Chipotle Mexican Grill’s (NYSE:CMG) recent rally has been absolutely astonishing. Following the company’s Q1 results, shares of Chipotle reached stratospheric heights, extending the already massive gains that it had achieved in recent months. In fact, Chipotle stock is trading about 63.5% higher than it was last year.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

To a considerable degree, there are numerous compelling factors that underpin Wall Street’s optimistic outlook, particularly due to Chipotle’s exceptional operational prowess within the quick service restaurant (QSR) industry, coupled with substantial potential for sustained expansion.

Nevertheless, the stock’s current valuation has become progressively challenging to justify as it continues to surge unabated without sufficient investor consideration for a potential market correction. Consequently, I am neutral on the stock.

What’s Driving Chipotle Stock’s Never-Ending Rally?

The “secret” behind Chipotle’s never-ending rally lies in the company’s promising position within the QSR space. To better understand this, it’s important to recognize the two key phases involved in a QSR’s brand expansion. Let’s dive deeper into this concept!

The initial phase entails establishing a strong foothold in the QSR market, which requires considerable investments in corporate-owned locations to serve as proof of concept for potential franchisees. The subsequent phase marks the maturity stage for a QSR chain, characterized by a shift towards franchisee-owned locations.

Take Shake Shack (NYSE:SHAK), for instance, which is still somewhere in between, continuing to open both corporate and licensed locations, as it is still establishing its presence in new markets. At the end of Q1, there were 449 Shacks in operation, with only 189 being licensed. Then, look at companies within the QSR space that have reached peaked maturity, like McDonald’s (NYSE:MCD) and Domino’s Pizza (NYSE:DPZ), with 95% and 99% of their restaurants owned and operated by third-party franchisees, respectively.

The second phase is where the big bucks are made, as high-margin royalties on franchise-related sales, rental revenues from franchised establishments, and ingredient distribution to franchisees can drive significant earnings growth, all without having to deal with the operational challenges of running the restaurants themselves.

What sets Chipotle apart in all of this is its exceptional achievement of completing the first phase without franchising a single location. No other company in the industry has managed to reach ~3,200 locations without resorting to franchising — except for Chipotle. The company has achieved remarkable menu optimization efficiencies, allowing it to achieve impressive margins (its trailing-12-months operating margin stands at 15.2%) despite going through the hassle of actually running each location.

You now see why the market is particularly excited to see how the company’s profitability will evolve from here, especially if Chipotle ends up choosing to scale its profitability faster by franchising locations.

Combine this with its ongoing underlying growth, which remains vigorous, and the picture becomes even clearer. In its Q1 results, Chipotle posted revenue growth of 17.2% to $2.4 billion, with comparable sales growth of 10.9% being a significant organic growth driver.

Back to my earlier point regarding Chipotle’s impressive profitability, the operating margin in Q1 came in at 15.5%, a massive increase compared to 9.4% in the prior-year period, while its restaurant-level operating margin was 25.6%, implying a year-over-year increase of 490 basis points.

The combination of exceptional revenue growth and an expansion in margins resulted in earnings per share skyrocketing by 84.2% to $10.50. Again, you can see why these awe-inspiring results continue to fuel investor enthusiasm, propelling the stock to even greater heights.

Is CMG Stock a Buy, According to Analysts?

Turning to Wall Street, Chipotle Mexican Grill retains a Strong Buy consensus rating based on 18 Buy and five Hold ratings assigned in the past three months. Nonetheless, at $2072.27, the average Chipotle Mexican Grill stock price target suggests 1.5% downside potential.

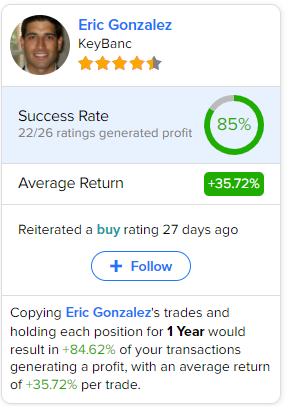

If you’re wondering which analyst you should follow if you want to buy and sell CMG stock, the most accurate analyst covering the stock (on a one-year timeframe) is Eric Gonzalez from KeyBanc (NYSE:JPM), with an average return of 35.72% per rating and an 85% success rate. See below.

The Takeaway

Surprisingly, Wall Street analysts remain bullish on Chipotle Stock. However, even by their estimates, shares appear to have exceeded their sky-high price targets. Following the stock’s massive rally over the past year, I struggle to see how the company’s earnings can grow into the stock’s valuation, even if Chipotle meets the market’s expectations.

Based on Chipotle’s Q1 results and management’s Q2 outlook, the Street expects the company to achieve earnings-per-share growth of 35.3% to $44.34, which implies a forward P/E of over 47 times. In my view, this multiple suggests the stock is priced for perfection, as the company will have to sustain an equally strong earnings-per-share growth rate in the coming years to grow into its valuation.

Any potential setback in profitability could result in significant stock losses, as there is no room for error given CMG’s current valuation. Accordingly, I am neutral on the stock.