisitions, the majority is now generated from data infrastructure (data center, industrial, automotive, mobile network). Seeing out 2021, the company had a 6,000+ workforce, more than 10,000 global patents, and annual revenue of $4.5 billion.

Despite being affected by ongoing supply constraints, the revenue haul has continued its growth trajectory in 2022, as was evident in the company’s latest quarterly report – for the second quarter of fiscal year 2023 (July quarter). Revenue increased by 41% year-over-year to a record $1.52 billion, while adj. EPS of $0.57 was up from the $0.34 delivered in the same period last year.

However, supply chain snags were cited as the main reason behind a disappointing outlook. For the October quarter, Marvell guided for revenue of $1.56 billion, below the $1.585 billion expected on Wall Street. Likewise, the adj. EPS of $0.59 at the midpoint, fell short of consensus at $0.61.

The market did what the market does in such situations and sent shares down subsequently. All in all, in 2022’s bear market, MRVL shares have shaved off 45% of their value.

That is not a concern for Mosesmann, who remains “bullish” on the company’s prospects.

“CEO Matt Murphy articulated a strong acceleration into the January quarter and remains incrementally more bullish on calendar 2023 as supply constraints ease somewhat (they will not go away completely), and multiple new products and custom ASIC ramp inflect (incremental $400 million plus, and $800 million plus in 2024),” Mosesmann explained. “Matt Murphy’s team has put together a world class execution machine that is strategically positioned to increase dollar content and customer engagement over the long term.”

Mosesmann is bullish, indeed; along with a Buy rating, the analyst’s $125 price target makes room for 12-month gains of 162%. (To watch Mosesmann’s track record, click here)

Most are echoing Mosesmann’s sentiment; barring 3 fencesitters, all 17 other recent analyst reviews are positive, making the consensus view here a Strong Buy. The average target stands at $71.20 and could generate returns of ~49% in the year ahead. (See Marvell stock forecast on TipRanks)

Lattice Semiconductor (LSCC)

Next up, we have Lattice Semiconductor, a maker of low power, field-programmable gate arrays (FPGAs). Given they are reconfigurable and can be programmed to execute any digital logic, FPGAs are well-suited for adaptive systems. After focusing on several other products too, over the past few years, Lattice has made a conscious decision to focus its energies on the low-power FPGA market, with a mission statement of becoming the low power programmable leader.

Looking at the constant upwards movement of the revenue haul, it’s a plan that appears to be working. Sales have been steadily growing over the past few years. The latest set of results – for F2Q22 – showed $161.37 million at the top-line, a 28.2% year-over-year increase. At the bottom-line, the company delivered adj. EPS of $0.42, also up from the $0.25 delivered in the same quarter last year. Both results were also above analysts’ expectations.

Even better, bucking the trend for warnings of a slowdown, revenue for Q3 is expected to be in the range between $161 million and $171 million; the consensus estimate stood at just $161.43 million.

The shares, though, have not been immune to the overall market conditions, and have retreated ~29% since the turn of the year.

Nevertheless, it’s the sort of performance which has Mosesmann singing the company’s praises.

“Lattice delivered another strong beat and raise for 2Q22 despite weakness in Consumer (8% of sales), driven by momentum in Communications/Computing and Industrial/ Automotive. A much richer mix of Nexus products, higher S/W attach rates, and share gains in small FPGAs are driving topline and gross margins,” the analyst said. “FCF now at an impressive 28% is a testament to the success of the A-team Jim Anderson recruited in 2017/18. We see Lattice as uniquely positioned as the only FPGA player innovating in small, and upcoming mid-tier, FPGA’s in a new era of AI disruption that requires a combination of programmability, low power, high parallel data-centric workloads, and faster time to market requirements.”

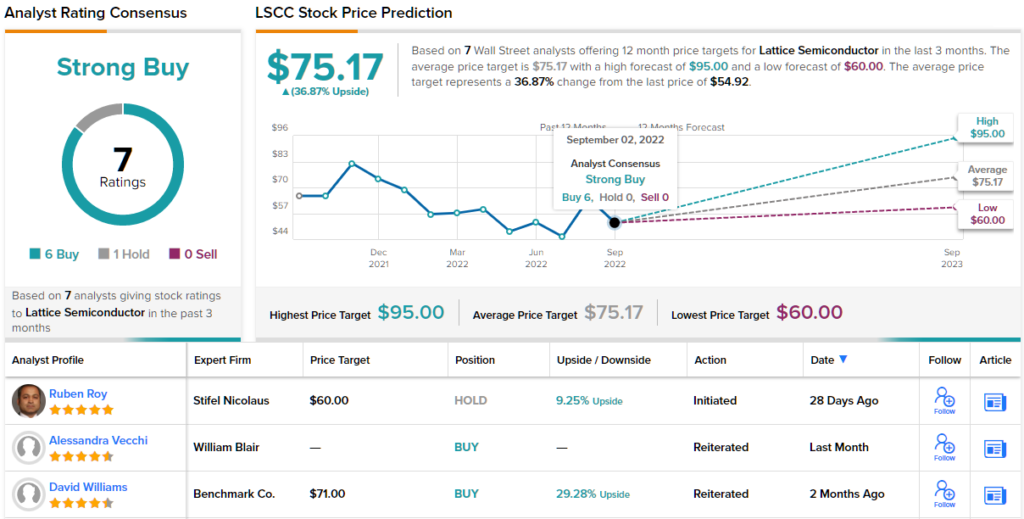

Unsurprisingly, then, Mosesmann rates Lattice shares a Buy, backed by a $95 price target. The implication for investors? Upside of 73% from current levels.

And what about the rest of the Street? Most are on board too; the ratings break down as 6 to 1 in favor of Buys over Holds, all culminating in a Strong Buy consensus rating. The forecast calls for one-year gains of ~37%, considering the average target stands at $75.17. (See Lattice Semiconductor stock forecast on TipRanks)

To find good ideas for chip stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.